General information, not personalised tax, legal or investment advice.

: Complete Guide](https://file-host.link/website/sentinelassetmanagementllc-lo1ayr/assets/refined-images/1778507216856000_469d582b9911469f999bb74e0353ecc6/360.webp)

The difference wasn't luck. It was planning.

Long-term tax planning for generational wealth isn't about loopholes or last-minute maneuvers. It's about building a deliberate, year-round strategy that treats taxes as one of the largest controllable expenses across a lifetime. This guide covers the essential areas: investment tax efficiency, gifting, trusts, charitable giving, and heir preparation—each working together to preserve what you've built and pass it forward on your terms.

Here's What You'll Learn

- Tax planning is a year-round, multi-decade discipline—not an April filing exercise

- Gifting strategies, trust structures, investment decisions, and retirement distributions are interconnected — adjusting one affects the rest

- IRS-sanctioned tools — from annual gift exclusions to dynasty trusts — exist specifically to lower the tax burden on wealth transfers

- Starting early lets more compounding happen outside your taxable estate, where it benefits heirs directly

- Coordinating tax, investment, and estate planning through one advisory team prevents costly blind spots between disciplines

What Is Generational Wealth and Why Does Tax Planning Matter?

Generational wealth refers to assets—financial accounts, real estate, business interests, investments—intentionally built and transferred across two or more generations. This isn't exclusively for the ultra-wealthy. Any family building assets that outlast one lifetime has a generational wealth concern.

The $124 Trillion Transfer Through 2048

According to Cerulli Associates' 2024 research, an estimated $124 trillion will transfer through 2048. Of this total, approximately $105 trillion will flow to heirs, while $18 trillion will be directed to charitable causes. High-net-worth and ultra-high-net-worth households—just 2% of all households—drive more than 50% of the total volume.

Three Destinations for Every Dollar

At death, every dollar in an estate goes to one of three places:

- Taxes

- Charity

- Heirs

How much goes to taxes is a planning variable, not a fixed outcome.

The federal estate tax affects only about 0.1% to 0.2% of decedents. The July 2025 passage of the "One Big Beautiful Bill Act" (P.L. 119-21) permanently increased the federal estate and gift tax exemption to $15 million per individual for 2026, indexed annually for inflation—meaning a married couple can now shield up to $30 million. These figures remain subject to legislative adjustment, so confirming the current-year exemption with an advisor is always worth the call.

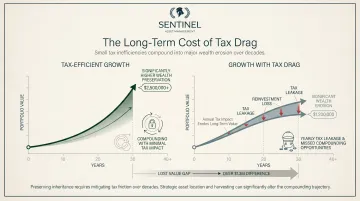

Taxes Compound in Reverse

Every dollar lost to unnecessary taxation is also a dollar that stops compounding for heirs—permanently. Over a 20- or 30-year horizon, that drag accumulates fast. The difference between passive tax management and a coordinated planning strategy can represent hundreds of thousands, sometimes millions, in wealth that reaches the next generation rather than the IRS.

Tax-Efficient Investment Strategies for Long-Term Wealth Building

Investment decisions made today shape your family's tax burden for decades. Strategic asset location, capital gains management, and retirement account optimization are foundational to building wealth that endures.

Asset Location: The Right Investments in the Right Accounts

Asset location is the strategy of placing tax-inefficient investments—those generating ordinary income, such as bonds and REITs—inside tax-advantaged accounts (IRAs, 401(k)s). Tax-efficient investments—broadly diversified index funds, long-term equity positions—belong in taxable brokerage accounts.

This coordination reduces drag on after-tax returns across a lifetime without changing your overall asset allocation. Morningstar research indicates that over a 10-year period, the average equity mutual fund lost 1.48% of its annualized return to taxes. Index funds, by construction, typically have lower turnover, allowing investors to retain a larger share of their pre-tax returns.

