General information, not personalised tax, legal or investment advice.

Introduction

Many families face a false choice: take care of loved ones or give back to causes they care about. In reality, charitable legacy planning isn't a compromise—it's a bridge that honors both commitments. When structured thoughtfully, your estate can provide for your heirs and leave a lasting mark on the organizations and communities that shaped your values.

Yet a significant gap exists between intention and action. While 38% of high-net-worth donors plan to leave money to charity, only 5.7% of Americans actually include a charity in their will. That gap represents billions in unrealized impact—and for most families, it comes down to not knowing where or how to start.

If you've thought about leaving something meaningful behind but haven't acted on it yet, this guide is the practical starting point. You'll learn how to define your charitable goals, choose the right giving vehicle for your situation, unlock tax advantages that benefit both your heirs and your chosen causes, and work with the right advisors to put your plan in motion.

Key takeaways

- Legacy planning for charitable giving formalizes donations to causes you care about within your estate plan—not one-time gifts, but a structured, lasting commitment

- Key vehicles include bequests, beneficiary designations on retirement accounts, charitable trusts (CRTs/CLTs), donor-advised funds (DAFs), and qualified charitable distributions (QCDs)

- Strategic charitable giving reduces estate taxes, avoids capital gains, and increases what flows to both heirs and charities simultaneously

- Working with a financial advisor ensures your charitable legacy is tax-efficient, legally sound, and woven into your broader financial picture

Defining Your Charitable Goals and Values

Understanding Planned Giving vs. Legacy Giving

Planned giving refers to any structured, future-oriented donation mechanism—bequests, trusts, QCDs, beneficiary designations, or gifts made through your estate plan. Legacy giving is the intention behind those gifts: the lasting philanthropic impact you'll be remembered for. Planned giving is the tool; legacy giving is the purpose. The terms are often used interchangeably, but understanding the distinction helps you match the right strategy to your goals.

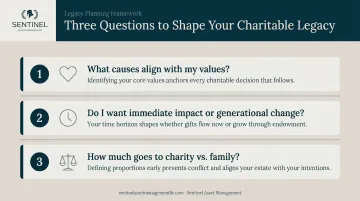

Three Questions to Anchor Your Giving

Before selecting a vehicle, clarify what you want your charitable legacy to accomplish:

- What causes align with my values? Identify the organizations, missions, or communities that reflect your beliefs and priorities.

- Do I want immediate impact or generational change? Some gifts fund current programs; others build endowments that sustain work for decades.

- How much of my estate goes to charity versus family? This isn't always an either/or decision—many plans balance both—but clarity on percentages guides vehicle selection.

Practical first step: Draft a brief personal charitable mission statement. A single paragraph clarifying why you give, what you hope to achieve, and who benefits creates a filter for every decision that follows.

Vetting Charities Before You Commit

With your goals in place, the next step is confirming that your chosen organizations can actually deliver on them. Due diligence protects both your intentions and your tax benefits:

- Verify 501(c)(3) status using the IRS Tax Exempt Organization Search

- Review Form 990 filings for financial transparency via the ProPublica Nonprofit Explorer

- Check independent ratings at Charity Navigator or the BBB Wise Giving Alliance

A charity that dissolves, merges, or mismanages funds can quietly derail a well-constructed legacy plan. Spending 30 minutes on verification now prevents years of misdirected giving later.

Charitable Giving Vehicles: Which Strategy Fits Your Plan?

No single vehicle works for everyone. The best choice depends on estate size, tax situation, income needs, and how much control and flexibility you want. Each tool below serves a different donor profile.

Bequests and Beneficiary Designations

Bequests are the simplest entry point: a gift written into your will or trust that takes effect at death. They're fully revocable during your lifetime and deductible from your taxable estate.

Naming a charity as primary, contingent, or partial beneficiary on an IRA or 401(k) is often the most tax-efficient bequest strategy. Why? Charities don't pay income tax on retirement account withdrawals. Individual heirs, by contrast, face ordinary income tax on inherited IRA distributions— potentially at rates up to 37%.

Best for: Donors who want simplicity, revocability, and tax efficiency without lifetime commitment.

Donor-Advised Funds (DAFs)

A DAF is a charitable giving account held at a sponsoring organization. You contribute assets (cash, securities, or other property), receive an immediate tax deduction, and recommend grants to qualified charities over time at your own pace.

