General information, not personalised tax, legal or investment advice.

The truth is, generic retirement advice fails precisely because it doesn't account for the life you've actually lived. Target-date funds and age-based withdrawal rules optimize for averages, not for you. They don't consider your specific tax situation, your family obligations, or what you want your wealth to achieve after you're gone.

This guide answers two critical questions: how to build a retirement income strategy that sustains your lifestyle for 25-30 years, and how to ensure your wealth reaches the people and causes you care about—on your terms, with minimal friction or tax cost.

This guide is for: individuals and families within 10-20 years of retirement, those who feel their financial plan lacks cohesion, and anyone who hasn't thought beyond "saving enough" to what comes next.

Key takeaways

- Retirement planning is personal — income needs, tax situation, risk tolerance, and life circumstances all shape the right strategy

- Retirement and legacy goals require coordinated planning from day one, not as separate phases

- A bucket withdrawal strategy shields near-term cash needs from market swings while keeping long-term assets growing

- Inflation, longevity, and sequence-of-returns risk are the three forces most likely to erode retirement income

- Most estate planning decisions don't require an attorney — your financial advisor handles the heavy lifting

Why Generic Retirement Plans Leave People Exposed

One-size-fits-all retirement advice optimizes for averages, not for individuals. Standardized tools like age-based contribution rules and generic target-date funds can't account for your unique tax exposure, Social Security timing, or family obligations.

Despite decades of disciplined saving, 58% of Americans are not on track to maintain their current lifestyle in retirement. The Employee Benefit Research Institute projects a $3.48 trillion aggregate savings shortfall across U.S. households — a gap driven less by bad intentions than by plans that were never built for real people.

Common Blind Spots of Generic Plans

Most off-the-shelf plans fail to address:

- Tax drag across income sources — No coordinated strategy for which accounts to withdraw from first

- Social Security timing — Claiming at 62 versus 70 can mean hundreds of thousands in lifetime benefits lost

- Long-term care costs — Fidelity estimates a 65-year-old retiring in 2025 will spend $172,500 on healthcare alone throughout retirement, excluding long-term care

- Legacy intentions — Left entirely as an afterthought at the end of life

Each of these gaps compounds the others. Personalized planning addresses them together — mapping income sources, liabilities, tax exposure, family obligations, and legacy intentions before a single investment decision is made.

The Two Goals That Should Guide Every Retirement Plan

Most people treat retirement income planning and legacy planning as sequential: first survive retirement, then worry about what you leave behind. This is a costly mistake.

Decisions made early in retirement—about withdrawals, account structure, and risk—can sharply limit your legacy options later. The two goals must be coordinated from the start.

Retirement Income: Sustaining the Life You've Built

A retirement income goal means more than hitting a savings number. It means replacing the right percentage of pre-retirement income while accounting for how expenses shift.

The 70-85% income replacement rule: The Social Security Administration notes that most retirees need 70-75% of final earnings to maintain their lifestyle, with lower earners needing 85-90%. A 2016 GAO review of 52 studies found a median recommended target of 77%.

Retirement lasts longer than you think. While expenses decline roughly 1% per year due to natural consumption changes, healthcare costs rise sharply. Planning for only 15-20 years leaves you dangerously exposed.

The Longevity Reality

Using Social Security Administration actuarial data:

| Demographic | Probability of Reaching Age 85 | Probability of Reaching Age 90 |

|---|---|---|

| Male | 41.8% | 21.3% |

| Female | 54.1% | 32.3% |

Source: SSA Actuarial Life Table

Key insight: With a roughly 1-in-3 chance a 65-year-old woman will live to 90, retirement income plans must be stress-tested across a 30-year horizon.

Identify and sequence all income sources:

- Social Security (claiming age impacts lifetime benefits by hundreds of thousands)

- Pension income if applicable

- Portfolio withdrawals

- Other income streams (rental property, part-time work)

Legacy: Ensuring Your Wealth Reflects Your Values

Legacy goals extend beyond passing wealth to heirs. They include:

- Charitable intentions and donor-advised fund strategies

- Securing a spouse's long-term financial needs

- Supporting children or grandchildren's milestones

- Providing for dependents with special needs

Defining legacy goals early allows every financial decision—account titling, beneficiary designations, investment structure, tax strategy—to align with those intentions from the start, not patched in later. When these decisions are made together, wealth reaches the right people, in the right amounts, with less tax cost and far less friction for the people you leave behind.

Building Your Personalized Retirement Income Strategy

Genuinely tailored planning requires understanding your investment goals, income needs in retirement, tax situation, risk tolerance, and time horizon before any recommendations are made.

That foundation shapes everything. Sentinel Asset Management formalizes it through an Investment Policy Statement for each client: a written document that governs every portfolio decision, stress-tested under different market conditions and monitored continuously for style drift.

