General information, not personalised tax, legal or investment advice.

Introduction

For most families, retirement savings compete with college tuition, mortgage payoffs, aging parent support, and—for some—caring for dependents with special needs. 54% of Americans in their 40s are simultaneously raising children and supporting aging parents. That dual pressure causes 59% to reduce or stop retirement contributions entirely.

The deeper challenge is that life rarely holds still. Job transitions, inheritances, divorces, and new dependents can upend even a well-structured plan. What works for a dual-income household in Connecticut won't work for a single-parent family supporting a special needs child in Maryland.

This article breaks down what retirement planning for families actually looks like—how to set specific goals, build a step-by-step plan, manage competing priorities, and work with the right services to create a strategy that evolves as your life does.

Key takeaways

- Family retirement planning means juggling education costs, parental support, and 25-30 years of income—simultaneously

- Your plan should be built around your income needs, tax situation, risk tolerance, and family structure—not a generic template

- A 65-year-old couple has a 47% probability that one spouse will live to age 90, requiring 25-30 years of income planning

- 59% of sandwich generation families have reduced retirement savings due to supporting both children and parents

- A fiduciary advisor coordinates your investments, taxes, and estate plan so your wealth reaches the people who matter most

Why Family Retirement Planning Is Different

Retirement planning for a single person is hard enough. Add a spouse, children, aging parents, and shared debt, and the complexity multiplies fast. Family retirement planning requires coordinating overlapping income timelines and financial dependencies that can shift your target retirement date by years.

The Sandwich Generation Reality

The "sandwich generation" describes adults simultaneously saving for retirement, funding children's education, and supporting aging parents. 54% of Americans in their 40s are in this position, according to Pew Research. The financial cost is steep: an Allianz Life study found that 59% of this group have reduced or stopped retirement contributions because of competing demands.

That pressure is real — and it illustrates why a one-size approach to family retirement planning breaks down.

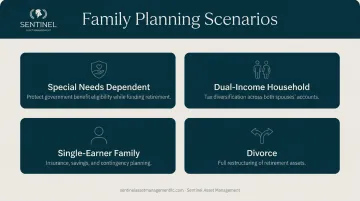

Family-Specific Circumstances Require Distinct Approaches

A dependent with special needs, a divorce, a dual-income household, or a single-earner family—each requires a distinct planning approach, not a template. For example:

- Raising a child with special needs means structuring assets to protect government benefit eligibility — while still funding your own retirement

- In dual-income households, tax diversification across both spouses' accounts requires active coordination, not just parallel saving

- Single-earner families carry more risk on one income stream, which changes how insurance, savings, and contingency planning are built

- Divorce triggers a full restructuring of retirement assets and often requires reassessing when and how retirement is even possible

Sentinel Asset Management has worked with families navigating each of these situations — including 25 years of experience supporting families with special needs dependents and more than 2,000 clients guided through retirement planning.

Common Family Financial Goals for Retirement

Family financial goals are the specific, measurable targets that shape how much to save, when to retire, and how income should be distributed across the household. These goals fall into two categories: short-term (paying off debt, building an emergency fund) and long-term (retirement income, legacy planning).

Concrete Examples of Family Financial Goals

Replacing 70-80% of pre-retirement household income to maintain living standards. Most people need to replace between 55-80% of pre-tax income, though the exact percentage depends on income level and fixed expenses.

Funding children's college education without drawing from retirement accounts. 529 plans remain the most tax-advantaged vehicle, with average balances reaching $30,961. SECURE 2.0 now allows up to $35,000 in lifetime 529-to-Roth IRA rollovers.

Ensuring long-term support for a special needs dependent through Special Needs Trusts or ABLE accounts. ABLE accounts allow up to $100,000 in savings without triggering SSI suspension.

Paying off the mortgage before retirement to reduce fixed monthly obligations and create more financial flexibility.

Building a legacy fund or estate plan so wealth transfers efficiently to the next generation while minimizing taxes and probate complications.

How to Prioritize Competing Goals

With five or more goals competing for the same dollars, ranking them is not optional — it's where the real planning begins. A useful starting framework:

- Retirement funding first: Unlike education, retirement cannot be financed. There are no loans for it.

- Time-sensitive goals second: College funding has a hard deadline; a mortgage payoff does not.

- Legacy and estate goals last: These matter, but they're built on the foundation the first two create.

Put Numbers to Your Goals

Vague goals like "save more" don't give you anything to plan around. Families should define:

- Target retirement income (monthly or annual)

- Target retirement date

- Estimated expense categories (healthcare, housing, travel)

- Funding targets for each dependent or obligation

What a family needs at 40 looks very different at 55 — job transitions, inheritances, medical costs, and shifting dependent needs all change the numbers. Build in a review at least every three to five years.

