General information, not personalised tax, legal or investment advice.

Introduction

Most investors focus intensely on what to invest in—stocks, bonds, or funds—but rarely stop to consider where those investments are held. That oversight steadily erodes wealth through avoidable taxes every single year. Research from Vanguard shows that investors who default to "equal-location" strategies—spreading the same asset mix across all account types—consistently underperform optimized asset location by 5 to 30 basis points annually.

Over a 20- or 30-year retirement horizon, that seemingly small gap compounds into tens or even hundreds of thousands of dollars in lost wealth.

Asset location addresses this directly. It's the strategy of matching specific investments to the account types—taxable, tax-deferred, or tax-exempt—where they face the least tax friction. For retirement-focused investors, getting this right can be one of the most impactful and underused levers available.

Key takeaways

- Asset location strategically places investments across taxable, tax-deferred, and tax-exempt accounts to maximize after-tax returns

- Tax-inefficient assets (bonds, REITs, actively managed funds) belong in tax-advantaged accounts

- Tax-efficient assets (index funds, municipal bonds, long-term stock holdings) belong in taxable accounts

- Research indicates this strategy can improve after-tax returns by 5 to 30 basis points annually—higher-income investors benefit the most

- Ongoing management is required as tax laws shift and account balances evolve

- Working with a financial advisor ensures this strategy is applied and maintained correctly

What Is Asset Location (and How It Differs from Asset Allocation)

Asset allocation determines how much of a portfolio goes into different asset classes—stocks, bonds, cash. Asset location determines which account type each of those assets should live in. They're two separate decisions, yet many investors treat them as one — and that conflation has real tax consequences.

Consider a simple example: placing tax-exempt municipal bonds inside a Traditional IRA defeats their purpose. Municipal bonds generate federally tax-exempt interest, but when held in a Traditional IRA, that income becomes taxable upon withdrawal—erasing the bond's primary benefit.

Done well, asset location minimizes lifetime tax liability and preserves more compounding power across the portfolio. At Sentinel Asset Management, every client portfolio is guided by an Investment Policy Statement that accounts for tax situation, income needs, and long-term goals. Asset location isn't a one-time setup — it's an ongoing component of a coordinated financial plan.

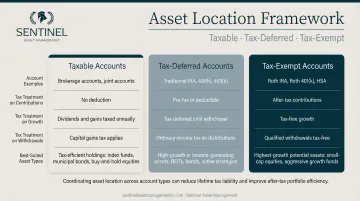

The Three Account Types and Where Each Asset Belongs

Taxable Accounts (Brokerage Accounts)

Taxable accounts tax interest and dividend income in the year it's earned, and capital gains upon sale. That makes them the right home for assets that rarely trigger taxable events.

Assets that belong here:

- Municipal bonds – Interest is generally federally tax-exempt

- Index funds and ETFs – Structured to minimize capital gains distributions through in-kind redemptions, where shares are exchanged rather than sold

- Individual stocks held long-term – Qualify for lower long-term capital gains rates and receive a step-up in cost basis upon the owner's death

Tax-Deferred Accounts (Traditional IRA, Traditional 401(k))

These accounts allow investments to grow without annual taxation, but withdrawals are taxed at ordinary income rates. Assets that throw off frequent income belong here, where that income won't trigger an annual tax bill while it grows.

Assets that belong here:

- Taxable bonds and bond funds – Interest is taxed as ordinary income annually in a taxable account

- REITs – Required by law to distribute at least 90% of taxable income as dividends

- Actively managed mutual funds – High portfolio turnover generates taxable capital gains distributions

- High-dividend stocks – Regular dividend income would otherwise trigger annual tax bills

Tax-Exempt Accounts (Roth IRA, Roth 401(k))

Roth accounts are funded with after-tax dollars, but qualified withdrawals—including all growth—are entirely tax-free. This makes them ideal for assets with the highest expected appreciation.

Assets that belong here:

- High-growth equities – All gains compound and exit the account tax-free

- Actively managed equity funds – Every dollar of gain leaves the account untaxed, so these accounts deliver maximum advantage when holding assets positioned for strong growth

Key Advantages of Strategic Asset Location

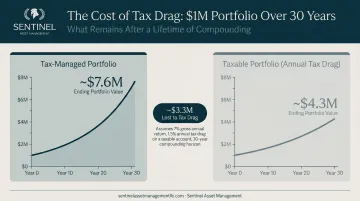

Advantage 1: Eliminating Annual Tax Drag on Investment Returns

Tax drag occurs when income-generating or high-turnover assets sit in a taxable account. The taxes owed each year reduce the amount available to reinvest, eroding compounding returns.

Sheltering tax-inefficient assets in a tax-deferred account removes this drag entirely during the accumulation phase. Interest and capital gains distributions compound without annual taxation until withdrawal.

Why this matters: Research from Research Affiliates found that moving from 0% to just 10% annual portfolio turnover reduces terminal wealth by nearly 20% over 20 years due to realized taxable gains. Eliminating a 1.0% annual tax drag on a $1,000,000 portfolio compounding at 6.0% over 30 years preserves an additional $1.42 million in wealth.

Who benefits most:

- Investors with significant bond allocations

- Those in the 24% federal income tax bracket and above

- Anyone holding actively managed mutual funds with high turnover in a taxable brokerage account

Advantage 2: Maximizing After-Tax Wealth by Choosing the Right Account

The same asset growing at the same rate produces a different after-tax outcome depending on which account it lives in. Placing high-appreciation assets in Roth accounts allows 100% of the growth to be harvested tax-free.

