General information, not personalised tax, legal or investment advice.

Introduction

More than $124 trillion will transfer between generations through 2048, according to Cerulli Associates' 2024 projections—the largest intergenerational wealth shift in history. Yet despite working lifetimes to build assets, most families spend almost no time planning how that wealth will outlive them. The result is predictable: confusion, family conflict, and wealth that dissipates within a generation.

Legacy building is not just about legal documents or account transfers. It is about intentionally passing down values, principles, and purpose alongside financial assets — and both dimensions matter equally.

When families focus solely on the legal mechanics — wills, trusts, beneficiary designations — they complete only half the work. A complete legacy defines why wealth exists and how it should serve the people who inherit it.

What follows is a practical guide to building a legacy that endures: the structures, conversations, and decisions that turn financial assets into something your family can actually carry forward.

Key takeaways

- Legacy planning goes beyond estate planning: it combines financial tools with the transfer of values, traditions, and purpose.

- A complete legacy rests on four pillars: values and life lessons, instructions and wishes, emotionally significant possessions, and financial assets.

- Wills, trusts, beneficiary designations, and powers of attorney form the legal foundation every legacy plan needs.

- Values require proactive steps to pass down: family mission statements, ethical wills, heir financial education, and honest conversations.

- The earlier you start—and the right advisors you involve—the more likely your legacy endures rather than dissolves.

Legacy Planning vs. Estate Planning: Two Sides of the Same Coin

Estate planning is the legal and financial infrastructure for managing and distributing assets. It covers what you leave and to whom—wills, trusts, beneficiary designations, and powers of attorney. The focus is technical: reducing tax exposure, avoiding probate, and ensuring assets transfer efficiently.

Legacy planning addresses the layer that estate planning cannot: why and how that wealth should serve future generations. It includes the values, wisdom, family stories, and principles you want carried forward. Legacy planning answers questions estate planning never asks—What do you hope your wealth will accomplish? What lessons do you want your heirs to remember? How can your resources reflect your purpose?

According to the Allianz American Legacies Study, a complete legacy rests on four pillars:

- Financial assets — investments, accounts, and real estate

- Personal property — meaningful possessions and heirlooms

- Values and life lessons — the principles and beliefs you want carried forward

- Instructions and wishes — guidance on how wealth should be used

Most families complete only the first pillar. When the remaining three go unaddressed, the legacy is structurally incomplete regardless of how well the estate documents are drafted.

The two approaches are complementary. Legacy planning builds on estate planning's foundation—adding the purpose and context that legal documents alone cannot convey.

The Four Pillars of a Complete Legacy

The Allianz American Legacies Study identifies four pillars that define a complete legacy:

- Values and Life Lessons

- Instructions and Wishes to Be Fulfilled

- Personal Possessions of Emotional Value

- Financial Assets and Real Estate

A legacy strategy that addresses only financial assets is structurally incomplete. Here's what each pillar entails.

Pillar 1: Values and Life Lessons

This pillar encompasses your family's ethics, faith, traditions, and the stories that define who you are and where you came from. 86% of Baby Boomers and 74% of elders rank family stories and values as the most important aspect of their legacy—far ahead of financial inheritance, valued by only 9% and 14% respectively.

Stories are particularly powerful because they capture values in ways abstract principles cannot. Consider a grandfather who started a business during the Great Depression with $50 and a borrowed truck. Retold across generations, that story becomes a living instruction about resilience and what hard work looks like under real pressure—not just as an abstract virtue, but as something witnessed and proven.

Pillar 2: Instructions and Wishes to Be Fulfilled

This pillar goes beyond end-of-life arrangements to include specific guidance on how assets should be used. Examples include:

- Stipulations in a trust that encourage education, entrepreneurship, or charitable activity

- Documented wishes about keeping a family business or property intact across generations

- Directives about caring for a loved one with special needs

- Instructions for how philanthropic resources should be deployed

These wishes turn passive asset transfer into guided decision-making, pointing heirs toward decisions that honor your intentions.

Pillar 3: Personal Possessions of Emotional Value

Intentionally designating sentimental items—and documenting the reason for that choice—transforms ordinary objects into cherished heirlooms. A grandmother's wedding ring, a handwritten recipe book, a grandfather's toolbox—these items carry meaning that no dollar amount captures.

Writing out why you're passing a specific item to a specific person prevents family disputes and adds context that deepens the gift's significance.

Pillar 4: Financial Assets and Real Estate

The emotional pillars above create the meaning behind a legacy. This one determines whether it actually reaches the people you intended. Minimizing taxes, avoiding probate, and ensuring assets transfer efficiently are all critical execution points.

Sentinel Asset Management's approach covers the financial coordination side—tax-efficient portfolios, structured withdrawal planning, and estate strategies—so that wealth reaches heirs on the client's terms. The firm organizes assets across taxable, tax-deferred, and tax-free accounts, coordinates beneficiary designations, and collaborates with estate attorneys to design trusts that minimize tax exposure and avoid unnecessary probate.

