General information, not personalised tax, legal or investment advice.

Introduction: The Retirement Income Challenge Most People Don't See Coming

You spent decades saving for retirement, watching your 401(k) grow and your IRA balance climb. Converting those savings into reliable, lasting income, however, requires a completely different skill set than the one that built your nest egg.

Research from the Employee Benefit Research Institute reveals that most retirees have no withdrawal strategy at all—they simply wait until the IRS forces distributions at age 73. This behavioral inertia leaves hundreds of thousands of dollars on the table in unnecessary taxes and exposes portfolios to preventable risks.

The fears driving the need for a plan are consistent across nearly every retiree:

- Outliving your savings before the end of retirement

- Suffering market downturns during the critical early years

- Managing rising healthcare costs on a fixed income

- Navigating unpredictable tax consequences from required distributions

This guide walks through the key decisions you can actually control — from identifying income sources and sequencing withdrawals to timing Social Security and protecting against inflation — treating each as a learnable, actionable step.

Key takeaways

- Retirement income planning follows a different set of rules than saving—strategically spending down assets requires a new framework

- Catalog all income sources before building your withdrawal plan to understand your guaranteed income floor

- Bucket strategies protect near-term spending needs from market volatility while maintaining long-term growth

- Withdrawal sequencing across taxable, tax-deferred, and tax-free accounts can reduce your lifetime tax bill by $100,000 or more

- Delaying Social Security even a few years substantially increases guaranteed lifetime income

Why Retirement Income Planning Is Different from Saving

The Fundamental Shift

During your working years, your portfolio's job was simple: grow. Market downturns were buying opportunities. You had time to recover. The longer the horizon, the more risk you could accept.

Retirement changes that entirely. Now your portfolio must sustain income for 20–30+ years while managing three forces that didn't matter much before: sequence-of-returns risk, withdrawal rates, and inflation erosion. Success depends less on how much you saved and more on how strategically you spend it down.

Why Early Market Downturns Hurt More

Sequence-of-returns risk means the order in which you experience market returns matters enormously when you're withdrawing funds. A market downturn in your first few retirement years is far more damaging than one mid-career because you're selling assets at depressed prices to fund living expenses. Those shares, once sold, can never recover—even when the market does.

Consider two retirees with identical $1 million portfolios, both withdrawing $40,000 annually. Retiree A experiences strong returns early and poor returns later. Retiree B suffers poor returns early but strong returns later. Despite identical average returns over 20 years, Retiree B's portfolio may be exhausted while Retiree A's continues growing. When you're in distribution mode, the sequence of returns matters as much as the returns themselves.

The 4% Rule Is a Starting Point, Not Gospel

The traditional 4% withdrawal rule—withdraw 4% of your portfolio in year one and adjust for inflation annually—emerged from historical analysis of portfolio survival rates. It's a useful benchmark, but your personal withdrawal rate might be higher or lower depending on:

- Longevity outlook — family history of living into the late 90s demands a more conservative rate than a shorter horizon

- Supplemental income — pensions, rental income, or part-time work reduce how much your portfolio needs to cover

- Spending flexibility — discretionary expenses that can contract during downturns give you more room than fixed obligations

- Portfolio cushion — a $2 million portfolio funding $60,000 annually has far more margin than one funding $80,000

The math only tells part of the story. How you behave when markets drop is just as important as the withdrawal rate you choose.

The Psychological Challenge: From Saver to Spender

After decades of discipline—maxing contributions, avoiding early withdrawals, watching balances grow—many retirees struggle to shift into spending mode. Some under-spend, depriving themselves of experiences their savings were meant to fund. Others overspend early, depleting assets before recognizing the danger.

Both patterns carry real costs.

This mental transition requires acknowledging that your portfolio's purpose has changed. The goal is no longer accumulation—it's strategic distribution that funds your lifestyle while preserving purchasing power across an uncertain timeline.

Know Your Retirement Income Sources

Before building any withdrawal strategy, you need a complete inventory of where income will come from and how reliable each source is.

