General information, not personalised tax, legal or investment advice.

Introduction

Most people spend 30 or 40 years building wealth through their careers, yet nearly one in four Americans have never updated their estate plan since creating it, and many lack basic documents entirely. Without a coordinated preservation and estate plan, a significant portion of accumulated wealth can erode through estate taxes, legal costs, creditor claims, or inefficient transfer structures.

Wealth preservation and estate planning serve distinct but inseparable roles. One protects assets from inflation, market risk, and taxes during your lifetime; the other ensures those assets reach the right people efficiently and on your terms after you're gone.

A well-diversified portfolio left without proper estate documents can be tied up in probate or taxed heavily. Conversely, a carefully structured estate built around a weak investment base may not have enough value left to transfer.

Addressing both sides together closes that gap. This guide covers eight strategies spanning financial planning and estate planning — relevant whether you're approaching retirement, already there, or building a multi-generational legacy.

Key takeaways

- Wealth preservation maintains purchasing power; estate planning controls how and to whom assets transfer—both are essential

- Eight core strategies span estate documents, trusts, tax-advantaged gifting, diversification, retirement accounts, insurance, charitable giving, and legacy planning

- Starting a decade before retirement dramatically expands your planning options and tax efficiency

- A coordinated plan covers investment strategy, tax minimization, asset protection, and distribution in one approach

- A fiduciary advisor who integrates financial and legal dimensions ensures your wealth reaches the right people, on your terms

What Is Wealth Preservation and Estate Planning?

The distinction matters: wealth preservation focuses on protecting and maintaining the real value of assets against inflation, market volatility, and tax drag over time. Estate planning focuses on the legal and financial structures that govern how assets are managed if you're incapacitated and distributed when you die.

The two must work together. A well-diversified portfolio left without proper estate documents can be tied up in probate for months or taxed at rates approaching 40% in some states. That same problem runs in reverse: estate structures built around a weak investment base may have little left to transfer if inflation and poor returns have already eroded purchasing power.

According to 2025 data from Caring.com, nearly one in four Americans have not updated their estate documents since creation, and many have no documents at all. This inaction leaves families vulnerable to state intestacy laws, probate court delays, and preventable tax exposure.

The tools available range widely depending on your situation:

- Simple wills and beneficiary designations for straightforward estates

- Revocable and irrevocable trusts for privacy and probate avoidance

- Annual gifting strategies and Qualified Charitable Distributions for tax efficiency

- Business succession plans for owners with operating companies

The right combination depends on your goals, asset complexity, family circumstances, and state of residence. This last factor matters more than most people realize — 12 states and the District of Columbia impose their own estate taxes with thresholds as low as $1 million.

8 Key Strategies for Wealth Preservation and Estate Planning

Strategy 1: Establish Your Core Estate Planning Documents

No advanced strategy works without a foundation. You need:

- A will

- Durable power of attorney

- Healthcare proxy/directive

- For most households, a revocable living trust

Without these, courts and state law decide outcomes—not you. These documents serve both lifetime incapacity planning and post-death distribution. If you become incapacitated without a healthcare directive and power of attorney, family members may face costly guardianship proceedings to make decisions on your behalf.

Beneficiary Designations Are Often Overlooked

Retirement accounts, life insurance policies, and transfer-on-death (TOD) accounts pass directly to named beneficiaries, bypassing your will entirely. Misaligned beneficiary designations are a common source of unintended outcomes—such as an ex-spouse receiving your IRA or a child being excluded because you forgot to update the form after a life change.

Sentinel Asset Management reviews titling, beneficiary designations, wills, and trusts for consistency and alignment as part of its comprehensive estate planning coordination, ensuring that what you intend matches what will actually happen.

Strategy 2: Use Trusts to Protect and Transfer Assets

Trusts solve different problems depending on their structure.

