General information, not personalised tax, legal or investment advice.

Introduction

Picture this: A retired couple with $2 million in retirement accounts, a paid-off home, and two adult children assumes their estate plan is complete because they've written a will. Then their financial advisor runs a comprehensive review and discovers their beneficiary designations name their ex-daughter-in-law, their IRA will force their children to pay taxes on $200,000 in a single year due to new RMD rules, and their trust was never funded—meaning it's legally worthless.

It's more common than most families expect. 56% of U.S. adults have no estate planning documents whatsoever, and among those who do, 50% of all trusts go unfunded, while nearly 40% have outdated beneficiary designations that override their carefully drafted wills.

This post explains what true estate planning and tax advisory services actually cover: coordinating every financial account, beneficiary designation, tax strategy, and legal document to work together as a unified plan.

You'll learn who needs these services most, what a financial advisor can handle without an attorney, and how the right tax strategies can reduce what your heirs owe.

Key takeaways

- Estate and tax planning work best when integrated—not treated as separate annual tasks

- Financial advisors handle most estate coordination (beneficiary forms, account titling, tax-efficient withdrawals) without attorney involvement for every step

- Roth conversions, strategic gifting, and smart asset location can each cut heirs' tax bills by tens of thousands

- Retirement, divorce, and special needs planning each trigger time-sensitive estate decisions that can't wait

- A personalized plan preserves wealth, reduces taxes, and ensures your assets reach the people and causes you care about

What Estate Planning and Tax Advisory Services Actually Cover

Beyond the Will: The Full Estate Planning Ecosystem

Most people think estate planning means writing a will. That's like thinking "getting in shape" means buying a gym membership: it's one piece of a much larger system.

A comprehensive estate plan includes:

- Beneficiary designations on retirement accounts, life insurance, and payable-on-death accounts

- Powers of attorney for financial and healthcare decisions

- Healthcare directives (living wills)

- Trusts for tax efficiency, probate avoidance, or special needs protection

- Proper asset titling across individual, joint, and trust ownership structures

- Insurance policy coordination so coverage actually matches your intentions

Here's the critical issue: beneficiary designations legally override your will. If your IRA names your ex-spouse but your will leaves everything to your children, your ex-spouse gets the IRA. No exceptions.

Tax Advisory in the Estate Context

Tax advisory for estate planning goes far beyond filing annual returns. It means minimizing lifetime tax liability through strategic decisions about:

- Timing distributions from the right accounts to reduce income tax exposure

- Choosing which assets to hold until death for a step-up in basis versus gifting them now

- Reducing the taxable estate through targeted gifting and trust structures

- Using the $19,000 annual exclusion (2025) and $13.99 million lifetime exemption before they shrink

Documents vs. Strategy: Who Does What?

Estate planning documents are legal instruments — wills, trusts, powers of attorney — drafted by an attorney.

Estate planning strategy is the financial architecture: coordinating accounts, beneficiary designations, investment structure, and tax-efficient transfers. A financial advisor owns this layer.

An attorney builds the legal framework. A financial advisor ensures your actual money flows through it as intended — and that the two stay aligned as your life changes.

The Coordinated Financial Ecosystem

That alignment is why the most effective planning treats investment management, tax planning, retirement income, and legacy planning as one integrated system — not separate silos.

For example:

- Investment decisions account for tax location (bonds in IRAs, stocks in taxable accounts)

- Withdrawal strategies sequence distributions to minimize taxes and preserve assets for heirs

- Estate structures align with tax-efficient account titling and beneficiary designations

- Legacy goals inform which assets to convert to Roth, gift, or hold until death

Sentinel Asset Management has guided over 2,000 clients through retirement using this coordinated approach, ensuring every decision — from portfolio allocation to withdrawal sequencing — aligns with the client's tax situation and legacy intentions.

The Cost of Poor Coordination

Consider what poor coordination actually costs families:

- 42% of Americans wouldn't know what to do if a family member died today

- More than 40% have never updated beneficiary forms, even after major life events like marriage, divorce, or children

- 50% of trusts remain unfunded, rendering them legally ineffective

These coordination failures cost families thousands in avoidable taxes, probate fees, and legal disputes.

Who Needs Estate Planning and Tax Advisory Services?

