General information, not personalised tax, legal or investment advice.

Introduction

Most donors write a year-end check to their favorite charity and feel good about giving. But they walk away leaving significant tax savings unclaimed because the method of giving, not just the amount, determines the tax outcome. The difference between writing a $10,000 check versus donating $10,000 worth of appreciated stock can mean thousands of dollars in federal taxes saved or forfeited.

The tax landscape has shifted. The near-doubling of the standard deduction has made traditional deduction-based giving harder to access for most taxpayers. In 2026, the standard deduction rises to $32,200 for married couples filing jointly, meaning only 9.5% of taxpayers now itemize deductions.

That narrowing window makes strategy more important, not less. Knowing which tools are available — and when to use them — is what separates a generous donor from a tax-efficient one.

This guide covers who qualifies for charitable deductions, which strategies deliver the most after-tax value, how to match the right approach to your financial profile, and how giving can integrate into a broader estate and retirement plan — not just a year-end impulse.

Key takeaways

- Charitable deductions require itemizing, with caps at 60% of AGI for cash and 30% for appreciated assets

- Donating appreciated securities eliminates capital gains tax while generating a full fair-market-value deduction

- Qualified Charitable Distributions (QCDs) from IRAs offer retirees aged 70½+ a direct, tax-free giving strategy

- Bunching donations into one year—often through a donor-advised fund—can clear the standard deduction threshold

- Charitable giving delivers maximum value when coordinated with investment strategy, income planning, and estate goals

What Makes a Charitable Donation Tax Deductible

Not all gifts are deductible. To claim a charitable deduction, your donation must go to an IRS-qualified 501(c)(3) organization, and you must itemize deductions on Schedule A rather than taking the standard deduction.

2026 Standard Deduction Figures:

- Single filers: $16,100

- Married filing jointly: $32,200

If your total itemized deductions—including state and local taxes, mortgage interest, and charitable contributions—don't exceed these thresholds, you receive no tax benefit from giving.

AGI Percentage Caps

Even when you itemize, deductions are capped by adjusted gross income:

- Cash donations to public charities: Up to 60% of AGI

- Appreciated long-term assets to public charities: Up to 30% of AGI

- Excess contributions: Can be carried forward for up to five tax years

Why Fewer Taxpayers Itemize Today

Approximately 9.5% of taxpayers currently itemize, down from roughly 31% before the Tax Cuts and Jobs Act. This shift has driven demand for strategies that deliver tax benefits without itemizing at all. Qualified Charitable Distributions are one example; bunching is another — a coordination technique that concentrates deductions into strategic years to clear the standard deduction threshold.

5 Tax-Smart Charitable Giving Strategies

Each strategy below targets a different aspect of your tax picture — from capital gains exposure to RMD management to deduction timing. Used together, they can significantly increase the after-tax impact of your giving.

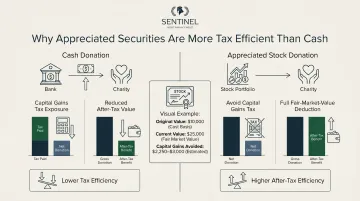

Donating Appreciated Securities Instead of Cash

This strategy delivers a dual tax advantage: you avoid capital gains tax on the embedded appreciation and qualify for an income tax deduction equal to the asset's full fair market value.

How it works:

When you donate long-term appreciated assets—stocks, mutual funds, or ETFs held more than one year—directly to a charity, the charity receives the asset and can sell it tax-free. You receive a deduction for the current market value, not your original cost basis.

Example:

You purchased stock for $10,000 five years ago. It's now worth $25,000.

- If you sell the stock and donate cash: You pay capital gains tax on the $15,000 gain (15-20% federal rate = $2,250-$3,000 tax). You donate the after-tax proceeds and deduct that amount.

- If you donate the stock directly: You avoid the $2,250-$3,000 capital gains tax entirely, and you deduct the full $25,000 fair market value.

Requirements:

- The asset must have been held for more than one year

- The deduction is limited to 30% of AGI for donations to public charities

- Non-publicly traded assets require a qualified appraisal to substantiate fair market value

Donors who already use DAFs have embraced this approach: approximately 63% of contributions to donor-advised funds are non-cash assets, reflecting how effectively the strategy transfers appreciated positions out of taxable portfolios.

Qualified Charitable Distributions (QCDs) from IRAs

A QCD is a direct transfer from a traditional IRA to a qualified charity, available to account holders aged 70½ or older. The distributed amount is excluded from taxable income entirely, unlike a standard IRA withdrawal.

Core tax benefit:

QCDs are valuable even for taxpayers who don't itemize because the distribution doesn't increase your adjusted gross income. This can help you:

- Avoid higher Medicare premiums (IRMAA surcharges)

- Stay below income thresholds for other tax benefits

- Reduce taxable Social Security income

2026 QCD limits:

- Annual limit: $111,000 per individual

- One-time split-interest election (e.g., charitable remainder trust): $55,000

RMD connection:

QCD amounts count toward satisfying required minimum distributions, which begin at age 73 for individuals who reached age 72 after December 31, 2022.

