General information, not personalised tax, legal or investment advice.

Introduction

Retirement marks a fundamental shift: your paycheck stops, but your bills don't. For most Americans, replacing 70–90% of pre-retirement income is the standard benchmark — yet it's a poor fit for most households. According to Vanguard and JP Morgan data, households earning $30,000 need to replace 104% of income, while those earning $196,000 need only 44%.

Those numbers reveal the real challenge: retirement income planning isn't just about saving more — it's about building a strategy matched to your actual spending needs.

That means shifting from the accumulation phase (saving as much as possible) to the distribution phase, where the goal is turning a lump sum into reliable, lasting monthly income. Many retirees are surprised to find that a large nest egg doesn't automatically produce dependable cash flow.

This article covers the core income sources available to retirees, how to sequence withdrawals strategically, and how to build a plan that holds up against inflation, longevity, and market volatility.

Key takeaways

- Most retirees draw from 3–5 income sources—no single stream covers 70–90% replacement needs alone

- Social Security, retirement accounts, pensions, annuities, and investment income each play distinct roles requiring strategic coordination

- Withdrawal sequencing directly impacts taxes and portfolio longevity; the order of distributions matters as much as the amounts

- Diversified income balances guaranteed sources (Social Security, pensions) with growth-oriented assets (portfolio withdrawals, dividends) to fight inflation and longevity risk

- Stress-testing a retirement plan against market crashes, inflation spikes, and healthcare costs confirms it can hold up under real-world conditions

Why Your Retirement Needs a "Paycheck" Strategy — Not Just Savings

The Psychological and Financial Shift

Having $500,000 saved feels secure—until you realize it doesn't produce automatic monthly income like a paycheck did. The predictability of bi-weekly deposits during working years contrasts sharply with managing multiple income streams in retirement. Many retirees experience anxiety when transitioning from accumulation to distribution, unsure how to draw income without depleting assets too soon.

Four Critical Risks Your Strategy Must Address

That anxiety has a root cause: retirement exposes you to several compounding financial risks that a single savings account can't offset. Each one demands a deliberate response.

- Longevity risk — A 65-year-old couple has a 46.7% probability that at least one spouse reaches age 90, meaning your income plan may need to hold for 25–30+ years.

- Inflation risk — At a steady 3% inflation rate, a fixed income stream loses 44.6% of its real value over 20 years and 58.8% over 30 years.

- Sequence of returns risk — Retiring into a bear market can be devastating. Vanguard research shows two retirees with identical average returns but different return sequences can end up with vastly different outcomes — one portfolio depleted by year 23, the other holding a $300,000 balance at year 35.

- Healthcare cost risk — Fidelity estimates a 65-year-old retiring in 2025 will spend $172,500 on healthcare alone, excluding long-term care and dental.

Relying on a single income source leaves all four of these risks unaddressed. A retirement paycheck is a coordinated system — multiple, complementary income streams working together to replicate the security of a working paycheck, built to last often spanning three decades.

The Core Income Sources for Your Retirement Paycheck

Most retirees draw from a mix of 3–5 income sources. Understanding what each provides—and its limitations—is essential to building a complete picture.

Social Security

Social Security forms the foundation for most Americans, but it was never designed to be the only source. Benefits provide at least 50% of income for roughly half of retirees, and 90%+ for about one-quarter.

Benefits are calculated from your earnings history, with a critical timing decision: when to claim. Claiming at age 62 results in a permanent 30% reduction. Delaying past Full Retirement Age (FRA) increases monthly payments by 8% per year up to age 70.

Example: If your FRA benefit is $2,000/month:

- Claiming at 62: $1,400/month (30% reduction)

- Claiming at 67 (FRA): $2,000/month

- Claiming at 70: $2,480/month (24% increase)

That $1,080 monthly difference ($2,480 vs. $1,400) adds up to nearly $13,000 annually in guaranteed, inflation-adjusted income for life. For married couples, coordinating spousal claiming strategies can meaningfully increase lifetime household benefits. Timing decisions should factor in health, other income sources, and expected longevity.

