General information, not personalised tax, legal or investment advice.

Family financial planning isn't about budgeting harder or saving more. It's a coordinated, living strategy that aligns every financial decision—from how you invest today to how you protect your family tomorrow—with where you're actually headed. This article walks through the foundational pillars of a family financial plan, the unique challenges families face, how to build a legacy that lasts, and what to look for when choosing an advisor to guide you.

Key takeaways:

- Family financial planning balances cash flow, investments, taxes, retirement, insurance, and estate needs across the entire household

- Families face unique pressures: raising children costs an average of $233,610, caring for aging parents averages $7,242 annually, and special needs dependents require specialized planning structures

- Only 32% of Americans have a will; dying without one can cost your estate 3-7% in probate fees

- Look for a fiduciary advisor with comprehensive services, relevant family experience, and transparent fee structures

What Is Family Financial Planning?

Family financial planning is a comprehensive, ongoing process of organizing income, assets, protection, and goals across the entire household. Unlike individual planning, it accounts for multiple people, life stages, dependents, and priorities that sometimes conflict.

Families must balance immediate cash flow with decades-long retirement timelines. They protect against risks that affect everyone—disability, premature death, divorce, a child with special needs. The CFP Board defines financial planning as "a collaborative process that helps maximize a Client's potential for meeting life goals through Financial Advice that integrates relevant elements of the Client's personal and financial circumstances."

Despite these benefits, only 36% of Americans have a written financial plan. Among those who do, 96% feel confident they will reach their financial goals. A written plan gives families a concrete framework for decisions that would otherwise be made reactively.

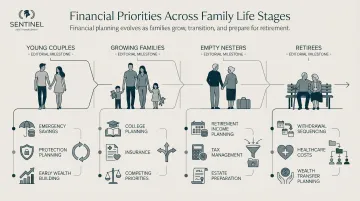

That framework matters at every stage of family life, because the priorities shift dramatically over time:

- Young couples focus on protection, emergency reserves, and cash flow management

- Growing families navigate education costs, life insurance gaps, and competing savings goals

- Empty nesters shift toward retirement income projections and legacy planning

- Retirees manage tax-efficient withdrawals, healthcare costs, and estate transfers

A structured plan doesn't just capture where you are today — it evolves as your family does.

The Core Pillars of a Family Financial Plan

Every family's plan looks different, but six foundational components must work together. Neglecting even one creates vulnerabilities the others can't cover. These pillars form the backbone of any comprehensive strategy—and each one affects how the others perform.

Cash Flow and Budgeting

Healthy cash flow funds every other financial goal: savings, debt payoff, investment contributions. Without it, nothing else in the plan gets traction.

Key components:

- Separate fixed from discretionary spending so you know exactly where flexibility exists

- Automate savings contributions before discretionary expenses hit your account

- Build an emergency fund covering 3-6 months of expenses to absorb unexpected costs without going into debt

Only 55% of adults have three months of emergency savings. Without this buffer, a single car repair or medical bill can force you into debt.

The 50/30/20 rule offers a starting framework: 50% of after-tax income toward needs, 30% toward wants, 20% toward savings and debt. But families with special circumstances—dependents, high debt, approaching retirement—may need a more tailored approach.

Investment and Asset Management

Investments drive long-term growth for retirement, college, and legacy. A family's investment mix must reflect its goals, timeline, and risk tolerance—and this changes over time.

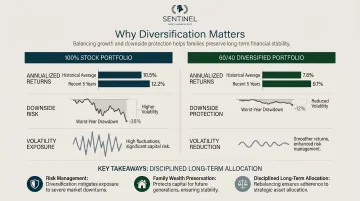

Modern Portfolio Theory, introduced by Harry Markowitz in 1952 (and awarded the Nobel Prize in 1990), is the mathematical framework for assembling portfolios that maximize expected return for a given level of risk. Asset allocation explains approximately 90% of return variability over time.

