General information, not personalised tax, legal or investment advice.

Introduction

Estate planning feels overwhelming because most people don't know where legal help ends and financial planning begins. An estate planning and trust services attorney is a licensed legal professional who drafts, reviews, and executes legally binding documents governing your assets and healthcare decisions after death or incapacity. Their role matters because without proper legal instruments—wills, trusts, powers of attorney—state law decides who gets your assets, rarely as you'd choose.

This article covers what estate planning attorneys do, the documents they draft, and how financial advisors handle the coordination work that sits outside legal counsel's scope.

Key takeaways

- Estate planning attorneys draft legally binding documents: wills, trusts, powers of attorney, and healthcare directives

- 56% of Americans lack any estate planning documents, primarily due to procrastination and perceived lack of assets

- Financial advisors handle beneficiary designations, asset titling, and tax coordination — work that falls outside legal document drafting

- Misaligned beneficiary designations can override your will entirely, as confirmed in the Supreme Court case Hillman v. Maretta

- Special needs trusts need both legal precision and financial oversight to protect government benefit eligibility

What Does an Estate Planning & Trust Services Attorney Do?

An estate planning attorney is the only professional authorized to draft, review, and execute the legally binding documents that dictate what happens to your wealth and who makes decisions if you're incapacitated. These documents aren't suggestions—they're enforceable legal instruments that direct executors, trustees, courts, and family members.

Core Legal Services

Estate planning attorneys provide distinct legal services that no financial advisor can replicate:

- Wills — Naming beneficiaries, designating an executor, appointing guardians for minor children

- Trusts — Establishing revocable and irrevocable structures that hold and distribute assets according to your terms

- Powers of Attorney — Granting agents authority to manage financial and legal affairs during incapacity

- Healthcare Proxies — Appointing someone to make medical decisions when you cannot

- Living Wills — Documenting your preferences for life-sustaining treatment

Each document serves a specific function. A will directs probate assets and names guardians, while a durable power of attorney keeps your finances running during incapacity. Your healthcare proxy and living will handle what a financial plan cannot: ensuring your medical decisions reflect your values when you can't speak for yourself.

Probate and Estate Administration

When someone dies, their will must be validated through probate—a court-supervised process that involves gathering assets, paying debts, filing tax returns, and distributing what remains. The average estate completes probate in 6 to 9 months, consuming 3% to 8% of the estate's gross value in fees and costs.

Attorneys guide executors and trustees through this multi-step administration process. Proper planning—particularly through trusts—can reduce or avoid probate altogether, preserving both time and money. A financial advisor coordinates this process alongside legal counsel, ensuring the financial components align with the legal structure your attorney puts in place.

Estate Litigation

When bad actors interfere with an estate through fraud, undue influence, or mismanagement, attorneys step in to protect beneficiaries. A San Francisco study found 11.5% of estates were tainted by litigation, with average attorneys' fees jumping from $505 in uncontested estates to $14,112 in contested matters. Time in probate extended from 511 days to 769 days.

Estate attorneys assert rights, challenge invalid documents, and help recover assets when legal disputes arise. Most of these disputes trace back to absent or ambiguous planning documents—which is exactly what the intestacy rules were never designed to fix.

Dying Without a Will (Intestacy)

If you die without a will, state intestacy laws determine who inherits your assets—and these rules rarely align with your actual wishes. Typically, your estate passes to your spouse and children in statutory proportions. If you have no spouse or children, it goes to parents, then siblings, then more distant relatives.

This means:

- Your unmarried partner receives nothing

- Stepchildren you raised receive nothing

- Charities you supported receive nothing

- Your estranged sibling gets the same share as your devoted friend

Legal documents ensure your intentions govern, not a one-size-fits-all state statute.

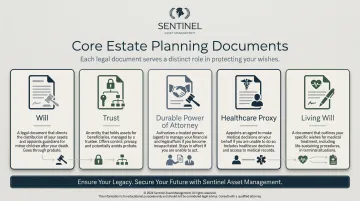

Core Estate Planning Documents Explained

Last Will and Testament

A will is a legal document that describes how property and assets should be distributed after death. It allows you to:

- Name specific beneficiaries for specific assets

- Designate an executor to manage the estate

- Appoint guardians for minor children

One important boundary: a will has no authority over assets held in trust or assets with named beneficiaries — such as retirement accounts, life insurance, and payable-on-death accounts. Those pass by contract, regardless of what your will says.

