General information, not personalised tax, legal or investment advice.

Introduction

Most people spend decades systematically saving for retirement — contributing to 401(k)s, maxing out IRAs, building investment accounts — but give little structured thought to how they'll actually generate reliable income once paychecks stop. The shift from accumulation (growing a nest egg) to distribution (living off it) is where most retirement plans fall short.

According to the 2024 EBRI Retirement Confidence Survey, while 52% of workers have tried to calculate how much they'll need in retirement, only 41% have thought through how to withdraw that money sustainably.

Here's the central question: beyond managing investments, can a financial advisor actively help you pull more income from what you've saved, reduce unnecessary taxes, and ensure your money lasts as long as you do? The answer is yes. This article breaks down the specific strategies advisors use to increase withdrawal efficiency, cut tax drag, and build income that holds up for decades.

Key takeaways

- A financial advisor helps convert savings into sustainable income, not just grow a portfolio

- Social Security timing, tax-efficient withdrawals, and Roth conversions are high-impact income levers

- Sequence-of-returns risk and taxes quietly erode retirement income — and both respond well to proactive planning

- Structured withdrawal strategies protect near-term income from market volatility

- A skilled advisor typically delivers 3–5% in net returns, which exceeds the cost of their fees

The Retirement Income Problem Most People Don't See Coming

Having a $1 million portfolio doesn't automatically translate into reliable, lasting income. The distribution phase of retirement requires an entirely different skill set than the accumulation phase — and without a deliberate strategy, even well-funded retirees can run short.

The Risks That Erode Retirement Income

Even after a lifetime of disciplined saving, several critical risks threaten retirement sustainability:

Longevity Risk: According to the Society of Actuaries' longevity illustrator, a 65-year-old couple has a 50% chance that at least one spouse will survive to age 92. Planning for a 20-year retirement might not be enough when you could easily live 30+ years.

Healthcare Inflation: Fidelity estimates that a single 65-year-old retiring in 2025 will need $172,500 for healthcare costs (excluding long-term care and dental). For couples with high prescription needs, the Employee Benefit Research Institute projects total healthcare expenses could reach $469,000 for a 90% chance of covering costs.

Sequence-of-Returns Risk: Losing money early in retirement does lasting damage. When withdrawals continue through a market decline, you sell more shares to generate the same income — shares that won't be there to recover when markets rebound.

Purchasing Power Decline: The Bureau of Labor Statistics Consumer Price Index shows that $100,000 in purchasing power in December 1994 required $210,800 by December 2024 to maintain the same buying power — a 111% increase over 30 years.

These Risks Don't Manage Themselves

Each of these risks compounds the others. Inflation shrinks fixed income just as healthcare costs climb. A market downturn in year two of retirement, combined with steady withdrawals, can permanently reduce the assets available for the next 25 years.

Without a coordinated strategy, retirees often withdraw from the wrong accounts at the wrong time, pay more taxes than necessary, and gradually erode the portfolio they spent decades building. That's precisely where professional guidance makes a measurable difference.

How a Financial Advisor Can Increase Your Retirement Income

Social Security Optimization

Claiming at age 62 results in a 30% permanent reduction in benefits, yet 27% of beneficiaries still claim as soon as eligible. This single decision can mean tens of thousands of dollars over a lifetime.

Advisors analyze optimal claiming age based on:

- Health status and family longevity

- Spousal benefit coordination

- Other income sources that can fund early retirement years

- Break-even analysis comparing claiming ages

Delaying benefits beyond Full Retirement Age yields an 8% annual increase through Delayed Retirement Credits, up to age 70. For married couples, coordinating spousal benefits and survivor benefits adds another layer of complexity where professional analysis delivers measurable value.

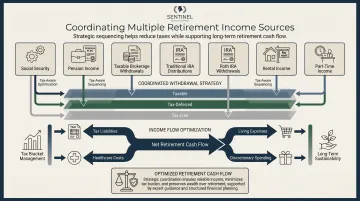

Coordinated Income Source Planning

Social Security optimization is just one piece. Advisors build a coordinated distribution plan across all income sources — pensions, 401(k) withdrawals, part-time income, rental income — that:

- Sequences withdrawals across income sources to minimize lifetime taxes

- Identifies which income sources to tap first based on tax efficiency

- Integrates Required Minimum Distributions (RMDs) into the broader strategy

- Adjusts annually as circumstances change

Sentinel Asset Management designs structured withdrawal plans coordinated across taxable, tax-deferred, and tax-free accounts to pursue steady income throughout retirement while protecting against sequence-of-returns risk.

RMD Planning and Roth Conversions

Before RMDs begin at age 73, advisors help clients execute pre-RMD Roth conversions during lower-income years — early retirement, before Social Security kicks in. Converting portions of traditional IRA/401(k) funds to Roth creates a pool of tax-free income and reduces future RMD burden.