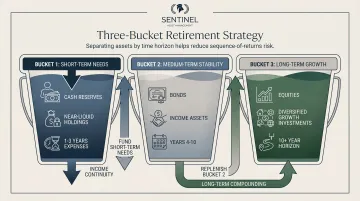

The Bucket Strategy: Protecting Income From Market Volatility

The bucket withdrawal framework divides assets into three pools:

- Short-term bucket: Cash and near-liquid assets covering 1-3 years of expenses

- Medium-term bucket: Bonds and income-generating assets for years 4-10

- Long-term bucket: Growth equities and diversified stocks for a 10+ year horizon

Near-term living expenses stay insulated from market downturns — retirees don't have to sell growth assets at depressed prices to cover day-to-day needs. When markets drop 30% in year two of retirement, your short-term bucket remains untouched, giving long-term assets time to recover.

Tax-Efficient Withdrawal Sequencing

Which account you withdraw from first — taxable, tax-deferred (traditional IRA/401k), or tax-free (Roth) — significantly impacts lifetime tax liability.

Coordinated withdrawal sequence reduces taxes over 20-30 years:

- Taxable accounts first — spend cash, dividends, interest, gradually liquidating principal

- Tax-deferred accounts strategically — traditional IRAs and 401(k)s when tax brackets allow

- Tax-free accounts last — preserve Roth accounts for maximum tax-free growth

The Pre-RMD Roth Conversion Window

The years between retirement and Required Minimum Distributions offer a unique low-tax window. Proactive Roth conversions during this period can meaningfully reduce lifetime tax liability.

RMD age under SECURE 2.0:

| Birth Year / Age Milestone | RMD Starting Age |

|---|---|

| Turned 72 after Dec 31, 2022, and turn 73 before Jan 1, 2033 | Age 73 |

| Turn 73 after Dec 31, 2032 | Age 75 |

Source: Congressional Research Service

Executing these conversions effectively requires coordinating your investment plan with your current and projected tax picture — which is why advisors who manage both together can capture opportunities a siloed approach would miss.

Portfolio Construction for Long-Term Resilience

In practice, a globally diversified, tax-efficient portfolio means:

- Asset allocation based on time horizon — appropriate mix of stocks, bonds, and alternatives

- Exposure to different geographies and asset classes — domestic, international developed, emerging markets

- Rebalancing discipline — systematic adjustments to maintain target allocation

This approach is rooted in modern portfolio theory, building on Harry Markowitz's Nobel Prize-winning work. Deliberate diversification eliminates unsystematic (avoidable) risk, leaving only the systematic market risks no investor can escape.

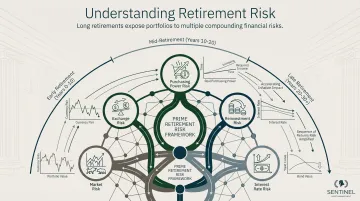

Understanding and Managing the Risks That Threaten Retirement

Retirement planning is as much about risk identification as return generation. Most people understand market risk but underestimate the others.

The Five Risks Every Retiree Faces

Sentinel's PRIME risk framework identifies the systematic risks that remain after proper diversification:

- Purchasing Power Risk: Inflation eroding spending ability over decades

- Reinvestment Risk: Lower returns when income is reinvested at unfavorable rates

- Interest Rate Risk: Impact on bond values and income-generating assets

- Market Risk: Sequence-of-returns risk that can permanently impair a portfolio when losses hit early in retirement

- Exchange Risk: Currency fluctuations affecting international holdings or global income sources

Each of these risks compounds over a 20- to 30-year retirement — which is why longevity risk, the sixth threat, may be the most consequential of all.

Longevity Risk: The Risk Most Plans Ignore

Longevity risk is the possibility of outliving your money. With a 65-year-old woman having a 32.3% chance of living to 90, a plan built for 15 years fails someone who lives 30.

Strategies to address longevity risk:

- Delayed Social Security claiming (age 70 versus 62 increases monthly benefits by 76%)

- Annuity income layers for guaranteed lifetime payments

- Longevity reserves built into portfolio stress-testing

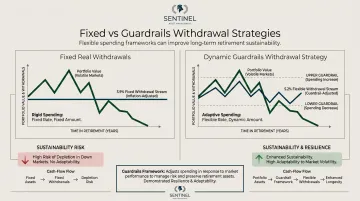

Sequence-of-Returns Risk and Dynamic Spending

Vanguard research shows investors who retire into a bear market with fixed withdrawal strategies are 31% more likely to outlive their wealth. The sequence of returns matters as much as the average return itself.

The new safe withdrawal reality: Morningstar's 2026 research establishes 3.9% as the safe starting withdrawal rate for a fixed 30-year retirement, refining the traditional 4% rule.

Dynamic spending strategies boost safety:

| Withdrawal Strategy | Starting Rate | Mechanism |

|---|---|---|

| Fixed Real Withdrawals | 3.9% | Adjusted annually for inflation only |

| Guardrails Method | 5.2% | Withdrawals decrease after losses, increase after gains |

Source: Morningstar State of Retirement Income 2026

Adopting flexible guardrails allows you to safely boost initial withdrawal rates from 3.9% to 5.2% while maintaining portfolio sustainability.