Durable Power of Attorney

A power of attorney grants an agent authority to act on your behalf. Under the Uniform Power of Attorney Act, a POA is "durable" if it remains effective during your incapacity.

A general POA terminates the moment you become incapacitated, which is precisely when you need it most. A durable POA survives incapacity, allowing your agent to pay bills, manage investments, and handle legal affairs when you cannot.

Healthcare Proxy and Living Will

A healthcare proxy (or durable medical power of attorney) appoints an agent to make medical decisions if you lose capacity. A living will expresses your written preferences for life-sustaining treatment in terminal scenarios.

Why you need both: The healthcare proxy names who decides. The living will documents what you want. Together, they ensure your medical care reflects your values when you can't communicate them.

Only 36.7% of U.S. adults have completed an advance directive, leaving the majority vulnerable to family conflict and unwanted medical interventions.

Trust Documents

A trust document establishes:

- Grantor: the person who creates and funds the trust

- Trustee: manages trust assets and carries out its instructions

- Beneficiaries: the individuals who receive trust benefits

- Terms: the rules dictating how and when assets are managed and distributed

Trusts bypass probate because assets are owned by the trust, not by you individually. Upon your death, the trustee distributes assets according to the trust terms — no court involvement required.

Non-Legal Instruments (Coordinated by Financial Advisors)

Not every estate planning tool requires a lawyer. Several contract-based designations transfer assets directly to named recipients, independent of your will:

- Beneficiary designations on retirement accounts (IRAs, 401(k)s)

- Life insurance beneficiary forms

- Transfer-on-death (TOD) registrations for brokerage accounts

- Payable-on-death (POD) designations for bank accounts

Because these designations override your will entirely, keeping them aligned with your broader estate plan matters. A financial advisor can map your beneficiary designations against your overall plan to catch conflicts before they become costly surprises.

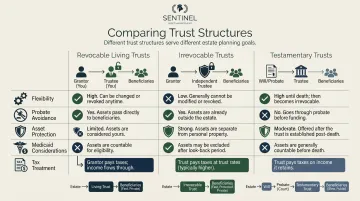

Types of Trusts and How They Protect Your Wealth

Revocable Living Trust

A revocable living trust is created during your lifetime and can be amended or revoked at any time. You maintain complete control as both grantor and trustee.

Primary uses:

- Avoiding probate (assets pass directly to beneficiaries)

- Managing assets during incapacity (successor trustee takes over without court intervention)

- Maintaining privacy (trust distributions aren't public record)

Trade-off: Because you retain control, the IRS treats the trust as a "grantor trust," reporting all income on your individual tax return. The trust offers no asset protection from creditors and doesn't reduce estate taxes.

Irrevocable Trust

Where a revocable trust prioritizes flexibility, an irrevocable trust trades control for protection. Once established, it generally cannot be changed or revoked — the grantor gives up ownership permanently.

Why surrender control?

- Assets are no longer yours, shielding them from creditors and lawsuits

- Properly structured irrevocable trusts remove assets from your taxable estate

- Assets transferred to an irrevocable trust may not count toward Medicaid eligibility limits (subject to the 60-month look-back period)

The Medicaid catch: The Deficit Reduction Act of 2005 enforces a strict 60-month look-back period. If you transfer assets to an irrevocable trust within 60 months of applying for Medicaid, you face a penalty period of ineligibility.

| Trust Type | Can You Change It? | Primary Benefit | Tax Treatment | Medicaid Impact |

|---|---|---|---|---|

| Revocable Living Trust | Yes | Probate avoidance | Taxed to individual | Countable resource |

| Irrevocable Trust | No | Asset protection | May be separate entity | 60-month look-back applies |

| Testamentary Trust | No (created at death) | Post-death control | Separate taxable entity | Funded post-death via probate |

Special Needs (Supplemental Needs) Trusts

Over 70 million U.S. adults live with a disability, many relying on means-tested benefits like Supplemental Security Income (SSI) and Medicaid. A direct inheritance can push a beneficiary over the strict $2,000 asset limit, instantly disqualifying them from vital programs.