This matters because of the "tax torpedo" — the point in later retirement when Social Security, RMDs, and other income sources converge, pushing retirees into unexpectedly higher brackets. Strategic conversions defuse it before it triggers.

Portfolio Income Optimization

Advisors build portfolios around income-generating assets — dividend payers, bonds, and fixed annuities for a guaranteed income floor — structured to produce reliable cash flow without forcing sales during downturns. This approach provides:

- Consistent income from dividends and interest

- Reduced need to sell equities during bear markets

- Tax-efficient income streams (qualified dividends taxed at lower rates)

- Growth potential to combat inflation over 20-30 year horizons

Behavioral Coaching as Income Protection

Emotional decision-making destroys retirement income. J.P. Morgan Asset Management research shows that missing just the 10 best market days over a 20-year period cuts portfolio returns from 9.8% to 5.6%.

The 2025 DALBAR Quantitative Analysis of Investor Behavior put a number on this: the average equity investor earned 16.54% in 2024 against the S&P 500's 25.02% return — an 848 basis point gap driven almost entirely by behavior, not markets.

Advisors prevent the panic-selling that creates this gap, keeping clients invested through full market cycles and protecting the long-term income their portfolios were built to generate.

Healthcare and Long-Term Care Planning

Healthcare is one of the fastest-growing retirement expenses — and one of the most underfunded. Advisors address it on multiple fronts. HSAs offer a triple-tax advantage that most retirees underuse. Medicare enrollment timing and supplement selection can mean thousands in avoidable costs. For long-term care, advisors weigh insurance coverage against self-insurance based on assets, health history, and family dynamics — then build dedicated reserves so care costs never cannibalize primary income.

Tax Efficiency: The Silent Income Booster

Every dollar not paid unnecessarily in taxes is a dollar that stays in your pocket. Advisors don't just manage investments — they coordinate a tax strategy across your entire financial picture.

Asset Location Strategy

Vanguard's Advisor's Alpha research found that optimal asset location can add up to 60 basis points of return annually without increasing risk. The strategy: place tax-inefficient assets (bonds, REITs) in tax-advantaged accounts and tax-efficient assets (index funds, growth stocks) in taxable ones.

Withdrawal Sequencing

The order in which you withdraw from accounts matters. The same research shows that sequencing withdrawals correctly — RMDs first, then taxable accounts, then tax-advantaged assets — can add up to 120 basis points of value annually. Done right, this approach:

- Avoiding premature depletion of tax-deferred accounts

- Preserving tax-free Roth assets for later years

- Managing annual tax brackets to avoid bracket creep

Roth Conversion Laddering

Converting traditional retirement funds to Roth during low-income years — typically the window between retirement and when Social Security and RMDs begin — locks in lower tax rates now and generates tax-free income later. If today's rate is lower than the expected future rate on those funds, conversion makes sense.

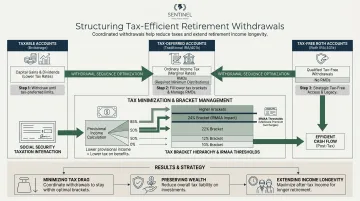

Tax-Bracket Management

Advisors engineer annual withdrawals to "fill up" lower tax brackets efficiently, avoiding inadvertent jumps into higher brackets that trigger:

- Medicare IRMAA surcharges: Crossing $106,000 (single) or $212,000 (joint) in modified adjusted gross income triggers Part B premium increases from $185 to $259 monthly

- Social Security taxation thresholds: Combined income above $34,000 (single) or $44,000 (joint) makes up to 85% of benefits taxable

Sentinel Asset Management treats taxable, tax-deferred, and tax-free accounts as a single coordinated plan — not three separate buckets. Each year's withdrawals are structured to draw from the most tax-efficient source available, reducing lifetime tax liability rather than just managing it year to year.

Building a Withdrawal Strategy That Doesn't Run Out

Why Withdrawal Sequencing Matters

Which accounts you draw from first — taxable, tax-deferred, or tax-free — has a major impact on both how long money lasts and how much tax you pay. There is no universal right answer; it depends on your individual tax situation, income needs, and legacy goals.

The Bucket Strategy

Advisors use a practical framework that segments assets by time horizon:

Near-Term Bucket (1-3 years): Held in stable, liquid assets (cash, money market funds, short-term bonds) so market volatility never forces selling at a loss. This bucket funds immediate living expenses.

Medium-Term Bucket (4-10 years): Invested in more conservative assets (balanced funds, intermediate bonds, dividend stocks) that provide modest growth while maintaining stability.

Long-Term Bucket (10+ years): Allocated to growth assets (equities, real estate) given time to recover from downturns and keep pace with inflation across a 20-to-30-year retirement.

Sentinel Asset Management uses structured withdrawal buckets as part of its personalized planning process, supported by Investment Policy Statements stress-tested under different market scenarios including historical bear markets, recessions, and inflationary periods.