Key advantages:

- Once contributed, funds are permanently committed to charitable use — though grant timing and recipient selection remain fully flexible

- Funds can be invested and grow tax-free inside the DAF

- Eliminates administrative burden of a private foundation

- Strong option for high-income years or when you want flexibility about which charities to support

DAFs held $326.45 billion in assets and distributed $64.89 billion in 2024, with a payout rate of 25.3%.

Best for: Donors who want immediate tax deductions, investment growth, and multi-year grant flexibility without the overhead of a foundation.

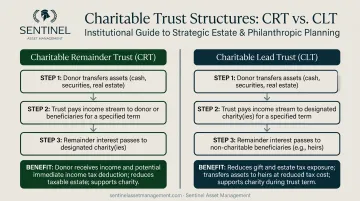

Charitable Remainder Trusts (CRTs) and Charitable Lead Trusts (CLTs)

Charitable Remainder Trusts (CRTs): You transfer appreciated assets into an irrevocable trust. The trust pays income to you or named beneficiaries for life or a set term (up to 20 years). The remainder passes to charity.

Benefits include a partial income tax deduction upfront and avoidance of immediate capital gains on donated appreciated assets. Under IRS rules, CRTs must distribute between 5% and 50% annually, and the charitable remainder must be at least 10% of the initial trust value.

Charitable Lead Trusts (CLTs): CLTs flip the structure: charity receives income first, and the remainder passes to heirs. This makes them useful for wealth transfer when philanthropic giving is the near-term priority. They also reduce estate or gift taxes while keeping assets on track for family.

Best for: Donors with highly appreciated assets, significant estates, and income needs who want to combine lifetime income with charitable impact and estate tax reduction.

Qualified Charitable Distributions (QCDs)

Donors aged 70½ or older can transfer funds directly from an IRA to a qualified charity. This counts toward your Required Minimum Distribution (RMD) but is excluded from taxable income.

The annual QCD limit is $111,000 per individual for 2026, indexed for inflation.

Why it's powerful: Retirees who don't need full RMD income can satisfy distribution requirements, support charities, and avoid the tax hit of a large taxable withdrawal — all in one move.

This approach suits retirees managing RMDs who want tax-efficient charitable giving without increasing adjusted gross income.

For donors who want to go further — building a philanthropic structure that outlasts them — private foundations offer the deepest level of control and legacy impact.

Private Foundations

A private foundation is your own charitable entity that can make grants, employ family members, and operate programs. It offers maximum legacy-building potential and control.

Trade-offs:

- Significant administrative, compliance, and cost requirements

- IRS filings, excise taxes (1.39% on net investment income), and minimum 5% annual distribution rules

- Most appropriate for very large estates

Best for: Ultra-high-net-worth families who want multi-generational philanthropic infrastructure and are prepared for ongoing operational complexity. For most donors, DAFs offer lower-complexity alternatives with similar flexibility.

Tax Benefits of Charitable Legacy Planning

Strategic charitable giving reduces estate taxes, income taxes, and capital gains taxes simultaneously — structured well, it increases what reaches both your family and the causes you care about.

Estate Tax Deductions

Assets left to qualified 501(c)(3) organizations are fully excluded from your taxable estate under IRC §2055. For 2026, the federal estate tax exemption is $15,000,000 per individual. Estates near or above this threshold benefit most from charitable deductions, which can meaningfully reduce or eliminate estate tax liability.

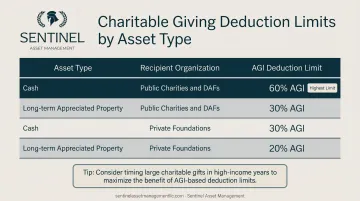

Beyond estate planning, charitable gifts made during your lifetime can also reduce your current tax bill. Deductions are capped as a percentage of your adjusted gross income (AGI), with limits varying by asset type and recipient organization:

Income Tax Deductions for Lifetime Gifts

| Asset Type | Recipient Organization | AGI Deduction Limit |

|---|---|---|

| Cash | Public charities & DAFs | 60% of AGI |

| Long-term appreciated property | Public charities & DAFs | 30% of AGI (fair market value) |

| Cash | Private foundations | 30% of AGI |

| Long-term appreciated property | Private foundations | 20% of AGI |

Timing tip: Larger donations made in high-income years — such as the year of a business sale or large bonus — generate the most deduction value. Coordinating gift timing with your overall tax picture is where legacy planning and tax management intersect most powerfully.

Take the next step in your financial journey by exploring our courses page for upcoming live seminars.