A special needs trust (SNT) holds assets for a beneficiary without disqualifying them from government benefits. Poor drafting can trigger immediate benefit loss or mandatory Medicaid payback — so the structure of the trust matters as much as the decision to create one.

First-Party vs. Third-Party SNTs:

| Feature | First-Party SNT | Third-Party SNT |

|---|---|---|

| Funding Source | Beneficiary's own assets (settlement, inheritance) | Family member's assets |

| Age Limit | Beneficiary must be under 65 | No age limit |

| Medicaid Payback | Required upon beneficiary's death | Not required |

| Creator | Beneficiary, parent, guardian, or court | Anyone except the beneficiary |

When funding comes from a parent, grandparent, or other family member, a third-party SNT preserves the full inheritance — nothing is clawed back by Medicaid after the beneficiary's death. The earlier this structure is established, the more options the family retains.

Testamentary Trusts

Unlike the trust types above — all created and funded during your lifetime — testamentary trusts exist only within a will and take effect at death. They work well when you need to:

- Controlling distributions to minor children (releasing assets at specific ages)

- Providing structured oversight for heirs who struggle with money management

- Protecting inheritances from beneficiaries' creditors or divorcing spouses

Unlike living trusts, testamentary trusts are funded through probate, meaning they don't avoid court involvement or public disclosure.

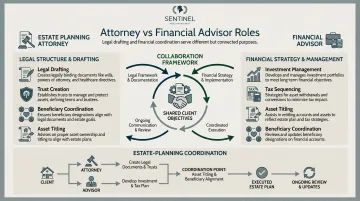

When Do You Need an Estate Planning Attorney vs. a Financial Advisor?

When Do You Need an Estate Planning Attorney vs. a Financial Advisor?

You Must Use an Attorney For:

- Drafting a will or trust document

- Creating powers of attorney

- Establishing healthcare proxies or living wills

- Any document requiring notarization or court interaction

- Complex estate planning instruments (irrevocable trusts, special needs trusts, charitable trusts)

These documents carry real legal consequences. Improperly drafted wills can be contested in probate court, and poorly structured trusts can fail to protect the assets they were meant to hold.

A Financial Advisor Handles:

- Investment management within a trust

- Beneficiary designation alignment across retirement accounts and life insurance

- Tax-efficient asset titling (how accounts are owned)

- Retirement account coordination (Roth conversions, withdrawal sequencing)

- Distribution strategy that minimizes lifetime tax liability

These are financial decisions, not legal ones. An attorney can't optimize your asset location across taxable, tax-deferred, and tax-free accounts. A financial advisor can't draft a power of attorney.

Cost and Efficiency

Understanding what each professional costs helps you budget for both. A 2026 study of 909 law firms found 94% use flat-fee pricing rather than hourly billing:

| Document/Package | National Median | Middle 50% Range |

|---|---|---|

| Power of Attorney (Single) | $300 | $250 – $400 |

| Last Will and Testament (Single) | $625 | $450 – $1,000 |

| Revocable Living Trust (Package) | $2,700 | $2,500 – $3,500 |

Legal document drafting is typically a one-time or periodic expense. Financial advisory relationships are ongoing, involving continuous portfolio management, beneficiary review, and tax coordination.

In practice, most families spend far more time with their financial advisor than their estate attorney — because keeping your plan current, tax-efficient, and aligned with your goals is an ongoing process, not a one-time drafting exercise.

How Financial Planning and Estate Planning Work Together

A legally drafted estate plan is only as strong as the financial structure supporting it. Misaligned beneficiary designations, improperly titled assets, or uncoordinated retirement accounts can override even a perfectly drafted will or trust.