Diversification reduces volatility and maximum drawdowns. For example, from 1972-2021:

- 100% stocks: 10.75% annual return, -37.45% worst year

- 60/40 stocks/bonds: 9.61% annual return, -16.88% worst year

Disciplined portfolio management addresses five systematic risks—Purchasing Power (inflation), Reinvestment (rate changes), Interest Rate (bond values), Market (overall declines), and Exchange (currency fluctuations)—through diversified, deliberately structured positions.

Sentinel Asset Management builds portfolios on these same principles, using Investment Policy Statements tailored to each family's goals, income needs, tax situation, and risk tolerance. Every portfolio is stress-tested across bear markets, recessions, and inflationary periods before implementation.

Tax Planning

Taxes touch every financial decision—how investments are held, how retirement accounts are structured, when income is recognized. Proactive planning can reduce lifetime tax liability in ways that compound meaningfully over time.

Key strategies:

- Asset location: Vanguard research shows placing tax-inefficient assets in tax-deferred accounts adds 5-30 basis points of after-tax return annually

- Tax-loss harvesting: Selling investments at a loss to offset gains can generate 0.47% to 1.27% annually

- Roth vs. traditional contributions: Pre-tax contributions reduce current taxes; Roth contributions deliver tax-free withdrawals in retirement

Retirement Planning

Retirement planning for families involves more than maximizing 401(k) contributions. It requires projecting income needs, understanding Social Security timing, structuring withdrawals to last through potentially decades-long retirements, and protecting a spouse's income if one partner dies first.

Critical considerations:

- Life expectancy: A 65-year-old female can expect to live 20.1 more years; a male 17.5 years

- Social Security timing: Delaying benefits to age 70 increases payments by 8% annually past full retirement age

- Structured withdrawal strategies: "Bucket" approaches insulate near-term cash flow from market volatility by separating short-term needs from long-term growth assets

Sentinel has guided 2,000+ clients into retirement, using structured withdrawal buckets paired with growth-oriented allocations to protect against sequence-of-returns risk—so income keeps pace with the lifespan, not just the plan.

Insurance and Risk Protection

Insurance forms the safety net beneath everything else. Without it, a single event can unravel decades of planning.

Essential coverage:

- Life insurance replaces income for surviving family members

- Disability insurance protects earning power when illness or injury interrupts work

- Long-term care coverage prevents care costs from depleting retirement savings

- Umbrella liability shields family assets from civil judgments and lawsuits

40% of U.S. adults need life insurance or need more coverage. Young adults overestimate the cost of term life insurance by 10-12 times. Long-term care is even more critical: a private nursing home room costs $129,575 annually in 2025.

Coverage should be reviewed regularly as family circumstances change—marriage, children, home purchase, income increases, or approaching retirement.

Estate Planning

Estate planning protects assets, wishes, and relationships. It removes administrative burden and family conflict at exactly the moments when families are least equipped to handle them.

Essential documents:

- Will establishes how assets are distributed

- Powers of attorney designate who manages your finances if you're incapacitated

- Healthcare directives specify your medical treatment preferences in advance

- Beneficiary designations often override what a will says and must be reviewed after any major life change

Only 32% of Americans have a will. Dying without one forces your estate into probate court, where assets are distributed according to state law, not your wishes. Probate costs can consume 3-7% of an estate's value.

Much of estate planning doesn't require an attorney. Organizing asset titling, reviewing beneficiary designations, and coordinating accounts can be handled by a financial advisor, with legal counsel engaged for complex trusts or specialized structures.

Financial Challenges That Are Unique to Families

Families face financial pressures that don't show up in single-person planning. A strong family financial plan addresses them directly.

Raising Children and Education Costs

The financial weight of raising children extends from day-to-day costs through college. The USDA estimates that a middle-income, married-couple family will spend approximately $233,610 to raise a child born in 2015 through age 17—excluding college.

