General information, not personalised tax, legal or investment advice.

Introduction: Why This Planning Cannot Wait

Parents of children with special needs face a unique financial dilemma: you want to leave enough to ensure your child's long-term security and quality of life, yet a direct inheritance—even a modest one—can immediately disqualify them from essential government benefits like SSI and Medicaid. These means-tested programs remain tied to strict resource thresholds that haven't budged in decades. As of 2026, the SSI countable resource limit is still just $2,000 for an individual and $3,000 for a couple—the same ceiling that's been in place since 1989.

This planning is complicated by the dual timeline you're managing: your own retirement and legacy alongside your child's lifetime care needs, which will likely extend far beyond your years.

One mishandled inheritance, retirement account, or life insurance policy can unravel years of careful planning. It strips away the Medicaid coverage that funds daily care, housing support, and medical services.

This guide walks you through the key planning tools that protect your child's benefits while funding their future: special needs trusts (SNTs), ABLE accounts, guardianship designations, the letter of intent, and the funding strategies to support it all.

Sentinel Asset Management has spent 25 years helping parents of children with special needs coordinate exactly these tools — building financial plans that work across both timelines, so each decision has a clear purpose behind it.

Key takeaways

- Leaving assets directly to a child with special needs disqualifies them from SSI and Medicaid (resource limit: $2,000 individual, $3,000 couple)

- A third-party Special Needs Trust (SNT) passes wealth without triggering benefit loss

- ABLE accounts (expanded to age 46 eligibility in 2026) offer tax-advantaged savings for disability expenses

- Guardianship designation and a detailed Letter of Intent belong in every special needs estate plan

- Beneficiary designations on retirement accounts, life insurance, and annuities must name the SNT — not your child directly

Why Estate Planning Is Different When Your Child Has Special Needs

The $2,000 Cliff That Changes Everything

SSI and Medicaid are means-tested programs with unforgiving asset limits. The countable resource threshold remains $2,000 for an individual and $3,000 for a couple as of 2026, with no scheduled increases. If your child's countable assets exceed this limit by even $1, they lose eligibility immediately—no grace period, no exceptions.

Parents naturally want to leave enough for their child to live comfortably. The problem is that a direct inheritance—whether from a will, a life insurance policy, or a retirement account—becomes a countable resource the moment it's received. Even a $10,000 bequest from a well-meaning grandparent can trigger immediate suspension of benefits that fund housing, medical care, and daily support.

What Government Benefits Cover (And What They Don't)

SSI provides monthly payments to people with disabilities who have little or no income or resources to meet basic needs for food and shelter. Medicaid covers mandatory services including inpatient and outpatient hospital care, physician services, lab work, and home health services.

What's typically not covered:

- Specialized therapies and out-of-network care

- Personal care aides beyond program limits

- Non-medical transportation

- Recreational programs and social activities

- Assistive technology and adaptive equipment

- Educational supports and enrichment programs

This is why supplemental private funds matter even when benefits remain intact. Government programs cover the basics; private planning fills the gap between survival-level support and a genuinely full life. That gap is where estate planning decisions become consequential.

Why Every Default Estate Plan Becomes Dangerous

Every common estate planning default—naming your child as a direct beneficiary on a will, retirement account, or life insurance policy—disqualifies them from means-tested benefits the moment funds are received. The solution requires a completely restructured approach: the trust receives the inheritance, not the child.

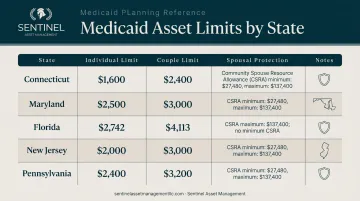

State rules add another layer of complexity. Medicaid eligibility varies significantly depending on where your family lives:

| State | Individual Asset Limit | Key Considerations |

|---|---|---|

| CT | $1,600 | Lower than federal SSI threshold; multiple waiver programs |

| MD | $2,500 | Higher than SSI; Community Pathways waiver available |

| NJ | $2,000 | WorkAbility program removes asset limits for working disabled individuals |

| PA | $2,000 | Community HealthChoices waiver; strict SSI alignment |

| MA | $2,000 | Multiple HCBS waivers; MassHealth-specific rules |

Families moving across state lines must re-evaluate their entire estate plan. A trust compliant in Connecticut may not meet Maryland's specific Medicaid requirements. An advisor familiar with your state's specific waiver programs and asset rules can identify compliance gaps before they become costly mistakes.

The Special Needs Trust: Your Most Important Planning Tool

A Special Needs Trust (SNT)—also called a supplemental needs trust—is a legal arrangement that holds assets for the benefit of a person with disabilities without those assets counting toward eligibility for means-tested government benefits. The trust, not the child, owns the assets.