Stress-Testing Your Plan

What happens if markets decline 30% in year two of retirement? What if inflation runs at 4% for a decade?

Sentinel stress-tests every client plan before and during retirement, modeling it against historical bear markets, recessions, and prolonged inflationary periods. A plan that only looks sound on paper at construction can fail badly under 2000-era or 2008-era conditions. Testing reveals which risks are manageable and which require structural changes to the withdrawal strategy itself.

Legacy Planning: Ensuring Your Wealth Outlasts You

A legacy plan is more than a will. It's the full architecture of how your assets transfer — who receives what, how quickly, and at what tax cost. The core components that determine this outcome include:

- Beneficiary designations — supersede your will on every account where they're named

- Account titling — how assets are owned dictates the transfer mechanics at death

- Trusts where the situation calls for them: special needs trusts, charitable remainder trusts

- Charitable giving vehicles such as donor-advised funds and Qualified Charitable Distributions

Most people assume legacy planning requires expensive legal infrastructure at every step. In practice, many estate planning decisions can be made in coordination with a financial advisor.

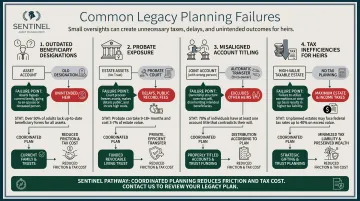

How Legacy Plans Fail in Practice

Common failure points include:

- Outdated beneficiary designations — Only 65% of adults 50+ have designated beneficiaries for all financial accounts

- Assets passing through probate unnecessarily — The average probate process lasts 20 months and costs 3-7% of estate value

- Lack of coordination between will and account ownership — Beneficiary designations override wills, creating unintended outcomes

- Failure to account for tax consequences — Heirs inheriting tax-deferred accounts face immediate tax liabilities

For most families, these gaps aren't intentional — they're the result of plans that were set up once and never revisited. Families with dependents who have disabilities face these same risks, compounded by an additional layer of complexity.

Special Needs Planning

Standard inheritance approaches can inadvertently disqualify a loved one from public benefits like SSI or Medicaid — even when the intent was to provide for them.

A special needs trust or alternative structure preserves government benefit eligibility while providing supplemental support. Sentinel has 25 years of experience working with families with special needs, supporting 20+ families long term through coordinated financial, legal, and care planning.

When Your Circumstances Require a Specialized Approach

Certain life situations make personalized planning even more critical:

- Families with a dependent with a disability: Financial security must extend beyond the client's lifetime, requiring multi-generational trust structures and coordinated care planning.

- Individuals navigating divorce: Assets must be divided, retitled, and replanned for a newly single financial future. Sentinel's advisors bring direct experience with divorce's financial and emotional complexity — from both personal and professional perspectives.

- Concentrated positions in employer stock or illiquid business interests: These create unsystematic risk that requires deliberate diversification and tax-efficient transition planning.

These situations require advisors with direct experience in the financial, legal, and emotional complexity involved — not advisors who are simply familiar with the textbook answers.

Frequently Asked Questions

How many Americans have $1,000,000 in retirement savings?

Only 4.6% of U.S. households hold more than $1 million in retirement assets, rising to 9.2% among those ages 55-64. Reaching a specific number matters less than building a personalized income strategy that sustains your lifestyle for as long as you need it.

What is the difference between retirement planning and legacy planning?

Retirement planning focuses on generating sustainable income during your lifetime, while legacy planning ensures your remaining wealth transfers efficiently to people or causes you care about. Both must be coordinated from the start, not treated as separate phases, because early retirement decisions about withdrawals and account structure significantly impact legacy options later.

When should I start personalizing my retirement financial plan?

The best time is 10-20 years before retirement, when there's still time to adjust savings rates, refine account structures, and establish tax strategies. That said, personalized planning helps at any stage—including in retirement itself—through tax-efficient withdrawal sequencing and risk management.

What is a bucket strategy and how does it protect retirement income?

The bucket strategy divides assets into pools by time horizon: short-term cash for near-term needs, medium-term bonds for income, and long-term equities for growth. This structure ensures retirees don't need to sell growth assets during market downturns to fund living expenses, protecting against sequence-of-returns risk.

How does personalized planning help reduce taxes in retirement?

Coordinated withdrawal sequencing, Roth conversions, and Social Security timing can reduce lifetime tax burden considerably. Each decision affects the others, so they must be made together as part of a unified plan—not in isolation—given their compounding impact across 20-30 years of retirement.

Do I need a lawyer to create a legacy or estate plan?

Most foundational decisions—beneficiary designations, account titling, charitable giving strategies—can be made with a financial advisor. Legal involvement is typically needed only for complex trusts or contested estates, not for the financial coordination that makes up the bulk of estate planning.

Take the next step in your financial journey by exploring our courses page for upcoming live seminars.