Building the Financial Foundation: Essential Estate Planning Tools

Without the right legal and financial tools in place, even the most intentional values-based planning can be undermined by taxes, probate, family disputes, or poor asset management. This section outlines the structural backbone of any legacy plan.

Wills and Trusts

A will is the foundational document that names beneficiaries, designates an executor, and provides instructions for asset distribution. It is essential—but limited. Wills must pass through probate, which is public, time-consuming, and often expensive.

A living trust allows assets to bypass probate, preserves privacy, and can include specific provisions guiding how wealth is used. Trusts offer flexibility that wills simply cannot match:

- Stage distributions across time rather than transferring assets all at once

- Attach conditions tied to education, responsible spending, or charitable giving

- Appoint a trustee to manage assets for beneficiaries who are not yet ready

Many families benefit from having both documents in place. A will serves as a catch-all for assets not held in the trust, while the trust handles the bulk of the estate efficiently and privately.

Beneficiary Designations and Powers of Attorney

Certain assets transfer outside of the will entirely. Retirement accounts, life insurance policies, and joint-tenancy property pass directly to named beneficiaries — which makes it critical to keep those designations current and aligned with your broader estate plan. Outdated beneficiary designations are one of the most common and costly estate planning mistakes families make.

Two additional documents round out your incapacity planning:

- Financial power of attorney: authorizes a trusted person to manage financial decisions if you cannot

- Healthcare power of attorney: designates someone to make medical decisions on your behalf

Without these in place, family members may need to petition a court for guardianship — a public, expensive, and emotionally draining process that the right documents make entirely avoidable.

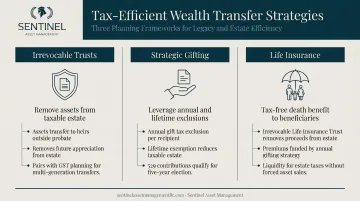

Tax-Efficient Wealth Transfer Strategies

Strategic planning can significantly reduce the estate tax burden on heirs. Key strategies include:

- Irrevocable trusts (such as ILITs and SLATs) remove assets from your taxable estate while preserving certain benefits or access

- Annual gifting: the 2025 exclusion is $19,000 per recipient, allowing lifetime wealth transfers without drawing on your lifetime exemption

- Life insurance structures that provide liquidity to cover estate taxes without forcing the sale of assets

Per IRS guidance, the federal estate tax exemption for 2025 is $13,990,000 per individual. Proposed legislation (the One Big Beautiful Bill Act) would raise that to $15 million per individual ($30 million for married couples) starting in 2026, indexed for inflation — though this has not yet been enacted into law. Families with estates approaching or exceeding these thresholds benefit substantially from proactive planning now, regardless of how the legislation resolves.

Special Needs Planning

Families with a loved one who has a disability face additional complexity. An inheritance received directly can disqualify that person from government benefits like Supplemental Security Income (SSI) and Medicaid.

A special needs trust (also called a supplemental needs trust) preserves eligibility while still providing meaningful financial support. Federal law (42 U.S.C. § 1396p) governs these trusts, permitting them to pay for supplemental expenses — education, recreation, therapy, quality-of-life improvements — without affecting benefit eligibility.

Sentinel Asset Management brings **25 years of experience supporting families with special needs**, having worked long-term with 20+ families requiring lifelong support. The firm coordinates with attorneys and care planners to ensure financial planning integrates seamlessly with legal structures and day-to-day care management.

Passing Down Values, Not Just Wealth

Most parents intend to pass down values but never create a formal mechanism for doing so. The values exist in the mind of the wealth-builder but never get encoded into documents, conversations, or structures that outlive them. This section covers practical tools that bridge the gap.

The Ethical Will

An ethical will (or "letter of intent") is a non-legal personal document in which you articulate your life philosophy, core beliefs, family traditions, and the hopes you have for future generations. It is distinct from a legal will, which governs property.

The practice has ancient roots, originating in Jewish tradition with the biblical example of Jacob blessing his sons in Genesis 49, but today it is used across secular and religious demographics. Ethical wills capture the "why" behind your decisions and provide context that legal documents cannot.

Example elements of an ethical will:

- Key life lessons learned through experience

- Values you hope your children and grandchildren will carry forward

- Stories that illustrate those values in action

- Blessings, hopes, and encouragement for future generations

- Reflections on what gave your life meaning and purpose

Most families who use one say it becomes the document heirs return to most.

The Family Mission Statement

A family mission statement is a written document—ideally developed collaboratively with family members—that gives the family a shared identity and set of principles to orient financial decisions around.