Capital Gains Management: Holding Periods and Realization Timing

The tax code treats long-term capital gains—assets held over one year—at significantly lower rates than ordinary income.

| Tax Rate | 2025 Taxable Income (Married Filing Jointly) |

|---|---|

| 0% | $0 to $96,700 |

| 15% | $96,701 to $600,050 |

| 20% | $600,051 or more |

Holding periods matter. Avoiding unnecessary portfolio turnover and being deliberate about when gains are realized—especially in years where other income is elevated—can meaningfully reduce your tax bill.

Tax-Loss Harvesting: Offsetting Gains Strategically

Tax-loss harvesting involves selling investments at a loss to offset realized gains elsewhere in the portfolio and potentially up to $3,000 of ordinary income annually. Any excess losses carry forward to future tax years.

This works best when integrated with rebalancing decisions rather than executed as a reactive, year-end move. One critical constraint: the IRS "wash-sale" rule disallows the loss deduction if a "substantially identical" stock or security is purchased within 30 days before or after the sale.

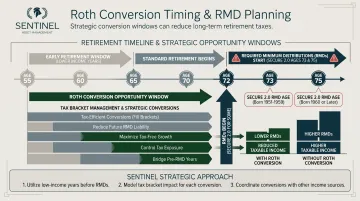

Roth IRA Conversions: A Multigenerational Tool

Converting traditional (pre-tax) retirement assets to Roth accounts during lower-income years reduces future required minimum distributions (RMDs), lowers taxable income in retirement, and allows heirs to receive tax-free distributions.

For 2025, direct Roth IRA contributions phase out completely for married couples filing jointly with a modified adjusted gross income (MAGI) of $246,000 or more. That said, there are no income limits for Roth conversions—high-net-worth individuals can convert traditional IRA assets to Roth IRAs by paying ordinary income tax on the converted amount.

The right years to convert depend on current-year income, other tax strategies in play, and your retirement income picture—not a blanket rule.

Updated RMD Timelines Under SECURE 2.0

The SECURE 2.0 Act significantly altered RMD timelines:

| Birth Year | Applicable RMD Age |

|---|---|

| 1951 through 1959 | Age 73 |

| 1960 and later | Age 75 |

The delay in RMDs provides a longer window for strategic Roth conversions before mandatory distributions increase taxable income and potentially push retirees into higher brackets.

Building a Tax-Efficient Portfolio Framework

A tax-efficient investment portfolio begins with a clear Investment Policy Statement reflecting your income needs, tax situation, and long-term goals. Sentinel Asset Management builds globally diversified, tax-efficient portfolios around this framework—each guided by an Investment Policy Statement and structured to minimize lifetime tax liability as one integrated part of a client's broader financial plan.

Gifting Strategies That Reduce Your Taxable Estate

Strategic gifting moves assets out of your taxable estate while you're alive, reducing estate taxes and allowing you to witness the impact of your generosity.

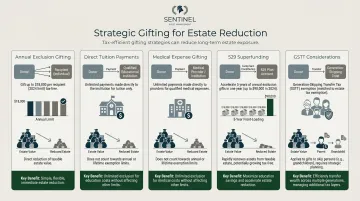

Annual Gift Tax Exclusion

For 2025 and 2026, the IRS annual gift tax exclusion is $19,000 per recipient ($38,000 for a married couple splitting gifts). These gifts don't consume any of your lifetime exemption.

Key benefits:

- Transfer $19,000 per recipient per year without gift tax or reducing your lifetime exemption

- Married couples can combine their exclusions, gifting $38,000 per recipient annually

- No limit on the number of recipients

Direct Payments for Medical Care and Tuition

Under IRC §2503(e), you can make unlimited, tax-free payments for another person's tuition or medical expenses. These qualified transfers don't count toward the annual gift tax exclusion or the lifetime exemption.

Payments must go directly to the educational institution or medical provider. Reimbursing the individual after the fact doesn't qualify.