Third-Party SNT (The Most Common Choice for Parents)

A third-party SNT is created and funded by someone other than the beneficiary—typically parents or grandparents. It can receive gifts, inheritances, and life insurance proceeds. Importantly, it does not require a Medicaid payback provision upon the beneficiary's death, meaning remaining assets can pass to siblings or other heirs.

What trust funds can cover:

- Medical and dental care not covered by benefits

- Therapy, counseling, and specialized treatments

- Education, tutoring, and job training

- Transportation and vehicle modifications

- Recreation, travel, and entertainment

- Personal items, clothing, and technology

- Private caregivers and companion services

What funds cannot cover without penalty: Distributions for food and shelter trigger In-Kind Support and Maintenance (ISM) rules, which reduce SSI payments by the Presumed Maximum Value. The trust can still pay these expenses, but you'll need to account for the SSI reduction.

First-Party and Pooled SNTs

A first-party (self-settled) SNT is used when the child with special needs already owns assets—through an inheritance, lawsuit settlement, or prior savings. It must be established before age 65 and carries a Medicaid payback requirement: upon death, remaining assets must first reimburse the state for benefits provided during the beneficiary's lifetime.

Pooled trusts offer a nonprofit-administered alternative. They're accessible for those over 65 or with smaller asset amounts. Individual sub-accounts are pooled for investment efficiency while still qualifying as supplemental needs trusts. This makes them a practical option for families who can't meet the high minimums—often $500,000 or more—required by corporate trustees.

Choosing and Structuring the Trustee Role

The trustee carries enormous responsibility:

- Distributing funds without jeopardizing benefits

- Staying current with evolving SSI and Medicaid rules

- Managing investments and tax filings

- Keeping detailed records for audits

- Understanding the beneficiary's specific needs and preferences

Given that weight, how you structure the role matters as much as who fills it.

Separate the trustee and legal guardian roles to create checks and balances. The trustee controls the money; the guardian makes personal and medical decisions. Also name backup successor trustees—including professional fiduciaries or trust companies—in case the primary trustee cannot serve.

How to Fund a Special Needs Trust

The most important financial question: how much will your child need over their lifetime, and how much will you actually have to fund the trust? A gap analysis—accounting for your child's life expectancy, estimated care costs, inflation, and expected government benefits—is the foundation of any funding strategy. Three funding tools do most of the heavy lifting.

Life Insurance: The Most Efficient Funding Tool

Life insurance delivers a death benefit income- and estate-tax-free directly to the SNT, creating an immediate pool of capital even if you haven't accumulated substantial investment assets. Many financial planners recommend survivorship (second-to-die) policies for SNTs because they pay out when the second parent dies—exactly when the trust needs capital most.

Update Beneficiary Designations Everywhere

Retirement accounts (IRAs, 401(k)s), existing life insurance, annuities, and real estate must name the SNT as beneficiary rather than the child directly. This is the most commonly overlooked step, and it can inadvertently transfer assets in a way that destroys benefit eligibility.

The Sibling Equation

If you plan to divide your estate among multiple children, the portion intended for the child with special needs must be routed through the SNT, not given outright. Consider whether to equalize the estate or weight it toward the child with special needs based on:

- Your other children's financial independence

- The severity and cost of your child's needs

- Family dynamics and sibling relationships

- Long-term care and housing requirements

Sentinel Asset Management has worked with families navigating these decisions for 25 years. That experience informs how the firm approaches funding gap analysis, portfolio structuring within the trust, and beneficiary designation reviews—ensuring the financial plan and the legal estate plan reinforce each other rather than work at cross-purposes.

Guardianship, the Trustee, and the Letter of Intent

Guardian vs. Trustee: Why Both Roles Matter

Parents must name two decision-making roles:

- Legal guardian: Makes personal and medical decisions for the child when parents cannot

- Trustee: Manages the trust's finances

Keeping these roles separate is the standard recommendation — it creates accountability and prevents conflicts of interest. Your most financially savvy sibling may not be the best choice to oversee daily care decisions.

The Letter of Intent: Non-Legal, But Critical

The Letter of Intent is a non-legal document that communicates everything a future caregiver needs to know:

- Your child's daily routine and preferences

- Complete medical history and current treatments

- Behavioral triggers, comforts, and communication style

- Preferred doctors, therapists, and care providers

- Social connections and community involvement

- Educational needs and learning approaches

- Personal goals and aspirations

While it has no legal force, it's often the most important document in the entire plan for ensuring continuity of quality care. Update it annually as your child's needs and preferences evolve.

Name Multiple Successors in Priority Order

Name at least two successor guardians and two successor trustees, listed in priority order. Life circumstances shift — illness, relocation, strained relationships, or financial changes can disqualify even the most committed person over time.

When selecting successors, consider:

- Longevity and proximity: Will this person realistically be available in 10 or 20 years?