The Myth of "Only for the Wealthy"

Estate planning isn't just for millionaires. You need a coordinated plan if you have:

- Retirement accounts (IRAs, 401(k)s)

- A home or other real estate

- Dependents who rely on you

- Specific wishes about how your assets transfer

- Any desire to minimize taxes and avoid probate

The numbers back this up. 54.3% of U.S. families hold retirement accounts, and 20% of adults 50+ have no retirement savings — meaning the other 80% do. If you're in that majority, estate and tax planning directly affects you.

Waiting creates unnecessary risk. 62% of Gen X adults have no estate planning documents, leaving families vulnerable to state intestacy laws, avoidable taxes, and court interference.

Three Life Situations That Demand Urgent Planning

Approaching or Entering Retirement

Tax-efficient withdrawal strategies become critical when you transition from accumulation to distribution. Drawing from the wrong account at the wrong time can push you into higher tax brackets, trigger Medicare premium surcharges, and prematurely deplete your estate.

Families with Special Needs Dependents

Direct inheritances can disqualify disabled dependents from government benefits. SSI eligibility requires countable resources below $2,000, and giving away resources can result in ineligibility for up to 36 months.

Special needs trusts (SNTs) protect your loved one's benefits while ensuring lifetime care. Yet only 23% of caregivers have a formal financial plan, and 67% lack an established SNT.

Sentinel Asset Management brings 25+ years of experience working with families navigating special needs planning, having supported more than 20 families long-term.

Life Transitions: Divorce or Inheritance

Divorce requires rapid re-evaluation of all beneficiary designations and estate documents. Failing to update after divorce can result in an ex-spouse legally receiving retirement or life insurance assets, since beneficiary forms override divorce decrees and wills.

Receiving an inheritance raises a different set of concerns: tax-efficient management and integration with your existing estate plan both need attention before decisions are made.

How a Financial Advisor Coordinates Your Estate Plan and Tax Strategy

The Advisor as Quarterback

A skilled financial advisor acts as the central coordinator of your estate and tax planning process, reviewing:

- All accounts and their titling

- Beneficiary designations across retirement accounts, insurance policies, and transfer-on-death accounts

- Investment allocations across tax categories

- Insurance coverage and ownership structures

- Existing wills, trusts, and legal documents for consistency

When these elements align, your plan works as a unified system rather than a collection of disconnected decisions.

The Investment Policy Statement: Your Financial Blueprint

The Investment Policy Statement (IPS) is the operational blueprint for your entire financial plan. Unlike a generic risk tolerance questionnaire, a robust IPS factors in:

- Tax situation: Account location strategy, anticipated tax brackets, conversion opportunities

- Income needs: Distribution rates, withdrawal sequencing, inflation protection

- Legacy goals: Wealth transfer timelines, charitable intentions, heir education

The IPS becomes the living document that guides portfolio construction, rebalancing decisions, and tax-efficient withdrawals throughout your retirement.

Structured Withdrawal Planning and Estate Reduction

How you sequence distributions from different account types directly impacts both your lifetime tax bill and your taxable estate.

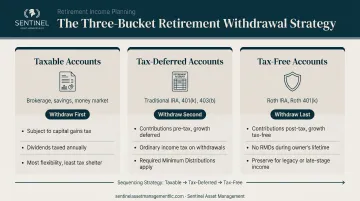

Example: The "Bucket" Strategy

Sentinel organizes client assets across three tax categories:

- Taxable accounts (brokerage, savings)

- Tax-deferred accounts (traditional IRAs, 401(k)s)

- Tax-free accounts (Roth IRAs, Roth 401(k)s)

By drawing from taxable accounts first during early retirement, clients:

- Reduce the gross taxable estate (assets spent are no longer subject to estate tax)

- Delay or minimize Required Minimum Distributions (RMDs) from tax-deferred accounts

- Preserve tax-free accounts for heirs, who inherit them without future tax liability

This sequencing can save families tens of thousands in taxes over a 20-30 year retirement.

What a Financial Advisor Handles Without an Attorney

Most estate planning doesn't require an attorney. A skilled financial advisor can handle:

- Beneficiary designation review and coordination

- Account titling alignment

- Roth conversion planning and execution

- Strategic gifting strategies

- Asset location optimization across tax categories

Attorneys are reserved for specific legal instruments like:

- Drafting or updating wills and trusts

- Creating powers of attorney and healthcare directives

- Complex trust structures (charitable remainder trusts, multi-generational trusts)

This division of labor reduces costs and simplifies the process for most families. Sentinel's approach covers the coordination of accounts, insurance policies, and ownership structures, while bringing in estate attorneys when complex legal instruments are required.