Revocable Trusts provide:

- Probate avoidance

- Privacy (trusts aren't public record)

- Seamless management during incapacity

- Flexibility to amend or revoke

Irrevocable Trusts provide:

- Estate tax reduction

- Creditor protection

- Removal of assets from your taxable estate

- The tradeoff: you give up control in exchange for legal and tax benefits

Specialized Irrevocable Trust Structures:

- Irrevocable Life Insurance Trusts (ILITs): Remove life insurance death benefits from your taxable estate while providing liquidity to pay estate taxes or support heirs

- Spousal Lifetime Access Trusts (SLATs): Allow one spouse to transfer assets out of their estate while the other spouse retains indirect access to funds during lifetime

- Qualified Personal Residence Trusts (QPRTs): Transfer your home to heirs at a reduced gift tax value while retaining the right to live there for a set term

Dynasty and Generation-Skipping Trusts

For families looking to extend wealth across multiple generations, dynasty trusts shelter assets from estate taxes at each generational transfer. They can include provisions protecting beneficiaries from creditors or divorcing spouses, preserving family wealth through decades of transitions.

Strategy 3: Maximize Tax-Advantaged Gifting

Strategic gifting reduces your taxable estate while transferring wealth during your lifetime.

Annual Gift Tax Exclusion

For 2025, you can gift up to $18,000 per recipient per year without using any of your lifetime exemption. For married couples, that doubles to $36,000 per recipient. Consistent annual gifting to multiple family members compounds significantly over time and can be directed into 529 education accounts for tax-free education funding.

Federal Lifetime Gift and Estate Tax Exemption

The current federal exemption stands at $13.99 million per individual (effectively $27.98 million per married couple). However, this historically high exemption is scheduled to sunset on December 31, 2025, reverting to approximately $7 million per person (adjusted for inflation).

Individuals with larger estates should be making strategic use of this exemption now by transferring appreciating assets into trusts or making direct gifts before the window closes. Delaying this planning significantly narrows available options.

Family Limited Partnerships (FLPs)

For families with business interests or substantial investment portfolios, FLPs allow you to transfer assets to family members while retaining management control. Valuation discounts for lack of marketability and minority interest mean more wealth transfers per dollar of exemption used—improving the efficiency of your overall gifting strategy.

Strategy 4: Diversify Your Investment Portfolio Against Multiple Risks

Wealth preservation requires your portfolio to outpace inflation over a multi-decade retirement while managing downside risk. A portfolio that is too conservative loses purchasing power; too aggressive creates sequence-of-returns risk—the danger that poor market performance early in retirement depletes assets before recovery occurs.

The PRIME Risk Framework

Sentinel Asset Management addresses five systematic risks that no investor can avoid through diversification alone:

- Purchasing Power Risk: Inflation erodes the real value of fixed income withdrawals

- Reinvestment Risk: Maturing investments must be reinvested at potentially lower rates

- Interest Rate Risk: Rising rates reduce bond values, forcing difficult timing decisions

- Market Risk: Systematic declines affect all equities regardless of individual company performance

- Exchange Risk: Currency fluctuations reduce the dollar value of international holdings

Structured Withdrawal Buckets

Sentinel's approach pairs near-term cash flow insulation against market volatility with growth-oriented allocations for longer horizons. Conservative, liquid allocations cover immediate needs without requiring forced sales during market downturns. Longer-term buckets can weather market cycles because they have time before those funds are needed.

Each plan is stress-tested against historical bear markets, recessions, and inflationary periods to confirm the strategy holds under unexpected conditions.

Strategy 5: Fully Leverage Retirement Accounts

Retirement accounts provide multi-layered value in wealth preservation:

- Tax-deferred or tax-free growth

- Reduced taxable income during accumulation

- Legal protections from creditors in many states

- Meaningful flexibility in legacy planning (especially Roth accounts passing income tax-free to heirs)

Roth Conversions as Strategic Moves

Converting tax-deferred balances to Roth IRAs during lower-income years reduces future required minimum distribution (RMD) exposure and creates a tax-free inheritance for beneficiaries. This strategy is particularly powerful in the gap between retirement and age 73, when RMDs begin. You may be in a lower bracket than during your working years—and almost certainly lower than your heirs will face when they inherit.

