General information, not personalised tax, legal or investment advice.

Introduction

Picture this: you've worked for decades, lived carefully, and built a retirement account that finally crossed six figures. You feel relief, maybe pride. But then a different question arrives, quieter and more urgent than the others: Now what?

Saving was the easy part. The real challenge is making that money work for you, keep growing, and last a lifetime. Asset management is the disciplined process that turns accumulated savings into a structured plan designed to endure — one built around your goals, your timeline, and the risks you can't afford to ignore. This guide covers what asset management actually means, how the process works, and the best practices that separate sound wealth management from guesswork.

Key takeaways:

- Asset management is the professional practice of investing and overseeing financial assets to grow wealth while managing risk

- Professional managers act as fiduciaries, legally obligated to put client interests first

- Portfolios blend equities, bonds, cash, and alternatives based on goals and timeline

- The process follows a structured path: planning, allocation, implementation, monitoring, and rebalancing

- Best practices include Investment Policy Statements, diversification, tax coordination, and scheduled portfolio reviews

What Is Asset Management?

Asset management is the professional practice of investing and overseeing a client's financial assets—stocks, bonds, real estate, and cash equivalents—with two primary goals: growing wealth over time while managing risk within the client's tolerance. It's fundamentally different from simply saving money in a bank account or making occasional trades in a brokerage app.

Professional asset managers build comprehensive, ongoing strategies rather than one-off transactions. According to the 2025 Investment Adviser Industry Snapshot, 15,870 SEC-registered investment advisers now manage $144.6 trillion for 68.4 million clients, reflecting massive growth in professional wealth management.

Fiduciary Duty vs. Broker-Dealer Standards

What separates asset managers from brokers or salespeople is their fiduciary duty. Under the Investment Advisers Act of 1940, investment advisers must act in their clients' best interests at all times, upholding both a duty of care and a duty of loyalty. This legal obligation requires ongoing portfolio monitoring and transparent communication.

Broker-dealers operate under a different standard. Regulation Best Interest (Reg BI) only requires acting in the client's best interest at the time a recommendation is made — no ongoing duty exists after that point.

That structural accountability shapes how asset managers actually invest on a client's behalf.

Active vs. Passive Management

Asset management approaches fall along a spectrum:

- Active management involves hands-on research, individual security selection, and frequent portfolio adjustments to outperform market benchmarks

- Passive management tracks market indices with minimal intervention, typically through low-cost index funds or ETFs

Most professional relationships blend both approaches, calibrated to the client's goals, risk tolerance, and fee sensitivity. Firms like Sentinel Asset Management use globally diversified portfolios rooted in modern portfolio theory, stress-tested across market conditions rather than optimized only for recent performance.

The 4 Main Types of Financial Assets

Diversification — spreading investments across assets that behave differently under market pressure — is how professional managers reduce risk without sacrificing long-term returns. That strategy starts with understanding the four core asset categories.

| Asset Class | Historical Annual Return (1926-2017) | Risk-Return Profile |

|---|---|---|

| Equities (Stocks) | 10.2% | Highest long-term growth; highest short-term volatility |

| Fixed Income (Bonds) | 5.5% | Steady income; moderate stability; sensitive to interest rate changes |

| Cash & Equivalents | 3.4% | Maximum safety and liquidity; lowest returns; vulnerable to inflation |

| Alternative Assets | Varies widely | Real estate, commodities, private equity; offers diversification but limited liquidity |

The Inflation Threat

Holding too much cash guarantees a loss of purchasing power over time. The Consumer Price Index rose from 130.7 in 1990 to 321.943 in 2025—meaning today's dollar buys less than half what it did 35 years ago. This erosion is why professional asset management balances safety with growth.

Why Diversification Matters

A well-managed portfolio balances all four categories based on your timeline, income needs, and risk tolerance. Nobel laureate Harry Markowitz demonstrated in 1990 that intelligent diversification can reduce unsystematic risk — the company-specific or sector-specific volatility that no investor needs to absorb — while accepting only the systematic risks that come with participating in markets at all.

What Does a Financial Asset Manager Do?

Asset managers perform five core functions that separate professional wealth management from self-directed investing.

Initial Client Assessment

Before any money moves, managers gather a complete financial picture:

- Current income and projected earnings

- Existing liabilities and debts

- Tax situation and filing status

- Investment timeline and retirement horizon

- Risk tolerance and emotional comfort with volatility

This profile becomes the foundation for every allocation decision that follows — specific to your life, not a standardized model.

Portfolio Construction

Using your profile, managers build diversified portfolios designed to meet stated objectives. Sentinel Asset Management, for example, creates custom allocations based on investment goals, income needs, tax situation, and risk tolerance—each portfolio guided by a formal Investment Policy Statement.

The approach builds on Harry Markowitz's Nobel Prize–winning work in Modern Portfolio Theory: by balancing expected returns against portfolio variance through deliberate diversification, unsystematic risk can be reduced or eliminated entirely.

Ongoing Monitoring and Rebalancing

Markets shift constantly. A portfolio properly allocated at inception will drift as different assets grow at different rates. Fidelity research demonstrates that portfolios rebalanced systematically experienced 16% less annualized volatility over 30 years compared to buy-and-hold portfolios.

Asset managers continuously monitor holdings and rebalance when allocations drift beyond acceptable thresholds, restoring the intended risk-return profile. That discipline is inseparable from risk management — because drift left unchecked is itself a risk.