Coordinating with Other Professionals

The best advisors work directly with your other professionals—estate attorneys and CPAs—while acting as the central point of continuity.

This prevents a common and costly problem : when professionals operate in silos, where:

- Tax-loss harvesting strategies go unrecognized by your CPA at filing time

- A new trust gets drafted without your advisor's knowledge or input

- Your beneficiary designations contradict your will because no one coordinated them

When your advisor serves as the central point of continuity, every professional—attorney, CPA, and planner—operates from the same picture of your financial life.

Key Tax Strategies Embedded in Estate Planning

Strategic Gifting: Use It or Lose It

Annual Gift Tax Exclusion: You can give $19,000 per person per year (2025) without triggering gift tax or using your lifetime exemption. Married couples can give $38,000 per recipient.

This is a use-it-or-lose-it opportunity. You can't "catch up" on missed years.

Example: A couple with two children and four grandchildren can gift $228,000 annually ($19,000 × 6 recipients × 2 spouses) without any tax consequences, reducing their taxable estate by over $2 million in a decade.

Lifetime Exemption: The basic exclusion amount is $13.99 million for 2025, but this is scheduled to be drop roughly in half in 2026 when current tax law sunsets. Families with estates approaching or exceeding this threshold should consider accelerated gifting strategies before the exemption drops.

Beyond annual transfers, how your retirement accounts are structured can be just as consequential for the people you leave behind.

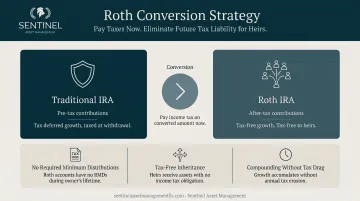

Roth Conversion Planning: Pay Taxes Now, Save Later

A Roth conversion moves pre-tax IRA money into a Roth IRA. You pay income tax now, but eliminate:

- Future taxes on growth and withdrawals

- Required Minimum Distributions (RMDs)

- Taxable income for your heirs

The SECURE Act requires most non-spouse beneficiaries to fully distribute inherited IRAs within 10 years, often during their peak earning years — compressing a decade of taxable income into a window where heirs are least equipped to absorb it.

By converting during lower-income years (early retirement, before RMDs begin, or after a market downturn), you:

- Pay taxes at your lower rate instead of your heirs' higher rate

- Reduce the taxable estate

- Pass tax-free assets that grow without future tax liability

Conversions must be balanced against current tax brackets and Medicare premium thresholds (IRMAA). Converting too much in one year can push you into a higher bracket or trigger premium surcharges — so sequencing matters as much as the decision to convert.

Once your account structure is optimized, the next question is what goes where.

Asset Location: The Right Assets in the Right Accounts

Not all investments are taxed the same way. Strategic asset location means placing:

- Tax-inefficient assets (bonds, REITs, actively managed funds) in tax-advantaged accounts (IRAs, 401(k)s)

- Tax-efficient assets (index funds, ETFs, individual stocks held long-term) in taxable accounts

Vanguard research shows this strategy can add 5 to 30 basis points of after-tax return annually—that's $500 to $3,000 per year on a $1 million portfolio. Compounded over 20–30 years, that differential alone can mean $30,000–$90,000 more reaching your heirs — without changing a single investment.

Asset location shapes how much you keep during your lifetime. The step-up in basis rules determine what your heirs keep after you're gone.

Step-Up in Basis: Hold vs. Gift

The Rule: When you inherit property, the basis resets to fair market value at the date of death. This "step-up in basis" eliminates capital gains tax on appreciation during the decedent's lifetime.

Example:

- You bought stock for $50,000 that's now worth $200,000

- If you gift it during life, your heir inherits your $50,000 basis (carryover basis). When they sell, they owe capital gains tax on $150,000

- If you hold until death, your heir inherits at $200,000 stepped-up basis. They can sell immediately with zero capital gains tax

Exception: Appreciated property gifted to you within one year of death and passed back to the original donor doesn't receive step-up.