Comparison example:

Assume a $250,000 investment in a taxable bond fund yielding 6% annually over 20 years. Holding this in a Roth IRA instead of a taxable brokerage account (with a 35.8% marginal tax rate) results in nearly $290,000 more in after-tax terminal wealth.

By contrast, a Traditional IRA taxes every dollar withdrawn at ordinary income rates — and a taxable account captures gains only at capital gains rates, leaving decades of compounding growth exposed. The gap between these outcomes grows meaningfully over a 20- to 30-year horizon, turning account selection into one of the most consequential tax decisions in a long-term plan. Strategic placement also creates tax diversification across account types, which gives you flexibility in how you draw retirement income.

Who benefits most:

- Investors approaching retirement who hold both Roth and traditional accounts

- Younger investors using Roth conversions during lower-income years to shift assets from tax-deferred to tax-exempt status

Advantage 3: Estate Planning and the Step-Up in Basis

When appreciated assets held in a taxable brokerage account pass to heirs, the cost basis resets to fair market value at the time of death. This effectively eliminates the embedded capital gains tax that would otherwise apply to decades of growth.

Example:

A stock purchased for $100,000 grows to $600,000 by the time of death. If held in a taxable account, heirs owe nothing on the $500,000 gain due to the step-up. If held in a Traditional IRA, heirs owe ordinary income tax on every dollar withdrawn, and under SECURE 2.0, they must liquidate the entire account within 10 years.

Why this matters for legacy planning: The step-up in basis is one of the most valuable — and most overlooked — tools in estate planning. For families who want appreciated assets to transfer cleanly to the next generation, holding those positions in a taxable account rather than a Traditional IRA can save heirs from a significant tax bill. Sentinel Asset Management incorporates this consideration directly into portfolio construction, so asset location decisions made today don't create unintended tax consequences for your heirs tomorrow.

Who benefits most:

- Investors who plan to leave assets to heirs rather than spend them in retirement

- Those with low-cost-basis positions that have appreciated significantly over time

What Happens Without an Asset Location Strategy

The most common default behavior is applying the same asset allocation across all account types—known as "equal location." This feels simple and intuitive but creates consistent, avoidable tax drag.

Real-world consequences:

- Bonds and REITs generating fully taxable interest income inside a brokerage account each year

- Actively managed funds distributing large capital gains in taxable accounts

- High-growth assets compounding inside accounts that will eventually be taxed at ordinary income rates

- Tax-advantaged space going underutilized

The quantifiable cost: Vanguard's research confirms that equal-location strategies consistently underperform optimized asset location by 5 to 30 basis points annually. On a $500,000 portfolio, that 20-year gap can quietly erode $25,000 or more—money that never had to leave in the first place.

How to Get the Most from Asset Location

Asset location works best when implemented from the start of a portfolio's design. However, most investors inherit portfolios that are already mislocated. A course correction is possible without triggering a major tax event.

Key tools for realignment:

- Tax-loss harvesting – Sell taxable assets at a loss to offset gains while freeing up cash for reallocation

- Redirect dividends and interest – Stop automatic reinvestment and deploy distributions into more tax-efficient assets

- Use tax-advantaged accounts to rebalance – Sell or reposition mislocated assets inside IRAs without triggering taxable events in the brokerage account

Adapt as Your Tax Picture Changes

What works at 45 may not work at 65. As Required Minimum Distributions (RMDs) from Traditional IRAs begin, they can push taxable income into a higher bracket and shift which assets belong where. The RMD age is now 73 for those born between 1951 and 1958, rising to 75 by 2033.

Why Personalization Matters

Asset location isn't a formula — the right structure depends on:

- Current and projected tax bracket

- Relative size of each account type

- Planned withdrawal sequencing in retirement

- Estate planning goals

Sentinel Asset Management builds tax-efficient portfolios guided by an Investment Policy Statement that accounts for each client's tax situation, income needs, and long-term goals. Asset location is treated as an ongoing part of a coordinated financial plan, reviewed and adjusted as life circumstances evolve.

Frequently Asked Questions

Is asset location worth it?

For investors in higher tax brackets with both taxable and tax-advantaged accounts, the strategy can meaningfully improve after-tax returns. Research suggests annual gains of 5 to 30 basis points, which compound significantly over a multi-decade retirement horizon.

How can asset location reduce taxes?

By placing tax-inefficient, income-generating assets in tax-deferred accounts and tax-efficient, low-turnover assets in taxable accounts, investors reduce the number of taxable events each year. This allows more of the portfolio to compound without interruption.

What are tax-efficient assets?

Common examples include index funds and ETFs (which rarely distribute capital gains), municipal bonds (whose interest is generally tax-exempt), and individual stocks held long-term for preferential capital gains rates and a step-up in basis at death.

Where to park money for taxes?

Income-producing, tax-inefficient assets (bonds, REITs, active mutual funds) belong in a Traditional IRA or 401(k). High-growth assets belong in a Roth account. Tax-efficient, long-term assets belong in a taxable brokerage account.

What is the difference between asset location and asset allocation?

Asset allocation decides how a portfolio is divided among stocks, bonds, and other asset classes to balance risk and return. Asset location is a separate decision about which account type—taxable, tax-deferred, or tax-exempt—each investment should occupy to minimize taxes.

Should I put bonds in my IRA or taxable account?

Taxable bonds generally belong in a Traditional IRA or 401(k), where their interest income is sheltered from annual taxation. Municipal bonds, however, are better suited for taxable accounts, where their tax-exempt interest retains its advantage—placing munis in a tax-deferred account removes this benefit entirely.

Take the next step in your financial journey by exploring our courses page for upcoming live seminars.