- Alignment with your child's values: Do they know your child, not just your family?

- Financial literacy (for trustees): Can they manage distributions, file accountings, and work with advisors?

- Emotional capacity: Caring for a loved one with special needs is rewarding but demanding

If family options become limited, professional fiduciaries — licensed individuals or trust companies — can serve as trustees. They bring institutional accountability and continuity that no individual can guarantee. Revisit all designations every three to five years, or after any major family change.

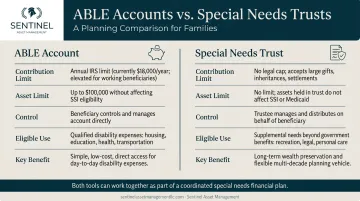

ABLE Accounts: A Tax-Advantaged Complement to the SNT

ABLE accounts under the Achieving a Better Life Experience Act are tax-advantaged savings accounts for individuals whose qualifying disability began before age 26 (rising to age 46 in 2026 per SECURE 2.0). Contributions grow tax-deferred and withdrawals for qualified disability expenses are federal income tax-free.

Beyond the tax benefits, ABLE accounts also carry an important asset protection feature: balances up to $100,000 do not count against SSI resource thresholds. If the balance exceeds $100,000, SSI payments are suspended — but Medicaid coverage continues.

How ABLE accounts complement the SNT:

- Ideal for smaller, more accessible day-to-day spending needs

- Can be managed directly by the beneficiary when appropriate

- SNT holds larger, long-term assets

- Families can use both simultaneously to maximize flexibility

Contribution limits to keep in mind:

- Annual contributions are capped at the gift tax exclusion ($19,000 in 2026)

- 529-to-ABLE rollovers count toward that annual limit

- Employed beneficiaries may contribute above the standard limit under the ABLE to Work Act, up to an additional $14,580 in 2026

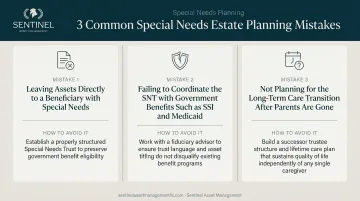

Common Mistakes Parents Make in Special Needs Estate Planning

Even carefully constructed plans can unravel due to a few predictable, avoidable errors. These three come up most often.

Mistake 1: Leaving Assets Directly to Your Child

A grandparent leaving a bequest directly to a grandchild—even with the best intentions—can destroy benefit eligibility. All family members involved in the estate plan need to know the SNT exists and must direct any gifts through it, not to the child personally.

Mistake 2: Creating the Trust but Never Funding It

A trust document without assets behind it is just paper. Parents need to actively build their funding strategy — life insurance, redirected savings, updated beneficiary designations — throughout their lives, not only at the end.

Mistake 3: Treating the Plan as a One-Time Task

Government benefit rules change. Medicaid thresholds shift. Your child's needs evolve. Review the plan every 3–5 years or after any major life event, and update the Letter of Intent annually. A plan that was sound five years ago may have real gaps today.

Frequently Asked Questions

What is the average cost for a special needs trust?

Attorney fees to draft a third-party SNT typically range from $2,000 to $8,000 depending on complexity and state. Ongoing trustee fees—especially for professional trustees—run 1% to 2% of assets annually. Pooled trusts offer lower barriers to entry, with setup fees around $500 to $2,500.

Should a special needs trust be revocable or irrevocable?

Third-party SNTs are generally irrevocable once funded to protect assets and preserve the beneficiary's benefits eligibility. Trustee discretion provisions can build in meaningful flexibility within that structure.

What is the best way to leave your estate to children with special needs?

Route all intended assets through a properly drafted third-party SNT—never by direct bequest or beneficiary designation. Coordinate all estate documents, life insurance, and retirement account beneficiary designations to reflect this structure. Any asset that bypasses the trust puts your child's government benefits eligibility at risk.

Can survivors' benefits for a child with special needs be placed in a special needs trust?

Social Security survivors' benefits go directly to the child or their representative payee — federal anti-assignment laws block redirecting them into an SNT. The SNT can still hold and manage other inherited assets alongside those benefits. Consult a special needs attorney for state-specific guidance.

What happens to a special needs trust when the beneficiary dies?

For a third-party SNT, remaining assets pass to whomever the trust creator designated (such as siblings), with no Medicaid payback requirement. For a first-party SNT, remaining assets must first reimburse the state for Medicaid benefits provided during the beneficiary's lifetime before any balance passes to other heirs.

What are common mistakes to avoid in special needs estate planning?

Three mistakes consistently derail special needs estate plans:

- Naming the child directly as a beneficiary instead of the SNT

- Failing to fund the trust adequately during your lifetime

- Not reviewing the plan as laws, benefit rules, and family circumstances evolve

Take the next step in your financial journey by exploring our courses page for upcoming live seminars.