Main Categories of Retirement Income

Guaranteed/Predictable Sources:

- Social Security retirement benefits

- Employer pensions (defined benefit plans)

- Annuity contracts with guaranteed income riders

Variable/Market-Dependent Sources:

- 401(k), 403(b), and traditional IRA withdrawals

- Roth IRA distributions

- Taxable brokerage account withdrawals

- Rental property income

- Part-time work or consulting income

Why Your Guaranteed Income Floor Matters

The stronger your guaranteed income base, the more risk you can prudently accept with remaining assets. A retiree with Social Security and a pension covering 80% of fixed expenses can invest the remaining portfolio more aggressively than someone entirely dependent on portfolio withdrawals.

Calculate your guaranteed monthly income floor, then compare it to your baseline living expenses—mortgage/rent, utilities, food, insurance, healthcare premiums, and property taxes. The gap between guaranteed income and baseline expenses is what your portfolio must reliably generate.

Take Stock Exercise:

- List all income sources with estimated monthly amounts

- Separate guaranteed from variable sources

- Calculate total monthly baseline expenses

- Identify the "gap" your portfolio must fill

- Determine how much discretionary spending you can layer on top

The Role of Annuities in a Retirement Income Plan

For retirees without pensions, annuities can help close that income gap. You transfer a lump sum to an insurance company in exchange for guaranteed monthly payments — either for life or a specified period.

Key trade-offs include:

- Once annuitized, those funds generally can't be accessed as a lump sum

- Fees and surrender charges can be substantial — read the fine print

- Product features vary widely; compare options carefully before signing

- Fixed payments lose purchasing power over time unless you pay for an inflation rider

Annuities aren't right for everyone. They work best when you need guaranteed income, have longevity concerns, and can afford to lock up a portion of your portfolio. Evaluate any annuity within the context of your complete income plan — never as a standalone purchase.

Building a Withdrawal Strategy That Works

Not All Retirement Accounts Are Created Equal

Where you hold money—taxable brokerage accounts, tax-deferred IRAs and 401(k)s, or tax-free Roth accounts—determines how much of it you actually keep. The order in which you withdraw from these accounts has major consequences for portfolio longevity and lifetime tax burden.

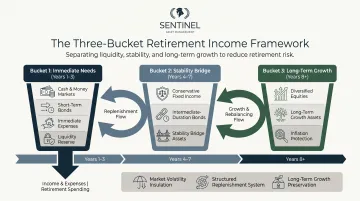

The Bucket Strategy: Structure for Stability

The bucket approach divides assets into three time-horizon-based pools:

Bucket 1 (Years 1-3): Cash, money markets, short-term bonds, and other stable assets covering 1-3 years of expenses. Having liquid reserves here means you never sell growth assets at a loss to meet near-term needs.

Bucket 2 (Years 4-7): Conservative bonds, intermediate-duration fixed income, and stable value funds. This middle tier bridges immediate spending needs and long-term growth while providing a buffer if Bucket 1 runs thin.

Bucket 3 (Year 8+): Diversified equities and growth assets designed to outpace inflation over decades. Because you won't touch these funds for years, they have time to recover from market downturns without forcing a sale at depressed prices.

This structure allows your growth bucket to recover from downturns without forcing you to sell at depressed prices. When markets fall, you draw from Buckets 1 and 2. When markets rise, you replenish Bucket 1 from Bucket 3's gains. Sentinel Asset Management uses a structured bucket approach as part of personalized portfolio design, specifically to protect near-term cash flow from market volatility while maintaining long-term purchasing power.

Determining How Much to Withdraw Each Year

Key factors include:

- Required Minimum Distributions (RMDs) starting at age 73

- Planned baseline expenses (housing, healthcare, insurance, taxes)

- Discretionary spending (travel, gifts, hobbies)

- Healthcare costs and long-term care planning

- Legacy goals and charitable giving intentions

The Investment Policy Statement: Your Written Plan

An Investment Policy Statement (IPS) is a documented framework that defines your income targets, risk tolerance, asset allocation, and withdrawal rules. It serves as your decision-making anchor during volatile markets, ensuring you act according to plan rather than emotion.

A strong IPS includes:

- Target annual withdrawal amount and inflation adjustment methodology

- Asset allocation ranges for each bucket

- Rebalancing triggers and rules

- Tax management guidelines

- Conditions under which the plan should be reviewed and adjusted

Among the 2,000+ clients Sentinel Asset Management has guided through retirement, those with a written IPS in place are better positioned to stay the course when markets move against them — because the decision was already made before the volatility arrived.