Yet 57% of new beneficiaries still claim before age 66, locking in permanent reductions.

Workplace Retirement Accounts (401(k), 403(b), IRA, Roth IRA)

These accounts shift from accumulation vehicles to distribution tools in retirement. The key difference: traditional (pre-tax) accounts are taxed as ordinary income upon withdrawal, while Roth accounts offer tax-free qualified withdrawals. This distinction has major implications for tax planning.

Required Minimum Distributions (RMDs) begin at age 73 under SECURE 2.0, forcing withdrawals whether you need the money or not. Failing to plan for them can push you into higher tax brackets unexpectedly. Early in retirement, forgoing unnecessary withdrawals allows assets to compound longer.

Once RMDs kick in, you lose that flexibility. The penalty for missing one was reduced from 50% to 25% (or 10% if corrected quickly), but the tax bite remains significant when stacked atop Social Security and other income.

Pension Plans

Defined benefit pensions—more common among public sector employees, teachers, and union workers—provide guaranteed monthly payments for life based on years of service and salary. 86% of state and local government workers have access to pensions, compared to only 14% of private-sector workers.

The key decision for pension holders: lump sum versus monthly payments. Factors influencing this choice include:

- Health and expected longevity

- Other guaranteed income sources

- Spouse's financial needs and survivor benefit options

- Debt obligations

- Tax implications

Monthly annuity payments offer guaranteed income and PBGC protection up to certain limits if your plan fails—protection you forfeit when taking a lump sum.

Annuities

Annuities are insurance products that convert a lump sum into guaranteed lifetime income, creating a pension-like stream you cannot outlive. Approximately 30% of retirees own an annuity, and retail annuity sales hit a record $434.1 billion in 2024.

Types:

- Immediate annuities: Payments begin within 12 months of purchase, ideal for covering current expenses

- Deferred annuities: Payments begin at a future date, allowing the account to grow in the interim

Trade-offs: Annuities offer security but come with fees, reduced liquidity, and limited flexibility. Guarantees are subject to the claims-paying ability of the issuing insurer. State guaranty associations typically cap protection at $250,000 per life, unlike federal FDIC insurance.

Annuities make the most sense when guaranteed income sources (Social Security plus any pension) don't fully cover essential living expenses. They're not right for everyone—if you already have sufficient guaranteed income or need portfolio flexibility, annuities may not add value.

Investment Income (Dividends, Interest, and Capital Gains)

While guaranteed products cover essential expenses, a well-diversified investment portfolio fills the gap with income you don't have to manufacture by selling assets. Dividends from stocks, interest from bonds, and fund distributions all contribute. Dividend-paying stocks help hedge inflation when payouts grow over time.

Bond ladders add another layer of predictability: bonds with staggered maturity dates generate recurring cash flow, and as each matures, the principal reinvests at current rates—managing both interest rate and reinvestment risk. Together, these sources complete the income mix most retirees need.

Supplemental Income Streams Worth Considering

Part-Time Work or Consulting

Many retirees continue earning through consulting, freelancing, or part-time work they enjoy. Earned income delays the need to tap retirement accounts—letting them grow longer—and can allow Social Security to be deferred for a higher monthly benefit.

A few caveats to keep in mind:

- Earned income before full retirement age can temporarily reduce Social Security benefits

- Wages are taxed at ordinary income rates, unlike most investment withdrawals

Rental Income

Owning rental property provides steady monthly cash flow, especially if the mortgage is paid off. The trade-offs are real, though:

- Hands-on management (or the cost of hiring a property manager)

- Illiquidity — you can't sell a bedroom to cover a bad month

- Income that varies with vacancies, repairs, and market conditions

REITs offer real estate exposure without direct ownership, trading some upside for far more liquidity.