Example: A grandparent can pay a grandchild's $60,000 annual college tuition directly to the university, transferring significant value without touching the annual exclusion or lifetime exemption. That same year, they could still gift the grandchild $19,000 under the annual exclusion.

529 Superfunding: Front-Loading Education Savings

The IRS permits front-loading up to five years of annual gift tax exclusion contributions into a 529 education savings account in a single year. For 2025, this allows a lump-sum contribution of $95,000 per beneficiary ($190,000 for a married couple).

The contribution is treated ratably over five years, and the election must be reported on IRS Form 709. Donors must avoid making additional gifts to that recipient during the five-year period to prevent exceeding the annual exclusion.

The result: a substantial transfer out of your taxable estate today, funded through annual exclusion rules spread across five years.

Generation-Skipping Transfer Tax (GSTT)

The GSTT is a separate tax that applies to gifts or bequests to grandchildren or those more than 37.5 years younger than the giver. It has its own exemption—identical to the lifetime estate tax exemption ($15 million for 2026)—and is not an additional exemption on top of it.

Without deliberate GSTT planning, a transfer that clears the estate tax threshold could still trigger this parallel tax at the same rate — eroding what reaches the next generation.

Step-Up in Cost Basis and Upstream Gifting

Under IRC §1014, when a person dies, the cost basis of assets in their estate resets to the fair market value at the date of death—effectively eliminating accumulated capital gains for the heir.

Upstream gifting involves gifting appreciated assets to a parent with a smaller estate, who then bequeaths them to grandchildren. This can allow a family to capture both estate tax exemptions and the step-up in basis.

The strategy carries real risks worth weighing before proceeding:

- Loss of control over the assets once transferred

- Creditor exposure at the recipient's level

- The recipient may bequeath the assets elsewhere

- The IRC §2035 three-year inclusion rule and potential step-transaction doctrines

Upstream gifting lacks formal IRS blessing and should be carefully evaluated with legal and tax advisors.

How Trusts Preserve and Transfer Wealth to Future Generations

Trusts remove assets from your taxable estate while keeping you in control — protecting beneficiaries and reducing taxes across multiple generations.

Irrevocable Trusts as Estate Planning Vehicles

Once assets are transferred into an irrevocable trust, they are removed from the grantor's taxable estate—meaning future appreciation occurs outside the estate.

Commonly used structures:

Grantor Retained Annuity Trusts (GRATs): Allow appreciation above an IRS-assumed interest rate (4.6% in April 2026) to pass to heirs gift-tax free. Any asset appreciation exceeding this rate transfers to beneficiaries tax-free.

Spousal Lifetime Access Trusts (SLATs): Remove assets from the estate while allowing a spouse to benefit. One critical risk: if both spouses create substantially identical trusts for each other, the IRS may invoke the "reciprocal trust doctrine" (U.S. v. Grace) and pull those assets back into their taxable estates. Each trust must differ in terms, beneficiaries, trustees, and timing.

Intentionally Defective Grantor Trusts (IDGTs): Allow the grantor to pay income taxes on trust earnings. Under IRS Revenue Ruling 2004-64, the grantor's payment of the trust's income tax liability is not considered an additional taxable gift to beneficiaries—effectively an additional tax-free gift.

Irrevocable Life Insurance Trusts (ILITs)

By having the trust own a life insurance policy rather than the individual, the death benefit is excluded from the taxable estate. This provides immediate liquidity for heirs to pay estate taxes or equalize inheritances.

Critical timing rule: Under IRC §2035, if an insured transfers an existing policy into an ILIT and dies within three years, the entire death benefit is pulled back into the gross estate. The ILIT should ideally be the original applicant and owner of a new policy to avoid this.

Dynasty Trusts for Multigenerational Protection

Where ILITs solve a liquidity problem at death, dynasty trusts (also called generation-skipping trusts) solve a longer-horizon problem: passing assets across multiple generations without triggering estate taxes at each transfer.