The Beneficiary Designation Problem

In the 2013 Supreme Court case Hillman v. Maretta, the Court ruled that federal law governing a life insurance program preempted a state law automatically revoking beneficiary designations to former spouses upon divorce. Because the deceased hadn't updated his beneficiary form, his ex-spouse legally received the death benefit—overriding state statute and his likely intent.

Contract-based designations (IRAs, 401(k)s, life insurance) trump your will. If your will leaves everything to your children but your IRA still names your ex-spouse, your ex-spouse gets the IRA.

The Coordinated Financial Ecosystem

That's the gap a coordinated financial ecosystem is designed to close. When investment allocation, tax efficiency, and legacy goals are aligned, wealth reaches beneficiaries as intended—without detours created by outdated forms or mismatched account titles.

This coordination integrates:

- Asset organization across taxable, tax-deferred, and tax-free accounts

- Beneficiary designation alignment across all financial accounts

- Asset titling that reflects your estate plan (individual, joint, trust ownership)

- Withdrawal sequencing that minimizes lifetime taxes

- Investment strategy designed to support income needs and legacy goals

Sentinel Asset Management focuses on the financial coordination work that sits outside a lawyer's scope—updating accounts, aligning insurance policies, and structuring ownership correctly. When formal legal documents are needed, their advisors work directly with estate attorneys so the financial and legal pieces reinforce each other.

Estate Planning for Families with Special Needs

Families with a special needs member face unique financial planning challenges:

- Long-term care costs that can exceed $100,000 annually

- Government benefit preservation (SSI, Medicaid) with strict asset and income limits

- Inheritance risks where a direct bequest disqualifies the beneficiary from critical benefits

Without proper trust structuring, an inheritance intended to help can instead harm by triggering benefit loss.

What Special Needs Trust Management Actually Requires

Special needs trusts require both legal precision (proper drafting to satisfy SSA rules) and ongoing financial oversight (investment management, distribution coordination, tax planning). A trust document alone isn't enough. Someone must manage the assets, coordinate distributions that supplement rather than replace benefits, and navigate the overlap between trust income and government program rules.

Sentinel Asset Management has spent 25 years supporting families with special needs members — currently working with more than 20 such families on an ongoing basis. The firm coordinates directly with attorneys and care planners so that trust distributions stay benefit-compliant, investment decisions account for long-term care timelines, and nothing falls through the cracks between legal and financial planning.

Frequently Asked Questions

Who is the best person to manage a trust?

Family members often serve as trustees, but corporate trustees — banks or trust companies — are better suited for complex or multi-generational trusts. They provide professional oversight, eliminate conflicts of interest, and ensure continuity over time.

What is the 5% rule for trusts?

Under Internal Revenue Code §664, charitable remainder trusts must pay "not less than 5 percent nor more than 50 percent" of trust assets annually to beneficiaries. The 5% minimum ensures a meaningful income stream while preserving the charitable remainder for the designated nonprofit.

Do I need an estate planning attorney if I already have a financial advisor?

Yes — the roles are complementary, not interchangeable. Attorneys draft and execute legal documents; financial advisors handle beneficiary coordination, asset titling, and tax strategy. A complete plan requires both.

What is the difference between a revocable and irrevocable trust?

A revocable trust can be changed or cancelled during your lifetime, preserving flexibility. An irrevocable trust cannot be altered, but that permanence enables asset protection, estate tax reduction, and Medicaid planning benefits.

What documents does a basic estate plan include?

At minimum: a will, durable power of attorney, and healthcare proxy or living will. Many plans also include a revocable living trust for probate avoidance. The right combination depends on your family situation, asset complexity, and state laws.

When should I review or update my estate plan?

The National Institute on Aging recommends reviewing your plan at least annually and after major life events — marriage, divorce, birth of a child, death of a beneficiary, or significant asset changes. Nearly one in four Americans haven't updated their wills since origination, leaving outdated provisions in place.

Attorneys and financial advisors serve distinct but connected roles in estate planning. When both are engaged, your legal documents and financial strategy align — so your wealth reaches the people and causes you care about, on your terms.

Take the next step in your financial journey by exploring our courses page for upcoming live seminars.