Health Savings Accounts (HSAs) as a Hidden Income Source

If you contributed to an HSA during working years, those funds can stretch further in retirement than most people realize — covering healthcare costs without touching Social Security, portfolio withdrawals, or other income sources. HSAs provide a triple tax advantage: deductible contributions, tax-free growth, and tax-free qualified withdrawals.

After age 65, HSA funds can be used for any purpose (taxed as ordinary income, similar to a traditional IRA), making them flexible assets that serve double duty — healthcare reserve first, supplemental income if needed.

The Withdrawal Strategy That Makes Your Money Last

Deciding which income sources to tap first—and when—is as important as what those sources are. A poorly sequenced withdrawal strategy increases taxes, triggers higher Medicare premiums, and shortens portfolio life.

Tax-Efficient Sequencing

The conventional approach: draw from taxable accounts first (brokerage accounts), then tax-deferred accounts (traditional 401(k)/IRA), and finally tax-free accounts (Roth IRA). This preserves tax advantages longest.

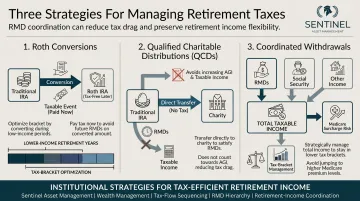

However, the right sequence depends on your specific tax situation. Roth conversions in lower-income early retirement years can be powerful. Vanguard's BETR framework shows conversions can add wealth even if future tax rates are lower, especially when conversion taxes are paid from taxable accounts.

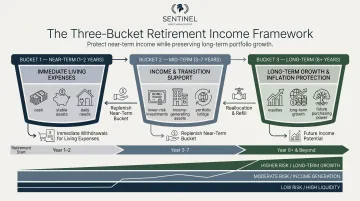

The Bucket Strategy

The bucket framework manages income during retirement without forcing you to sell growth assets during market downturns. Structure:

- Near-term bucket (1–2 years): Cash or stable assets covering immediate expenses

- Mid-term bucket (3–7 years): Lower-risk investments bridging to long-term growth

- Long-term bucket (8+ years): Equities and growth assets for future needs

Sentinel Asset Management builds this structure into client portfolios, designed to insulate near-term cash flow from market volatility so retirees never need to sell investments at the worst possible time.

Sequence of Returns Risk

The bucket structure exists for one specific reason: sequence of returns risk. Selling investments when the market is down—especially early in retirement—permanently reduces portfolio longevity because fewer shares remain to recover when markets rebound.

Vanguard's case study illustrates this starkly: two investors retire with $500,000 and withdraw $25,000 annually (inflation-adjusted), experiencing identical long-term average returns. The 1973 retiree, facing an immediate bear market, depleted their portfolio in 23 years. The 1974 retiree maintained a $300,000 balance 35 years in.

The difference? The order of returns, not the average. Reverse dollar-cost averaging—selling more shares at low prices during downturns—cripples recovery.

Managing RMDs and Tax Brackets

Required Minimum Distributions begin at age 73, stacking atop Social Security and investment income to push retirees into higher tax brackets. Strategies to manage this:

- Roth conversions in earlier retirement years: Convert traditional IRA assets to Roth when income is lower, paying taxes at favorable rates

- Qualified Charitable Distributions (QCDs): Transfer up to $108,000 (for 2025) directly from an IRA to charity, satisfying RMDs without adding to AGI

- Coordinated withdrawal amounts: Stay within target tax brackets by managing total income across all sources

Unmanaged RMDs can trigger stealth taxes like the 3.8% Net Investment Income Tax (NIIT) for modified AGI over $200,000 (single) or $250,000 (joint).

Building a Resilient Retirement Income Plan

How Much Income Do You Actually Need?