It typically includes:

- Shared values and guiding principles

- Philanthropic priorities and charitable goals

- Expectations around stewardship and responsible wealth management

- Guidelines for family governance and decision-making

The mission statement can be referenced in trust documents or family governance policies, providing trustees and heirs with a clear framework for discretionary decisions. It creates alignment across generations and reduces the ambiguity that can otherwise invite disputes.

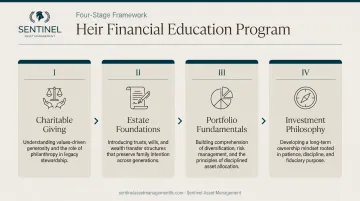

Financial Education for Heirs

A governance structure means little if heirs lack the knowledge to work within it. That gap is where wealth transfer most often breaks down.

The industry frequently cites that "70% of wealth is lost by the second generation," but that statistic has been debunked as stemming from a narrow 1987 study of 200 Illinois manufacturing businesses. The real problem is not inevitable dissipation. Peer-reviewed research links financial literacy directly to better household wealth accumulation and intergenerational transfer outcomes. The problem is lack of preparation.

Educating heirs on investing, budgeting, charitable giving, and the family's financial philosophy pays dividends for generations.

This can include:

- Involving heirs in charitable decisions

- Providing supervised practice managing a small inheritance ("pilot program")

- Sharing the family's investment philosophy and risk management approach

- Teaching the difference between assets that appreciate and liabilities that depreciate

Involving Your Family in the Legacy Conversation

Family communication is a non-negotiable component of effective legacy planning. When heirs are surprised by decisions, they are more likely to dispute them. Research on 2,500 families found that 60% of post-estate transition failures are caused by a breakdown of communication and trust within the family, while 25% are due to unprepared heirs.

Starting these conversations early is one of the most protective steps a family can take.

Practical approaches for starting the conversation:

- Hold a family meeting to share your values and intentions

- Explain the reasoning behind key decisions—why certain assets go to certain people, why a trust includes specific conditions

- Give heirs a preview of the plan rather than a surprise after the fact

- Discuss your expectations around stewardship, education, and responsible wealth management

These conversations do not need to happen all at once. An experienced financial advisor can serve as a neutral facilitator, helping families work through sensitive topics such as unequal distributions, family business succession, or planning for dependents with special needs. That kind of structured guidance keeps the focus on shared intentions rather than individual grievances.

Common Mistakes That Derail a Legacy

No Plan — or an Outdated One

The most common and costly mistake is having no plan at all—or having a plan drafted decades ago that was never updated. Only 24% of American adults currently have a will—a steady decline from 33% in 2022. Among those without a will, 40% falsely believe they "don't have enough assets" to justify one.

An outdated estate plan can be as damaging as no plan because it may contradict your actual wishes. Marriages, divorces, births, deaths, and tax law changes all necessitate plan updates.

Treating Estate Planning as a One-Time Event

Circumstances change, and a legacy plan needs to keep pace. Common triggers that call for a review include:

- Major positive financial changes (inheritance, business sale, significant asset growth)

- Family expansion or contraction (marriage, divorce, births, deaths)

- Medical diagnoses that affect long-term care planning

- Shifts in federal or state tax law

Failing to Prepare Heirs

Leaving significant wealth to unprepared beneficiaries is a primary reason inherited wealth disappears within one or two generations. Without financial education, governance structures, or clear guidance on family values, even well-constructed estates can unravel. The plan itself is only half the work — the people receiving it matter just as much.

Frequently Asked Questions

Frequently Asked Questions

What is the most common inheritance mistake?

The most common mistake is failing to have—or regularly update—a formal plan, which leads to assets passing through probate, unintended tax burdens, and family disputes. A close second is leaving wealth to heirs who have not been prepared financially or emotionally to manage it.

What is the difference between legacy planning and estate planning?

Estate planning focuses on the legal and financial mechanics of transferring assets—wills, trusts, beneficiary designations. Legacy planning goes beyond that foundation to include the intentional transfer of values, life lessons, charitable goals, and family principles.

When should I start legacy planning?

The best time to start is well before it feels urgent—ideally in your 40s or 50s. Family conversations, ethical wills, and heir education take years to develop meaningfully—waiting until health declines limits your options.

What is an ethical will and do I need one?

An ethical will is a personal (non-legal) document in which you capture your values, life lessons, and hopes for future generations. While it is not legally required, it is one of the most impactful tools for ensuring your values—not just your assets—reach the people who follow you.

How can I include charitable giving in my legacy plan?

Options include donor-advised funds (DAFs), charitable remainder trusts (CRTs), and direct bequests in a will or trust. Each option lets you support causes that matter to your family while also reducing estate tax liability.

How do I make sure my heirs are prepared to receive wealth responsibly?

Start with financial education and open family conversations about your estate plan, then reinforce those with trust structures that encourage responsible behaviors. An advisor experienced in wealth transfer can design provisions that motivate heirs rather than restrict them.

Take the next step in your financial journey by exploring our courses page for upcoming live seminars.