Structured correctly, they offer:

- Asset protection from creditors, divorces, and lawsuits at every generation

- No estate tax exposure at each generational handoff

- Perpetual duration in states like South Dakota, Delaware, and Nevada, which allow trusts to run for hundreds of years or indefinitely

Practical Steps to Establish a Trust

- Determine which type fits your family's goals

- Select a trustee with appropriate financial knowledge and willingness to serve

- Draft the trust document with an estate planning attorney

- Retitle assets into the trust's ownership—this step is often overlooked, but the trust must legally own the assets to be effective

Charitable Giving as a Tax Planning Tool

Charitable giving can serve three goals at once: advance philanthropic intent, reduce estate taxes, and generate income. For families building multigenerational wealth, that combination makes it one of the most efficient planning tools available.

Donating Appreciated Assets vs. Cash

Donating long-term capital gain property—such as publicly traded stock held for more than one year—to a public charity allows you to:

- Claim an income tax deduction for the fair market value of the asset

- Completely avoid capital gains tax on the appreciation

- Allow the charity to sell the asset tax-free, since tax-exempt organizations owe no capital gains on the transaction

| Charity Type | AGI Deduction Limit for Appreciated Property |

|---|---|

| Public Charities & DAFs | 30% of AGI |

| Private Nonoperating Foundations | 20% of AGI |

If the donation exceeds AGI limits, the excess contribution can be carried forward for up to five subsequent tax years.

Example: You purchased stock for $10,000 that's now worth $50,000. Donating the stock allows a $50,000 charitable deduction and avoids $8,000 in capital gains tax (at 20% rate). Donating cash only provides a $50,000 deduction with no capital gains benefit.

Donor-Advised Funds (DAFs)

A DAF is a giving account established at a public charity. You make an irrevocable, tax-deductible contribution and retain advisory privileges to recommend grants to other charities over time.

According to the National Philanthropic Trust's 2024 DAF Report, total charitable assets in DAFs reached $251.52 billion in 2023, with donors recommending $54.77 billion in grants.

DAFs are particularly valuable in high-income years—such as the year of a major liquidity event—where front-loading charitable intent captures the deduction when it's most valuable.

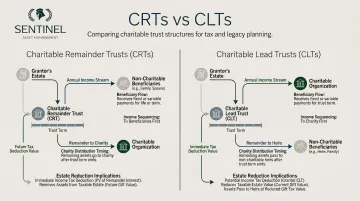

Charitable Remainder Trusts (CRTs) and Charitable Lead Trusts (CLTs)

For families who want more structural control than a DAF provides, trust-based vehicles offer additional flexibility. Charitable Remainder Trusts (CRTs) provide the donor (or named beneficiary) with income for a set period before the remainder passes to charity. Benefits include:

- Immediate partial income tax deduction

- Capital gains deferral on appreciated assets placed inside the trust

- The CRT is tax-exempt, so it can sell highly appreciated assets without paying immediate capital gains tax

Charitable Lead Trusts: Work in reverse—they pay an income stream to charity first, with the remainder passing to family heirs.

Either structure can significantly reduce estate exposure while transferring wealth to heirs. Families already engaged in legacy planning often find CRTs and CLTs complement their broader estate strategy rather than complicate it.

Preparing Heirs and Staying Ahead of Tax Law Changes

Successful wealth transfer requires more than legal documents and tax strategies. It requires preparing heirs and adapting to legislative changes.

Heir Preparation: The Overlooked Half of Wealth Transfer

Families that successfully transfer assets but fail to prepare heirs for financial responsibility often see that wealth erode within one or two generations. While the widely cited statistic that "70% of families lose their wealth by the second generation" is based on a flawed 1987 study regarding family businesses—not diversified financial wealth—the principle remains valid: unprepared heirs struggle.