The 70–90% replacement rule is a useful starting point, but actual needs vary widely based on lifestyle, debt, healthcare costs, and whether you're still paying a mortgage. Research by David Blanchett identifies a "retirement spending smile"—spending tends to decline in mid-retirement but spikes again for healthcare in late retirement.

That pattern matters for how you allocate resources across early, mid, and late retirement — not as a one-size-fits-all budget, but as a phased strategy.

Planning for Inflation and Longevity

A retirement lasting 25–30 years means even modest inflation significantly erodes purchasing power. At 3% annual inflation, a fixed income stream loses 44.6% of its real value over 20 years and 58.8% over 30 years.

Guaranteed sources like Social Security (which includes annual COLA adjustments averaging 2.55% over 20 years) offer partial protection. Inflation-adjusted annuities provide similar benefits, but most fixed income sources don't keep pace with inflation—making growth-oriented assets essential even in retirement.

Stress-Testing Your Plan

Run "what-if" scenarios before and throughout retirement:

- What happens if markets drop 30% in year two?

- What if one spouse needs long-term care at 80?

- What if inflation averages 4% rather than 2%?

A well-constructed plan should withstand these stresses without requiring dramatic lifestyle changes. Sentinel Asset Management stress-tests each retirement plan against historical bear markets, recessions, and inflationary periods to ensure resilience. Advisors monitor the full landscape—portfolio variance, healthcare inflation, property tax trends, and long-term income gaps—so when markets shift, plans flex without panic.

How a Financial Advisor Can Help

Building and maintaining a retirement paycheck strategy is complex. It requires coordinating several moving parts simultaneously:

- Tax planning across account types and withdrawal sequences

- Investment management aligned to income needs and risk tolerance

- Social Security timing to maximize lifetime benefits

- Estate considerations to protect what transfers to heirs

Sentinel Asset Management's advisors bring 100+ years of combined experience and have guided 2,000+ clients through retirement.

The firm uses personalized Investment Policy Statements and a PRIME risk framework — Purchasing Power, Reinvestment, Interest Rate, Market, and Exchange Risk — to build portfolios calibrated to endure. Every withdrawal sequence, account type, and timing decision is structured to preserve independence and quality of life, regardless of how markets behave or how long you live.

Frequently Asked Questions

How to set up a retirement income stream?

Setting up a retirement income stream involves identifying all available sources (Social Security, retirement accounts, pensions, investments), determining a tax-efficient withdrawal sequence, and aligning income timing with expense needs—ideally with guidance from a financial advisor who can coordinate these moving parts.

What is the best income stream for retirement?

The most effective strategy combines guaranteed sources (Social Security, pension, annuities) for essential expenses with market-based sources (portfolio withdrawals, dividends) for discretionary spending. No single source works in isolation—a diversified plan balances security with growth potential.

What are some retirement income strategies?

Common strategies include:

- Bucket approach: segregate assets by time horizon (short, mid, long-term)

- Withdrawal sequencing: draw from taxable, tax-deferred, and tax-free accounts in a deliberate order

- Delay Social Security to age 70 to maximize monthly benefits

- Roth conversions during low-income years to reduce future tax exposure

- Annuities to guarantee a baseline income for life

What is the biggest mistake most people make regarding retirement?

The most common mistake is focusing only on accumulation without a distribution strategy. Without a clear plan for converting savings into reliable monthly income, retirees risk poor tax outcomes and premature depletion of their portfolio.

How long will $750,000 last in retirement at 62?

The answer depends on withdrawal rate, investment returns, other income sources, and inflation. Using the 4% rule, $750,000 would generate approximately $30,000 per year—which is why most retirees need additional income sources (Social Security, part-time work, pensions) to cover living expenses comfortably.

Can you live off $3,000 a month in retirement?

$3,000 per month can work in lower cost-of-living areas for retirees with paid-off homes and modest healthcare costs. The bigger question is whether that amount holds up against inflation over a 20–30 year retirement.

Take the next step in your financial journey by exploring our courses page for upcoming live seminars.