College adds significant expense. Average published costs for 2025-26:

- Public 4-year (in-state): $25,850 total

- Private nonprofit 4-year: $60,920 total

Early savings vehicles make these costs manageable without derailing retirement goals:

- 529 plans — Tax-advantaged college savings; 35% of families use them

- Custodial accounts — Flexible savings for children's expenses

- Intentional cash flow planning — Balancing current expenses with future needs

Supporting Aging Parents or Multigenerational Households

23% of U.S. adults are part of the "sandwich generation"—supporting children and aging parents simultaneously. This burden peaks in the 40s — 54% of Americans in that age group are managing both at once.

The financial impact is significant. 78% of family caregivers incur out-of-pocket expenses averaging $7,242 annually—26% of their income.

Planning strategies:

- Budget for potential care contributions — Anticipate needs before they become urgent

- Understand parents' own estate plans — Coordinate resources and expectations

- Address long-term care insurance — For aging family members to protect their assets and yours

Families with Special Needs Dependents

Families with a child or adult dependent with special needs face unique and complex financial considerations. Planning must preserve government benefit eligibility while ensuring lasting security.

Critical planning tools:

- Special needs trusts — Protect assets without disqualifying from SSI or Medicaid

- ABLE accounts — Allow savings for disability-related expenses; annual contribution limit is $19,000 for 2025-26

- Long-term care plans — Must extend well beyond parents' lifetimes

More than 1 in 4 U.S. adults (28.7%, over 70 million people) have some type of disability. Sentinel Asset Management has worked with special needs families for 25 years, guiding 20+ families through the benefit-eligibility decisions and long-term care structures these situations require.

Divorce and Financial Restructuring

Family finances don't only evolve through growth — sometimes they're reshaped by loss or separation. Divorce disrupts a financial plan at nearly every level at once:

- Asset division — Retirement accounts, real estate, and investments require careful restructuring

- Beneficiary designations — Must be updated immediately across all accounts and policies

- Revised retirement projections — Income, expenses, and timelines shift significantly for both parties

- Support obligations — Alimony and child support have lasting cash flow implications

Working through these changes with an advisor who understands the financial and emotional weight of divorce matters. Sentinel's team brings both professional expertise and personal experience to this work, helping clients rebuild a plan they can trust.

Building a Legacy: Estate and Wealth Transfer Planning

Legacy planning is the natural culmination of a family financial plan. It ensures that what you've built reaches the people and causes you care about, on your terms, with minimal friction and tax costs.

Having the Family Conversation

The most effective estate plans are built with family input, not revealed after death. Frame the conversation around vision—what the family wants its legacy to mean—rather than accounts and assets. This reduces conflict among heirs, aligns expectations, and gives the plan its greatest impact.

Wills, Trusts, and Beneficiary Designations

Foundational documents:

- Will — Establishes distribution wishes

- Trusts — Provide control, protection, and potential tax benefits (especially relevant for special needs dependents or minor children)

- Beneficiary designations — On retirement accounts and life insurance can override a will; review them regularly

Even modest, well-structured plans remove enormous burden from loved ones. Trusts can minimize tax exposure, avoid probate, and ensure assets reach the right people at the right time.

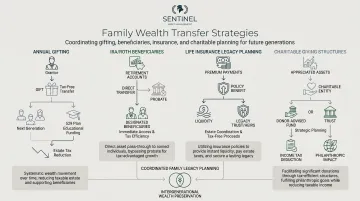

Wealth Transfer Strategies

Families use practical tools to transfer wealth efficiently:

- Annual gifting — $19,000 per recipient in 2025-26 without gift taxes; couples can jointly gift $38,000

- IRA/Roth beneficiaries — Name children or grandchildren to extend tax-advantaged growth

- Life insurance — Creates instant, tax-free legacy

- Charitable strategies — Reduce taxable estates while supporting causes you care about

Cerulli Associates projects $124 trillion in wealth will transfer through 2048—$105 trillion to heirs, $18 trillion to charities. That scale makes coordination with tax planning essential — the difference between a well-structured plan and a poorly timed one can mean tens of thousands of dollars lost to avoidable estate taxes before assets ever reach your beneficiaries.