Essential components of heir preparation:

- Open family conversations about long-term objectives

- Discussions about the values behind the wealth

- Clarity about the role each heir is expected to play

- Financial literacy education—however uncomfortable

These conversations don't happen naturally — they need to be built into the planning process itself. That's what separates families who preserve wealth from those who don't.

Legislative Risk: Exemptions and Rates Change

Estate tax exemptions, gift exclusions, and capital gains rates are all subject to congressional action. Two areas deserve close attention:

- Estate tax exemptions: The current $15 million federal exemption is permanent under P.L. 119-21, but future legislation could still reduce it — and families with large estates should plan around that possibility now.

- Step-up in basis: The proposed Equal Tax Act (H.R. 5336) would treat death as a realization event, eliminating the step-up and taxing embedded capital gains at death.

Families with growing estates should monitor these developments and consult advisors about whether acting now — such as using the full lifetime exemption before any reduction — makes sense for their situation.

The Role of an Integrated Advisory Team

Tax strategy, investment management, retirement income planning, and estate documents need to work together as a single system. When advisors operate in silos — an estate attorney here, a tax preparer there, a portfolio manager elsewhere — strategies that look sound in isolation can conflict or leave significant gaps.

Sentinel Asset Management coordinates tax-efficient portfolios, legacy planning, and retirement income sequencing as a unified plan, drawing on 100+ years of combined advisory experience across its team. The question worth asking: are your current advisors actually talking to each other?

Frequently Asked Questions

What is considered intergenerational wealth?

Intergenerational wealth refers to financial assets—including investment accounts, real estate, business interests, and life insurance—that are intentionally built and passed from one generation to the next. It's not limited to the ultra-wealthy and applies to any family with assets intended to outlast one lifetime.

How much can I gift to my children each year without paying taxes?

For 2025 and 2026, the IRS annual gift tax exclusion is $19,000 per recipient. Married couples can combine their exclusions, gifting $38,000 per recipient annually. Amounts above the annual limit reduce your lifetime exemption rather than immediately trigger a tax.

What is the difference between estate tax and inheritance tax?

The federal estate tax is paid by the deceased's estate before assets are distributed; inheritance tax is paid by the recipient in certain states based on the amount received. Not all states impose an inheritance tax, and the federal estate tax only applies to estates above the lifetime exemption threshold ($15 million for 2026).

When is the right time to start tax planning for generational wealth?

The earlier the better. Strategies like annual gifting, trust funding, and Roth conversions are compounding strategies that benefit from time. The best time to start is before a major liquidity event, health change, or legislative shift forces a reactive decision.

How does a step-up in cost basis work for inherited assets?

When an asset is inherited, its cost basis resets to the fair market value at the date of the original owner's death. This means heirs owe no capital gains tax on appreciation that occurred during the original owner's lifetime and could sell the asset immediately with little to no capital gains tax burden.

Do I need a trust to transfer wealth to the next generation?

A trust is not always required. Annual gifting, direct payments for medical care and tuition, and beneficiary designations on retirement accounts and life insurance can transfer significant wealth without one. That said, trusts become highly valuable for larger estates, blended families, heirs needing asset protection, or families aiming to minimize estate taxes across multiple generations.

Effective generational wealth planning is a deliberate, multi-decade discipline — and the strategies in this guide work best when coordinated as a single integrated system. The strategies outlined in this guide—tax-efficient investing, strategic gifting, trust structures, charitable giving, and heir preparation—work most effectively when coordinated as a single, integrated system.

Sentinel Asset Management has guided 2,000+ clients through retirement and legacy planning, with an average plan horizon of 20+ years and 100+ years of combined advisory experience across the team. That depth allows the firm to coordinate tax strategy, legacy planning, and retirement income sequencing as one cohesive plan — not separate conversations.

If you're ready to build a coordinated plan that treats taxes as one of the largest controllable expenses across your lifetime, contact Sentinel Asset Management to schedule a consultation.

Take the next step in your financial journey by exploring our courses page for upcoming live seminars.