Restrictions:

QCDs cannot be directed to donor-advised funds or private foundations. The distribution must go directly from your IRA custodian to the qualified charity.

Bunching Charitable Contributions

For donors whose annual giving falls short of the standard deduction, bunching offers a straightforward fix. The strategy concentrates two or three years' worth of planned giving into one tax year, pushing itemized deductions above the standard deduction threshold. In off years, you claim the standard deduction instead.

Example:

A married couple has $10,000 in state and local taxes (SALT) and typically donates $15,000 per year.

- Without bunching: $25,000 total itemized deductions annually—below the $32,200 standard deduction. No tax benefit from charitable giving.

- With bunching: They donate $45,000 (three years' worth) in 2026, creating $55,000 in itemized deductions. This exceeds the standard deduction by $22,800, generating significant tax savings. In 2027 and 2028, they take the standard deduction.

Natural pairing with donor-advised funds:

The donor makes a large lump contribution to a DAF in the bunching year, receives the full deduction immediately, and then distributes grants to charities on their preferred timeline over subsequent years.

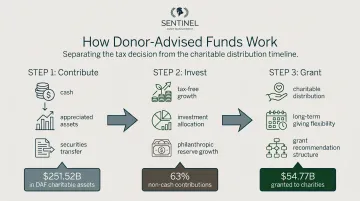

Donor-Advised Funds (DAFs)

A DAF allows you to contribute cash or appreciated assets to the fund, receive an immediate tax deduction in the year of contribution, and then recommend grants to qualified charities over time at your own pace.

How DAFs work:

- Contribute to a DAF sponsoring organization (a 501(c)(3) public charity) and receive an immediate tax deduction

- Assets in the fund are invested and grow tax-free until distributed

- Recommend grants to qualified charities on your own schedule — next month or next decade

Planning flexibility:

DAFs decouple the tax decision from the philanthropic decision. This allows you to act quickly for tax purposes in a high-income year—after a business sale, large bonus, or Roth conversion—without rushing the selection of charities.

Tax treatment:

- Cash contributions: Deductible up to 60% of AGI

- Appreciated assets: Deductible up to 30% of AGI

- Contributed appreciated assets avoid capital gains tax

Growth and usage:

According to the National Philanthropic Trust's 2024 DAF Report, total charitable assets in DAFs reached $251.52 billion in 2023, a 9.9% increase from 2022. DAFs granted an estimated $54.77 billion to qualified charities in 2023, maintaining a payout rate of nearly 24%.

Cash Donations: When Simplicity Still Has a Place

For donors already itemizing well above the standard deduction threshold, or making smaller contributions where administrative overhead isn't justified, cash donations are still fully deductible up to 60% of AGI.

The limitation:

Cash forfeits the opportunity to avoid capital gains embedded in appreciated positions, making it the least tax-efficient method for donors who hold long-term appreciated assets.

How to Choose the Right Strategy for Your Financial Profile

No single charitable giving strategy works for everyone. The right approach depends on where you are financially right now — your age, income sources, and portfolio composition. Here are the key variables to consider before choosing:

- Your age and whether you're taking required minimum distributions

- The composition of your portfolio (appreciated assets vs. cash)

- Whether your itemized deductions currently exceed the standard deduction

- Your marginal income and capital gains tax rates

- Timing of income events (bonuses, business sales, Roth conversions)

Retirees Drawing from IRAs

For retirees aged 73 and older facing mandatory RMDs, Qualified Charitable Distributions (QCDs) are often the most efficient approach because they:

- Reduce taxable income directly

- Lower potential Medicare premium surcharges (IRMAA)

- Require no itemizing

- Satisfy RMD requirements while supporting charitable goals

High-Income Earners in an Elevated Income Year

In years with unusually high income — executive bonuses, business liquidity events, large Roth conversions — bunching contributions into a Donor-Advised Fund (DAF) maximizes the deduction in the year it carries the most value. A DAF allows you to:

- Make a large contribution when your marginal rate is highest

- Distribute grants to charities over multiple years

- Maintain flexibility in your philanthropic timeline

Investors with Concentrated or Highly Appreciated Stock Positions

For investors holding long-term appreciated positions, donating securities directly to charity is often the most tax-efficient move available. This approach:

- Eliminates capital gains exposure on the donated shares

- Generates a full fair-market-value deduction

- Allows you to repurchase the same security at current market price, resetting your cost basis for future tax planning

This approach is particularly valuable when combined with tax-loss harvesting strategies elsewhere in the portfolio. If you're unsure which profile fits your situation, a fiduciary advisor can map the right strategy to your specific income, portfolio, and giving goals.

Charitable Giving as Part of Your Estate and Retirement Plan

Charitable giving is not just a tax-year decision—it's an estate planning tool. Properly structured charitable bequests can reduce the size of a taxable estate, and certain assets may be more tax-efficiently left to charity than to heirs.

Estate Tax Parameters

The federal estate and gift tax basic exclusion amount is $15 million per individual for 2026 under the One Big Beautiful Bill Act, indexed for inflation thereafter. Amounts above this threshold are subject to a 40% federal estate tax.