How to Build a Personalized Family Retirement Plan

Step 1 — Assess Your Full Financial Picture

Before setting a retirement target, families need a complete view of:

- Assets: Retirement accounts (401(k), IRA), brokerage accounts, real estate, business equity

- Liabilities: Mortgage, student loans, caregiving costs, medical debt

- Monthly cash flow: Income sources, fixed expenses, discretionary spending

This baseline matters because it sizes the retirement income gap—the difference between what you'll have and what you'll need. Closing that gap starts with knowing exactly where you stand today.

Step 2 — Define Your Household Retirement Income Target

Estimate retirement income needs by considering:

- Projected expenses (housing, healthcare, lifestyle)

- Anticipated Social Security benefits

- Any pension or annuity income

The "$1,000/month rule" (explained in FAQ) offers a simplified benchmark, but most families need a more tailored calculation that accounts for dependent support, variable healthcare costs, and longevity risk.

Step 3 — Choose the Right Account Mix

The main retirement savings vehicles families should consider:

- 401(k)/403(b) plans: Employer-sponsored, pre-tax or Roth options

- Traditional IRAs: Tax-deferred growth, taxed at withdrawal

- Roth IRAs: After-tax contributions, tax-free growth and withdrawals

- Taxable brokerage accounts: Flexible access, no contribution limits

The mix should reflect your current and expected future tax bracket, time horizon, and liquidity needs. Sentinel coordinates assets across taxable, tax-deferred, and tax-free accounts—using strategies like Roth conversions and withdrawal sequencing—to reduce what families pay in taxes over a lifetime.

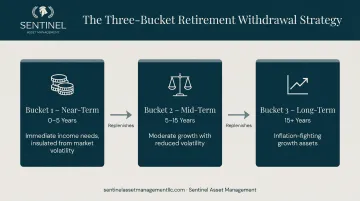

Step 4 — Build a Withdrawal Strategy

How you draw down assets in retirement is as important as how you accumulate them. Structured withdrawal "buckets" segment assets by time horizon:

- Near-term bucket (0-5 years): Cash and stable investments for immediate income needs, insulated from market volatility

- Mid-term bucket (5-15 years): Balanced allocation providing moderate growth with reduced volatility

- Long-term bucket (15+ years): Growth-oriented assets to preserve purchasing power and combat inflation

This approach reduces vulnerability to market downturns during early retirement years and ensures you don't have to sell stocks at a loss to fund living expenses.

Step 5 — Incorporate an Investment Policy Statement and Stress Testing

Every family retirement plan should be anchored by a documented Investment Policy Statement (IPS) that outlines:

- Specific financial goals and retirement income targets

- Risk tolerance and time horizon

- Asset allocation targets and rebalancing guidelines

- Withdrawal strategy and decision-making framework

Stress-testing the plan against scenarios like inflation spikes, prolonged bear markets, and interest rate shifts exposes weaknesses before they become crises—while the plan can still be adjusted.

Sentinel's PRIME risk framework addresses five systematic risks: Purchasing Power, Reinvestment, Interest Rate, Market, and Exchange Risk. Running a plan through this lens often surfaces concentration risks or sequence-of-returns vulnerabilities that standard projections miss.

Managing Competing Financial Priorities as a Family

Retirement vs. Education Funding

Financial advisors consistently advise prioritizing retirement savings over college funding. Retirement cannot be borrowed for, while education costs have alternatives: loans, scholarships, work-study programs, and community college transfers.

529 plans remain the most tax-advantaged vehicle for education savings and can run parallel to retirement contributions if budgeted correctly. With SECURE 2.0, families can now roll over up to $35,000 in unused 529 funds into a Roth IRA, transforming education savings into a retirement jumpstart.

The Aging Parent Challenge

Supporting aging parents financially can significantly disrupt your retirement trajectory if unplanned. Families should assess early:

- Parents' income sources (Social Security, pension, savings)

- Long-term care insurance status

- Potential out-of-pocket medical costs

According to the 2025 Genworth Cost of Care Survey, the national median cost for a nursing home semi-private room is $114,975 annually, while home health aides average $80,080 annually. Starting this assessment a decade before care is needed gives families time to fund it without drawing down their own retirement assets.

Planning for Families with Special Needs Dependents

Families caring for a dependent with a disability face unique retirement planning considerations. They must plan for their own retirement while ensuring the dependent's long-term financial security does not conflict with government benefit eligibility.

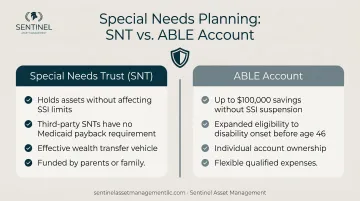

Two planning tools address this directly:

- Special Needs Trusts (SNTs) hold assets for a disabled individual without counting toward SSI resource limits. Third-party SNTs — funded by parents — carry no Medicaid payback requirement, making them effective wealth transfer vehicles.

- ABLE accounts allow up to $100,000 in savings without triggering SSI suspension. The 2026 ABLE Age Adjustment Act expands eligibility to individuals whose disability began before age 46.