Keeping the Plan Current

Legacy plans decay if not maintained. Marriages, divorces, births, deaths, and changes in tax law all require plan updates. Review key documents and beneficiary designations at least annually with a financial advisor. A single missed beneficiary update after a divorce, for instance, can redirect assets to the wrong person entirely.

What to Look for in a Family Financial Advisor

The right advisor makes the difference between a plan that works and one that sits in a drawer.

Key qualities to prioritize:

- Fiduciary duty — The advisor is legally required to act in your best interest

- Breadth of services — Can they address investments, tax, retirement, and estate together rather than in silos?

- Relevant experience — Have they guided families in situations similar to yours?

That last point — relevant experience — carries real weight. Look for advisors with documented track records across retirement transitions, estate structures, and family-specific challenges. Sentinel Asset Management, for example, draws on 100+ years of combined advisory experience, has guided 2,000+ clients into retirement, and maintains specialized expertise in special needs families and divorce financial planning across five offices.

Practical questions to ask before hiring:

- How are you compensated?

- Do you use an Investment Policy Statement?

- How do you coordinate across tax, investment, and estate planning?

- What happens to my plan when markets change?

Understanding an advisor's compensation model matters. Fee-only advisors are compensated solely by clients—no commissions. Fee structures vary:

| Fee Structure | Typical Range | Description |

|---|---|---|

| Assets Under Management (AUM) | 0.50% - 1.25% annually | Ongoing fee based on portfolio value managed |

| Flat/Retainer Fee | $2,000 - $8,000+ | Fixed annual or project-based fee for comprehensive planning |

| Hourly Rate | $200 - $400+ per hour | Billed for specific, as-needed advice |

Ask about compensation upfront to understand potential conflicts of interest.

Getting Started with Your Family Financial Plan

First steps:

- Gather your full financial picture — income, assets, debts, insurance, and any existing estate documents

- Clarify goals and risk tolerance — What matters most to your family? What keeps you up at night?

- Identify areas of greatest urgency — Often cash flow and protection gaps come first

An initial advisor conversation should be a listening session as much as an information-sharing one. A good advisor will ask about your family's full context, not just account balances. The outcome should be a clear, prioritized roadmap—not a list of products.

That's the approach Sentinel Asset Management takes from day one — each client receives a personalized Investment Policy Statement, built around their specific income needs, tax situation, and risk tolerance, developed through 100+ years of combined advisory experience.

Frequently Asked Questions

What are the 5 pillars of financial planning?

The five core pillars are cash flow and budgeting, investment management, tax planning, retirement planning, and estate/insurance planning. A comprehensive family financial plan integrates all five rather than treating them in isolation.

How much does a family financial advisor cost?

Fee structures vary: fee-only advisors charge hourly ($200–$400+), flat fees ($2,000–$8,000+), or AUM-based fees (0.50%–1.25% annually); commission-based and fee-based advisors earn differently. Ask about compensation models upfront — the structure directly affects whose interests the advisor is serving.

What is the 50 30 20 rule for family?

The rule allocates 50% of after-tax income toward needs, 30% toward wants, and 20% toward savings and debt. It's a useful starting framework for families, but households with special circumstances—dependents, high debt, near-retirement—may need a more tailored approach.

When should a family start financial planning?

The best time is as early as possible—ideally when major life events occur (marriage, first child, first job). That said, families 10–15 years from retirement still gain meaningful ground by formalizing a plan, particularly around tax strategy and income sequencing.

What does a family financial plan include?

A written financial plan typically covers a budget baseline, an investment policy statement, retirement income projections, insurance gap analysis, and an estate/legacy outline. Most families also include a review schedule — annual at minimum, or after major life changes — to keep the plan current.

How do I choose the right financial advisor for my family?

Start with fiduciary status — an advisor legally bound to act in your interest, not just recommend suitable products. From there, verify they offer holistic planning (not investments alone), have experience with families in comparable situations, and are transparent about how they're compensated.

Take the next step in your financial journey by exploring our courses page for upcoming live seminars.