Asset Beneficiary Coordination

Not all assets are equal from a tax perspective, and the right beneficiary assignment depends on the asset type:

| Asset Type | Best Recipient | Why |

|---|---|---|

| Traditional IRA (pre-tax) | Charity | Charity receives funds tax-free; individual heirs would owe ordinary income tax |

| Appreciated securities | Heirs | Heirs benefit from a step-up in cost basis at death, eliminating capital gains tax |

Advanced Planning Tools: Charitable Trusts

Charitable Remainder Trusts (CRTs):

A CRT pays a specific annuity or unitrust amount to a noncharitable beneficiary (such as the donor) for a term of years or life. At the end of the term, remaining trust assets are distributed to a designated charity.

Charitable Lead Trusts (CLTs):

A CLT reverses the structure. It pays a fixed annuity or unitrust amount to a charitable organization for a specified period. At the end of the term, the remaining corpus passes to noncharitable beneficiaries such as the donor's heirs.

Both instruments require coordination with an estate attorney and financial advisor—and work best when integrated into a broader financial plan from the start, not retrofitted later.

Integrating Giving with Legacy Goals

For families who want their values to outlast their assets, charitable giving belongs in the estate structure alongside investment and retirement planning—not treated as a separate decision made at year-end.

At Sentinel Asset Management, advisors coordinate giving strategies with each client's Investment Policy Statement, tax situation, and legacy goals, ensuring that wealth reaches both causes and heirs efficiently. That coordination extends across taxable, tax-deferred, and tax-free accounts, so philanthropic intentions and multi-generational wealth transfer move forward together.

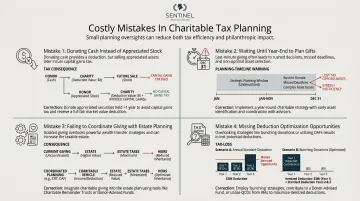

Costly Mistakes to Avoid in Charitable Tax Planning

Donating Cash When Appreciated Assets Are Available

This is the most common and costly oversight. Donors default to writing checks out of habit, forfeiting the opportunity to eliminate capital gains tax while receiving the same deduction amount.

Cost example:

Donating $25,000 in cash versus donating $25,000 worth of stock with a $10,000 cost basis:

- Cash donation: $25,000 deduction, but no additional tax benefit

- Stock donation: $25,000 deduction plus $2,250-$3,000 in avoided capital gains tax (15-20% federal rate on $15,000 gain)

The stock donation delivers the same charitable impact with thousands of dollars in additional tax savings.

Treating Giving as a Year-End Event Rather Than a Year-Round Strategy

Last-minute giving forces reactive decisions that close off better options. When giving is left until December, there's rarely enough time to properly transfer securities or fund a donor-advised fund. Common consequences include:

- Missing securities transfer windows (brokerages need 2-4 weeks minimum)

- Losing the ability to coordinate with major income events earlier in the year

- Defaulting to less tax-efficient cash donations under deadline pressure

- Forfeiting opportunities tied to liquidity events or retirement transitions

Planning gifts earlier in the year keeps every strategy option open — and makes it far easier to connect those gifts to the rest of your financial picture.

Failing to Coordinate Charitable Planning with the Overall Financial Plan

Charitable giving decisions affect:

- Taxable income

- AGI thresholds for Medicare premiums and other phase-outs

- Estate size and tax liability

- Investment portfolio composition

When giving decisions are made in isolation, the tax benefits built into the broader plan go unclaimed — and estate goals can shift in ways no one intended. Treating charitable strategy as part of the full financial plan, not an add-on, is what separates reactive giving from purposeful wealth transfer.

Frequently Asked Questions

What is the maximum tax deduction for charitable gifts?

The deduction limit depends on the type of asset and recipient organization. Cash donations to public charities are generally deductible up to 60% of AGI, while appreciated long-term assets are capped at 30% of AGI. Excess amounts can typically be carried forward for up to five years.

What are the new QCD rules for 2026?

The annual QCD limit for 2026 is $111,000 per individual, indexed for inflation under the SECURE 2.0 Act. The minimum age requirement remains 70½. QCDs count toward satisfying required minimum distributions but cannot be directed to donor-advised funds or private foundations.

What records do you need to substantiate a charitable deduction?

For cash donations under $250, a bank record or written receipt suffices. Gifts of $250 or more require a written acknowledgment from the charity, and non-cash donations over $500 must be reported on IRS Form 8283. Appraisals are required for non-cash contributions exceeding $5,000.

What is the meaning of gift planning?

Gift planning (also called charitable gift planning) is the strategic structuring of charitable contributions to maximize tax benefits and philanthropic impact — covering decisions about what to give, when to give, and which vehicle to use within your overall financial plan.

How do you create a wealth plan that includes charitable giving?

Start by working with a financial advisor to set an annual giving budget, identify the right vehicles (such as DAFs, QCDs, or charitable trusts), and align your philanthropic goals with your broader tax, income, and estate planning strategy.

Take the next step in your financial journey by exploring our courses page for upcoming live seminars.