Sustainable Withdrawal Rate Planning

William Bengen's 1994 research established the "4% rule" — a first-year withdrawal of 4%, followed by inflation-adjusted withdrawals. However, Morningstar's 2025 State of Retirement Income report suggests that 3.9% is the highest safe withdrawal rate for a 30-year retirement with 90% success probability using forward-looking return forecasts.

The good news: dynamic "guardrails" approaches that adjust spending based on portfolio performance can safely boost starting withdrawal rates to 5.7%. This flexible approach allows retirees to spend more in good years and trim modestly in down years, maximizing lifetime income without running out of money.

Ongoing Calibration

Those guardrails only work if someone is watching. Advisors revisit withdrawal strategies as:

- Markets fluctuate and portfolio values change

- Tax laws evolve

- Health conditions and care needs shift

- Spending patterns change over retirement phases

Regular reviews catch drift early — before a tax law change or an unexpected health cost quietly erodes what looked like a solid plan.

Is Hiring a Financial Advisor Worth the Cost?

What Advisors Cost

Financial advisors typically charge:

- Assets Under Management (AUM): 100 to 120 basis points for portfolios under $1 million; 80 to 100 basis points above $2 million

- Hourly Rates: $300 per hour median

- Flat Fees: Vary by complexity and service scope

What Advisors Deliver

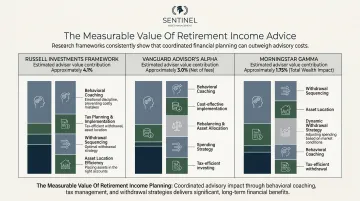

Leading research frameworks quantify the value of professional advice:

| Framework | Total Value | Key Contributors |

|---|---|---|

| Russell Investments (2025) | 4.87% | Behavioral coaching (2.47%), Family wealth planning (1.13%), Tax planning (0.97%) |

| Vanguard Advisor's Alpha | ~3.00% | Behavioral coaching (0-200+ bps), Withdrawal order (0-120 bps), Asset location (0-60 bps) |

| Morningstar Gamma | 1.59% | Dynamic withdrawals (0.70%), Asset allocation (0.45%), Asset location (0.23%) |

Across all three frameworks, the quantified value of advice outpaces the typical 1% advisory fee — often by a factor of two or three.

Who Benefits Most

Professional retirement income guidance delivers the greatest value for:

- Individuals within 5-10 years of retirement

- Those with multiple income sources to coordinate (Social Security, pension, retirement accounts, rental income)

- Retirees with significant tax-deferred account balances facing large RMDs

- Anyone without a clear, tested withdrawal plan

Beyond Financial Returns

The financial returns are only part of the picture. Research consistently shows that working with an advisor also produces measurable non-financial outcomes:

- Greater confidence in long-term financial decisions

- Lower financial stress, particularly around market volatility and income gaps

- Clearer planning direction, with documented goals and tested withdrawal strategies

For clients navigating this stage, Sentinel Asset Management brings 100+ years of combined advisory experience and a track record of guiding 2,000+ clients through retirement — providing the technical depth and continuity that complex retirement income plans require.

Frequently Asked Questions

Frequently Asked Questions

Is it worth getting a financial advisor for retirement?

Yes, particularly because the distribution phase is more complex than accumulation. Coordinating income sources, managing taxes, and avoiding sequence-of-returns risk are areas where professional guidance typically delivers concrete, quantifiable value — through tax savings, optimized Social Security timing, and withdrawal sequencing — that offsets advisory fees.

How do I increase my retirement income?

Optimize Social Security claiming age, execute Roth conversions before RMDs begin, use tax-efficient withdrawal sequencing across account types, and ensure your portfolio is structured to generate income without excessive selling during downturns.

What does a retirement income advisor do differently than a general financial advisor?

A retirement income specialist focuses on the distribution phase: building a plan to generate reliable cash flow from existing assets, rather than primarily on portfolio growth. This requires different strategies around withdrawal sequencing, tax management, Social Security optimization, and longevity planning.

When should I start working with a financial advisor before retirement?

Ideally 5-10 years before retirement, as this window allows time for Roth conversions, tax-bracket management, and strategic portfolio repositioning. That said, starting later still matters. Retirees already drawing income can benefit from restructured withdrawal sequencing and ongoing tax management.

How do I know if a financial advisor is a fiduciary?

A fiduciary is legally required to act in your best interest rather than their own. Ask any advisor to confirm their fiduciary status in writing. You can verify credentials and disciplinary history for free through FINRA's BrokerCheck or the SEC's Investment Adviser Public Disclosure database.

What is the biggest mistake people make with retirement income planning?

Treating retirement accounts as a savings balance rather than an income system. Withdrawing without a sequencing strategy, ignoring tax implications, and failing to plan for longevity can turn a healthy nest egg into an income shortfall within 15-20 years.

Take the next step in your financial journey by exploring our courses page for upcoming live seminars.