For highly appreciated assets, holding until death is more tax-efficient than gifting during life. For assets with little appreciation — or gifts within the annual exclusion — gifting during life reduces the taxable estate without sacrificing tax efficiency.

What to Look for in an Estate Planning and Tax Advisory Advisor

Fiduciary Status: Non-Negotiable

A fiduciary advisor is legally required to act in your best interest. This is a meaningful legal distinction: non-fiduciary brokers are only required to recommend "suitable" products, which may still earn them higher commissions at your expense.

Under federal law, investment advisers owe clients a duty of care and duty of loyalty, and must not subordinate client interests to their own.

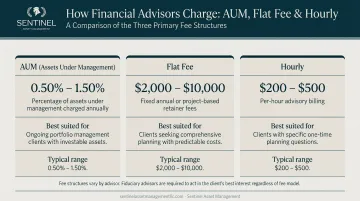

Fee Transparency: Know What You're Paying

Advisors are compensated through different models:

Fee-Only: Paid exclusively by clients (AUM percentage, flat fee, or hourly rate). No commissions, no product sales incentives.

Fee-Based: May charge fees and also earn commissions on product sales. Creates potential conflicts of interest.

Research shows that broker-sold funds earn roughly 0.8% lower returns annually after adjusting for risk, and savers receiving conflicted advice earn roughly 1% lower returns each year.

Industry Benchmarks:

| Fee Structure | Typical Range |

|---|---|

| AUM fee (overall median) | 0.59% - 1.18% |

| AUM fee ($1M portfolio) | ~1.00% |

| AUM fee ($2M portfolio) | 0.75% - 1.00% |

| Flat annual fee | ~$3,000 |

| Hourly rate | ~$300 |

Source: SmartAsset industry survey

Note: AUM fees generally decrease as portfolio size increases, with $1 million often serving as a breaking point.

Relevant Credentials

Look for credentials like:

- CFP (Certified Financial Planner): Comprehensive financial planning training and ethics requirements

- CPA (Certified Public Accountant): Tax expertise

- Certified Financial Fiduciary®: Specific fiduciary training and commitment

Credentials matter, but they're not the whole picture. Experience with estate and tax planning, client references, and the ability to coordinate across disciplines carry equal weight.

The Value of In-Person, Relationship-Based Advisory

Estate and legacy planning carry significant emotional weight. These decisions benefit from trust built over time — not one-off virtual consultations or robo-advisor algorithms.

An advisor who knows your family, understands your values, and has guided you through market cycles and life transitions provides consistency across decades of planning decisions.

Sentinel Asset Management maintains 5 offices across the U.S. — with locations in Connecticut and Maryland — and serves clients across nine states, backed by 100+ years of combined advisory experience among its team.

Frequently Asked Questions

What is a normal fee for a financial advisor to charge?

Typical fee structures include AUM-based fees (1% annually on a $1 million portfolio), flat annual fees ($3,000), or hourly rates (~$300). AUM fees generally decrease for larger portfolios. Fee-only models may be more economical for larger estates.

Can a financial advisor help with estate planning?

Yes—a financial advisor can handle the majority of estate planning strategy, including beneficiary designations, account titling, tax-efficient withdrawal sequencing, and gifting strategies. Advisors coordinate with estate attorneys when specific legal documents like trusts or wills are required.

When should you start estate planning?

The best time is before a major life event forces the issue—ideally when approaching retirement, after acquiring significant assets, or when a dependent's long-term care needs become apparent. Waiting until a crisis hits often means higher probate exposure, unintended asset distribution, and fewer options.

What is the difference between estate planning and tax planning?

Estate planning focuses on how assets transfer at death and are preserved during life. Tax planning focuses on minimizing ongoing and future tax liability. The two deliver the most value when they work together under one plan.

What happens if you don't have an estate plan?

Without a plan, state intestacy laws determine asset distribution, beneficiary designations may override your intentions, and heirs may face avoidable tax burdens, probate costs, and court involvement. Your wishes may not be honored.

What does a financial advisor do differently from an estate attorney?

An attorney drafts legal documents—wills, trusts, powers of attorney. A financial advisor handles the surrounding financial strategy: account titling, tax-efficient transfers, and beneficiary alignment that make those documents work in practice.

Take the next step in your financial journey by exploring our courses page for upcoming live seminars.