Asset Location Strategy

Holding tax-inefficient assets (such as bonds generating ordinary income or actively managed funds with high turnover) inside tax-advantaged accounts while holding tax-efficient assets (such as index funds or municipal bonds) in taxable accounts maximizes after-tax returns across your entire portfolio.

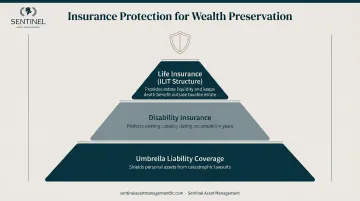

Strategy 6: Protect Assets with the Right Insurance Coverage

Insurance is the first line of defense in wealth protection:

Life Insurance

Permanent life insurance held inside an Irrevocable Life Insurance Trust (ILIT) keeps the death benefit outside your taxable estate while providing liquidity to heirs for estate taxes, income replacement, or legacy funding.

Disability Insurance

Protects your earning capacity—your most valuable asset during accumulation years. Without disability coverage, a health event can derail decades of wealth-building progress.

Umbrella Liability Coverage

Shields personal assets from lawsuits exceeding standard homeowners or auto policy limits. A $1-2 million umbrella policy typically costs just a few hundred dollars annually and protects against catastrophic liability claims that could otherwise wipe out your estate.

The right insurance strategy is not just about coverage amounts but about policy structure—ensuring that insurance integrates cleanly with your overall wealth preservation and estate plan.

Strategy 7: Incorporate Charitable Giving Strategies

Charitable tools serve dual purposes: advancing philanthropic goals while reducing taxable estate size.

Charitable Remainder Trusts (CRTs)

Provide income to you during your lifetime with the remainder going to charity after death, removing assets from your taxable estate. This structure is particularly effective when funded with highly appreciated assets, as it bypasses capital gains tax while generating a charitable deduction.

Charitable Lead Trusts (CLTs)

Provide income to charity for a set term, with the remainder passing to heirs at reduced transfer tax cost. This strategy works well when interest rates are low, maximizing the value that ultimately transfers to family members.

Donor-Advised Funds (DAFs)

A simpler, more flexible alternative that allows you to take an immediate charitable deduction while retaining the ability to recommend grants to charities over time. DAFs are ideal for managing irregular income (such as bonuses or stock options) by bunching deductions in high-income years.

Across all three structures, pairing charitable vehicles with appreciated assets delivers the greatest combined tax and transfer benefit.

Strategy 8: Plan for Business Succession and Multi-Generational Legacy

For business owners, a business interest is often the largest and most illiquid asset in the estate. Without a succession plan, forced sales, family disputes, or estate tax bills can destroy decades of built value.

Essential Components of Business Succession:

- Documented succession plan identifying who will lead the business

- Buy-sell agreements funded by life insurance to provide liquidity

- Gradual ownership transfer using gifting or Grantor Retained Annuity Trusts (GRATs) to minimize transfer taxes

Legacy Planning Beyond Business Ownership

Estate planning is ultimately about values, not just assets. Tools that help ensure wealth is preserved and purposefully used across generations include:

- Family governance: Regular meetings and financial education for heirs

- Incentive trusts: Distributions tied to milestones like education, career achievement, or charitable contributions

- Written legacy statement of intent: Articulates your values and intentions to guide future generations

Sentinel Asset Management helps families establish multi-generational structures that empower heirs while preserving the values that created the wealth in the first place.