Managing Taxes on Your Retirement Withdrawals

How Different Accounts Are Taxed

Each account type is taxed differently — and knowing the rules shapes every withdrawal decision you make:

- Traditional 401(k)/IRA: Withdrawals taxed as ordinary income at your current marginal rate

- Roth IRA: Qualified distributions are completely tax-free

- Taxable brokerage: Long-term capital gains taxed at preferential rates (0%, 15%, or 20% depending on income)

IRS Publication 590-B confirms these treatments and provides detailed distribution rules for retirement accounts.

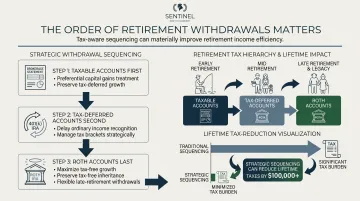

The Standard Withdrawal Sequencing Rule (and When to Break It)

The conventional wisdom suggests this order:

- Taxable accounts first - Capture preferential capital gains rates and preserve tax-deferred growth

- Tax-deferred accounts second - Delay ordinary income tax as long as possible

- Roth accounts last - Maximize tax-free growth and preserve for heirs or large expenses

Exceptions exist: Strategic Roth conversions during low-income years before RMDs begin can cut your future tax burden substantially. If you retire at 62 but delay Social Security until 70, you may have a multi-year window of relatively low income—perfect for converting traditional IRA assets to Roth at favorable rates.

That window closes once RMDs arrive, which is where the sequencing strategy meets its biggest test.

The RMD Tax Trap

Required Minimum Distributions force ordinary income recognition that stacks on top of Social Security and pensions starting at age 73. This forced income can push retirees from the 12% bracket into the 22% or 24% bracket. It can also trigger taxation on up to 85% of Social Security benefits.

RMDs also trigger hidden "ghost taxes":

- Medicare IRMAA surcharges when income exceeds $106,000 (single) or $212,000 (joint)

- Net Investment Income Tax (NIIT) at 3.8% when income exceeds $200,000 (single) or $250,000 (joint)

Planning ahead, before RMDs begin, gives you the best tools to avoid these traps: strategic Roth conversions, qualified charitable distributions, and disciplined income management in the years leading up to age 73.

When and How to Claim Social Security

The Age Decision and Benefit Amounts

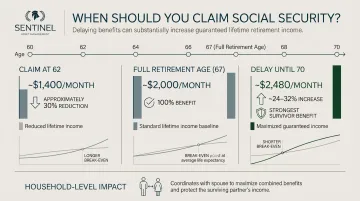

You can claim Social Security as early as 62, at full retirement age (66-67 depending on birth year), or as late as 70. Each month you delay increases your benefit:

- Claiming at 62: Approximately 30% reduction from full retirement age benefit

- Claiming at full retirement age: 100% of calculated benefit

- Delaying to 70: Approximately 24-32% increase above full retirement age benefit

For someone entitled to $2,000/month at full retirement age (67), claiming at 62 yields roughly $1,400/month. Waiting until 70 produces approximately $2,480/month — a 77% difference in monthly income over a lifetime.

Key Factors Influencing Optimal Timing

Several factors shape the right claiming age for your situation:

- Health and life expectancy: A family history of longevity favors delaying; chronic health conditions may support earlier claiming.

- Other income sources: With sufficient portfolio assets or pension income, delaying lets your Social Security benefit grow at a guaranteed 8% annually — a rate few investments can reliably match.

- Marital status: Coordinated claiming strategies for married couples can meaningfully increase household lifetime income. The higher earner delaying to 70 maximizes the survivor benefit for the remaining spouse.

- Continued employment: Claiming before full retirement age while still working triggers a benefit reduction — $1 for every $2 earned above $22,320 in 2024.

The Break-Even Concept

These factors feed directly into a concept worth understanding before you decide: the break-even age. This is the point at which cumulative benefits from delayed claiming surpass what you would have received by claiming early. For someone comparing age 62 versus age 70 claiming, break-even typically occurs in the early-to-mid 80s.

For married couples, the analysis is more nuanced. Even if the primary earner doesn't personally reach break-even, the surviving spouse may receive decades of higher survivor benefits. Delayed claiming can be profitable at the household level even when one spouse passes earlier than expected.