Families with special needs dependents should work with advisors who have deep, specialized experience. Sentinel has 25 years of dedicated experience supporting such families, coordinating with attorneys and care planners to ensure financial strategies align with legal structures and government benefit protection.

Estate Planning as a Unifying Layer

Each of these priorities — education funding, aging parent care, special needs planning — ultimately connects to the same question: where do assets go, and who controls them? Estate planning provides that answer. Wills, trusts, beneficiary designations, and powers of attorney ensure assets reach the right people under any circumstance, including death or incapacity.

Sentinel handles estate planning coordination—beneficiary designations, account titling, and ownership structures—directly, bringing in estate attorneys only when complex instruments like irrevocable trusts or SNTs require formal legal drafting.

Key Retirement Planning Services Families Should Leverage

Core Advisory Services

The services that make the most difference for families include:

- Investment management with tax-efficient, diversified portfolios built on modern portfolio theory

- Retirement income planning including Social Security timing and withdrawal sequencing

- Estate planning support coordinating beneficiary designations, trusts, and wealth transfer strategies

When these services operate under one advisory relationship, strategy stays consistent and nothing falls through the cracks between tax planning, investments, and estate decisions.

Personalized Allocation in Practice

A retirement portfolio should be built around your family's investment goals, income needs, tax situation, and risk tolerance—not a generic model. Every portfolio should be guided by an Investment Policy Statement that holds the strategy accountable over time.

Sentinel creates tailored portfolios stress-tested under different market conditions and monitored continuously for style drift and opportunity—so the strategy stays grounded in your family's actual priorities, not last year's assumptions.

Ongoing Plan Reviews

Retirement plans need to keep pace with your life. Major changes that typically require a plan update include:

- Job loss or a significant income shift

- An inheritance or unexpected windfall

- Divorce or remarriage

- Adding a dependent, including a child or aging parent

Families should establish a review cadence with their advisor, at minimum annually, to ensure the plan still reflects current goals and risk capacity.

A structured annual review—more frequent during transitions—is what separates a plan that holds up from one that gets abandoned at the worst possible moment.

Common Mistakes Families Make in Retirement Planning

Underestimating Healthcare and Longevity Costs

Many families plan for retirement as though it will last 15-20 years. A 65-year-old couple, though, has a 46.7% probability that at least one spouse will survive to age 90.

A healthy couple retiring in 2026 faces projected lifetime healthcare costs of $955,411 when including premiums, deductibles, and out-of-pocket expenses — and that doesn't include long-term care. Healthcare costs also tend to rise faster than general inflation, compounding the gap between what families save and what they'll actually need.

Planning for a 30-year retirement rather than 20 changes the math significantly — on withdrawal rates, investment risk, and how aggressively you need to grow and protect assets.

Ignoring Sequence-of-Returns Risk

Retiring into a down market is one of the most damaging scenarios a family can face. Withdrawing from a shrinking portfolio locks in losses and permanently reduces the capital available for future recovery — a dynamic called sequence-of-returns risk.

A couple who retired in January 2000 and withdrew 5% annually would have depleted their portfolio by 2012, even though the market eventually recovered. Timing matters as much as average returns.

Strategies like structured withdrawal buckets — separating near-term cash needs from long-term growth assets — can help insulate spending from short-term volatility.

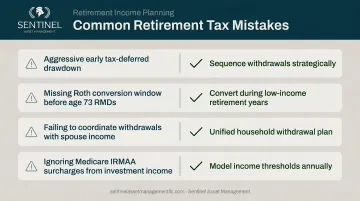

Overlooking Tax Drag and Withdrawal Strategy

Most retirement savers focus on accumulation. Far fewer think carefully about how taxes will erode withdrawals. Pulling exclusively from tax-deferred accounts like traditional IRAs or 401(k)s can push retirees into higher brackets, increase Medicare premiums, and trigger Social Security taxation.

A coordinated withdrawal strategy — drawing from taxable, tax-deferred, and tax-free accounts in a deliberate sequence — can meaningfully reduce lifetime tax liability.

Common tax mistakes include:

- Drawing down tax-deferred accounts too aggressively in early retirement

- Missing Roth conversion windows between retirement and age 73 (when RMDs begin)

- Failing to coordinate withdrawals with a spouse's income or part-time earnings

- Ignoring the impact of investment income on Medicare IRMAA surcharges

Treating Estate Planning as Optional

Many families delay estate planning until health declines or a crisis forces the issue. By then, options narrow. Beneficiary designations may contradict a current will. Assets may pass outside the estate plan entirely — directly to an ex-spouse or a minor child without a guardian named.

A retirement plan without an estate component isn't complete. Decisions about power of attorney, healthcare directives, and account titling should be revisited every few years — not set once and forgotten.

Take the next step in your financial journey by exploring our courses page for upcoming live seminars.