How to Choose the Right Strategies for Your Situation

No two wealth preservation plans are identical. The right mix depends on:

- Estate size and asset types (liquid vs. illiquid, business ownership, real estate)

- Family structure (blended families, special needs dependents, minor children)

- State of residence—12 states impose estate taxes with thresholds ranging from $1 million in Oregon to $13.99 million in Connecticut

Common Planning Mistakes to Avoid:

- Treating estate planning as a one-time event rather than an ongoing process

- Failing to align beneficiary designations with trust structures

- Underestimating the impact of state-level taxes

- Waiting until illness or death is imminent to begin advanced strategies

- Building a financial plan without coordinating it with legal documents

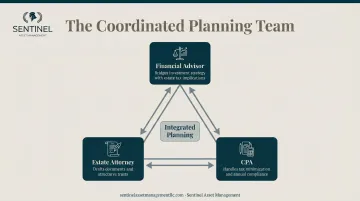

The Team-Based Approach

Comprehensive planning requires a coordinated team:

- Financial advisor: bridges investment strategy with estate planning tax implications

- Estate attorney: drafts documents and structures trusts correctly

- CPA: handles lifetime tax minimization and annual compliance

All three need to work from a shared, complete picture of your finances and goals — and that coordination is often where plans break down.

Sentinel Asset Management handles the financial coordination side of this equation, aligning investment strategy, tax efficiency, and legacy goals into a single integrated system. For complex planning instruments, the firm works alongside estate attorneys. For the financial coordination side of estate planning, Sentinel works directly with accounts, insurance policies, and ownership structures to ensure plans function exactly as intended.

Conclusion

Wealth preservation and estate planning are not separate disciplines. The most resilient plans weave investment strategy, tax efficiency, asset protection, and legacy intent into a single coordinated framework built to endure market cycles, tax law changes, and generational transitions.

If you're approaching retirement or already there, schedule a comprehensive review with Sentinel Asset Management's advisory team. With 100+ years of combined experience and 2,000+ clients guided through retirement and legacy planning across five U.S. offices, the team works with you to integrate every dimension of your financial life into one cohesive, enduring plan.

Meaningful estate planning starts with a clear understanding of your goals, your assets, and the structures that will protect both — not necessarily in a lawyer's office.

Frequently Asked Questions

What are the 5 D's of estate planning?

Per the American Bar Association Commission on Law and Aging, the five D's are Decade, Death, Divorce, Diagnosis, and Decline. Each marks a critical life transition where reviewing and updating your estate documents is essential.

What are the strategies for wealth preservation?

Core strategies include portfolio diversification across global markets, maximizing tax-advantaged retirement accounts, coordinated tax planning (Roth conversions, tax-loss harvesting), estate planning structures (trusts and beneficiary alignment), comprehensive insurance coverage, and strategic gifting. Sequencing these strategies around your tax bracket, retirement timeline, and legacy goals is what separates a plan that preserves wealth from one that merely accumulates it.

What is the difference between wealth preservation and estate planning?

Wealth preservation focuses on maintaining the value and purchasing power of assets over time through investment strategy, tax efficiency, and risk management. Estate planning covers how assets are managed during incapacity and transferred at death through legal documents, trusts, and beneficiary designations.

When should you start planning for wealth preservation and estate planning?

Planning should begin at least a decade before retirement to allow time for Roth conversions, strategic gifting, trust structures, and business succession strategies. Delaying significantly narrows available options, particularly around the federal gift and estate tax exemption, which is scheduled to sunset on December 31, 2025.

Do I need a lawyer for estate planning?

Wills, trust deeds, and complex irrevocable structures require an attorney. Most of the surrounding coordination—beneficiary alignments, retirement account structuring, gifting strategies, and insurance planning—falls within the scope of a financial advisor and doesn't require legal fees.

How often should I review my wealth preservation and estate plan?

Review every 2-3 years, or immediately after major life events: marriage, divorce, death of a beneficiary or executor, a business sale, or significant tax law changes. Caring.com's 2025 study found 62% of Americans update their plans within five years of creation.

Take the next step in your financial journey by exploring our courses page for upcoming live seminars.