Protecting Your Retirement Income Against Inflation and Longevity Risk

The Longevity Challenge

Longevity risk is the possibility of outliving your money. According to Social Security Administration actuarial data, a 65-year-old couple today has approximately a 50% probability that at least one spouse will live to age 90, and roughly a 25% chance one will reach 95. Planning for a 25-30 year retirement isn't pessimistic—it's realistic.

How Inflation Erodes Purchasing Power

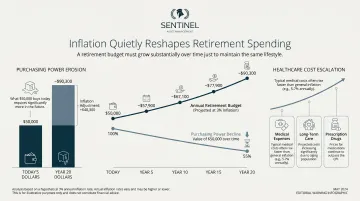

A 3% annual inflation rate cuts purchasing power in half over 24 years. Healthcare inflation typically runs higher than general inflation, meaning medical expenses—often the largest retirement cost—erode budgets faster than other categories.

A $50,000 annual budget today needs to grow to roughly $90,000 in 20 years just to maintain the same standard of living at 3% inflation. Without growth assets in your portfolio, purchasing power shrinks quietly but steadily—year after year.

These risks are real, but they're plannable. Here are the core strategies that address both.

Practical Protection Strategies

Maintain equity exposure throughout retirement: Even conservative retirees should hold 30-40% in diversified equities to generate real returns above inflation. The bucket strategy enables this by keeping near-term needs in stable assets while long-term funds pursue growth.

Use inflation-adjusted income sources:

- Social Security includes annual Cost-of-Living Adjustments (COLA)

- Treasury Inflation-Protected Securities (TIPS) adjust principal for inflation

- Some annuities offer inflation riders (at additional cost)

Build spending flexibility into your plan: Separate fixed baseline expenses from discretionary ones. When markets drop or inflation spikes, trimming travel, entertainment, or gifts preserves your standard of living without touching essential costs.

Plan specifically for healthcare cost escalation: Medicare premiums, Part D prescription coverage, supplemental insurance, and out-of-pocket costs all tend to rise faster than general inflation. Model these separately rather than assuming average inflation rates.

Frequently Asked Questions

How much money do I need to retire comfortably?

There is no universal number—it depends on your expenses, income sources, healthcare needs, and lifestyle. The common benchmark targets replacing 70–100% of pre-retirement income, but your real number comes from the gap between guaranteed income (Social Security, pension) and actual spending. That gap determines your portfolio requirements.

What is the 4% rule in retirement?

The 4% rule—drawn from historical analysis of 30-year retirements—suggests withdrawing 4% of your portfolio in year one, then adjusting that dollar amount for inflation each year. It's a useful starting point, but your sustainable rate also depends on portfolio size, other income sources, and market conditions when you retire.

What is a bucket strategy for retirement income?

The bucket approach divides assets into short-term (1–3 years), medium-term (4–7 years), and long-term (8+ years) pools. Near-term expenses sit in stable assets like cash and bonds, while long-term funds invest for growth—so you're never forced to sell stocks during a downturn to cover living costs.

When should I start taking Social Security benefits?

The decision depends on health, other income, and marital status. Delaying to 70 maximizes monthly benefits (roughly 77% higher than claiming at 62), while claiming at 62 reduces them permanently. For married couples, coordinating claims to maximize survivor benefits is critical. A break-even analysis—typically around age 80—can help clarify which timing works in your favor.

How do taxes affect retirement income withdrawals?

Traditional IRA and 401(k) withdrawals are taxed as ordinary income, Roth withdrawals are tax-free, and taxable brokerage accounts qualify for lower capital gains rates. Strategic withdrawal sequencing—deciding which accounts to draw from and when—can reduce your lifetime tax burden by tens or hundreds of thousands of dollars.

How do I protect my retirement savings from inflation?

Maintain a portion of your portfolio in growth assets (equities) throughout retirement, use inflation-adjusted income sources like Social Security's COLA and TIPS, and plan specifically for rising healthcare costs. Keeping a discretionary spending buffer—travel, dining, entertainment—gives you room to pull back during high-inflation years without cutting essential expenses.

Take the next step in your financial journey by exploring our courses page for upcoming live seminars.