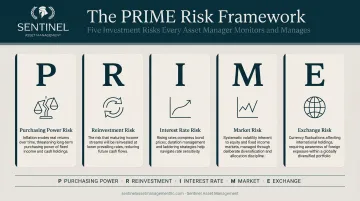

Risk Identification and Management

Professional managers identify and manage multiple risk layers:

- Purchasing power risk – inflation eroding your real returns over time

- Interest rate risk – rising rates decreasing the value of existing bonds

- Market risk – broad market volatility affecting overall portfolio value

- Reinvestment risk – falling rates reducing income when cash flows are reinvested

- Exchange rate risk – currency fluctuations affecting international holdings

Sentinel Asset Management frames these as the PRIME risks: the five systematic risks that cannot be diversified away but can be managed through proper asset allocation.

Client Communication and Reporting

Effective asset management includes regular reporting that covers what's happening in your portfolio, why decisions are being made, and how performance tracks against your goals. That ongoing dialogue keeps you grounded during volatile markets — and builds the kind of trust that makes a long-term relationship work.

How the Asset Management Process Works

Professional asset management follows a structured, repeatable process designed to keep decisions disciplined and aligned with your objectives.

Step 1: Define Goals and Establish an Investment Policy Statement

Before any investment decision, managers document your financial goals, risk parameters, income needs, tax situation, and constraints in a formal Investment Policy Statement (IPS). This document serves as your strategic roadmap and accountability anchor.

The IPS defines rebalancing triggers, acceptable asset classes, and performance benchmarks—creating objective criteria that prevent emotional, reactive decisions during market stress.

Step 2: Asset Allocation and Portfolio Construction

Using the IPS as the guide, managers allocate capital across asset classes to optimize expected returns for your acceptable risk level. This isn't one-size-fits-all—a 65-year-old retiree needing monthly income requires fundamentally different allocation than a 35-year-old in wealth accumulation mode.

Allocation decisions determine 80-90% of portfolio performance over time—which is why getting this right matters more than any individual security selection.

Step 3: Implementation and Diversification

Managers select specific securities, funds, or instruments within each asset class. From there, portfolios are stress-tested against scenarios like bull markets, recessions, and rising rate environments to confirm that allocations hold up under real-world pressure, not just recent conditions.

Sentinel Asset Management runs this process against historical bear markets and inflationary periods specifically, ensuring each portfolio can endure the disruptions clients are most likely to face.

Step 4: Ongoing Monitoring, Rebalancing, and Tax Management

Portfolios drift as assets grow at different rates, and left unattended, those drifts compound into real risk exposure. Vanguard research shows that threshold-based rebalancing—triggered when allocations drift by a set percentage—generates higher returns than calendar-based approaches because it reduces unnecessary transaction costs.

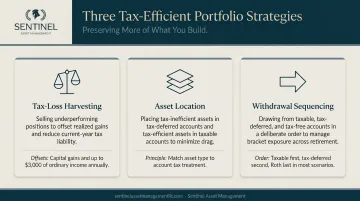

Tax-efficient strategies extend the value further:

- Tax-loss harvesting – selling securities below cost basis to offset gains; Vanguard finds this can add 0.47% to 1.27% in annual after-tax returns

- Asset location – placing tax-inefficient bonds in IRAs and tax-efficient equities in taxable accounts; adds 5 to 30 basis points annually

- Withdrawal sequencing – coordinating which accounts to draw from to minimize lifetime tax liability

Step 5: Performance Review and Plan Evolution

At regular intervals, managers review performance against benchmarks and your personal goals. Life changes—retirement, inheritance, divorce, caring for family members with special needs—may trigger full strategy reassessment.

What worked at 45 may need significant adjustment at 65, and a well-managed plan anticipates those shifts before they become problems.

Asset Management Best Practices

Professional asset management relies on proven principles that separate disciplined wealth-building from speculation.

Anchor Every Decision to a Written Plan

The most effective relationships are governed by documented Investment Policy Statements, not market headlines. This written discipline ensures decisions remain consistent, clear, and aligned with actual goals rather than reactive to short-term noise.

Build Globally Diversified, Tax-Efficient Portfolios

Diversification across geographies, sectors, and asset classes reduces volatility without sacrificing expected returns. Sentinel Asset Management applies this through globally diversified model portfolios stress-tested across market environments—not just optimized for recent history.

Tax efficiency compounds over decades. Strategic asset location and tax-loss harvesting can add meaningful after-tax returns without taking additional investment risk.

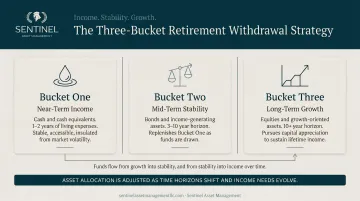

Use Structured Withdrawal Strategies

For clients in or near retirement, bucket strategies segment assets by time horizon. Assets are divided across three horizons:

- Near-term (1-2 years): Held in stable instruments to cover immediate cash needs

- Mid-term (3-10 years): Invested in bonds to balance growth and stability

- Long-term (10+ years): Kept in growth-oriented investments to build wealth over time

This prevents forced selling during downturns. Research in the Journal of Financial Planning confirms that cash reserve strategies improve plan survival rates relative to systematic withdrawals without reserves.

Coordinate Investments, Taxes, and Estate Planning as One Ecosystem

Effective asset management integrates portfolio returns with tax minimization and estate planning as a single system. Decisions about which accounts hold which assets, and when to act, can add more to long-term outcomes than investment selection alone. Legacy planning and wealth transfer should be built into the strategy from the start — not addressed as an afterthought.

Review and Adapt as Life Circumstances Change

Life changes — and your strategy should too. Retirement transitions, divorce, caring for special needs family members, or receiving an inheritance can each shift what an appropriate portfolio looks like. Regular, structured reviews keep your plan aligned with where you actually are, not where you were when you started.

How to Choose the Right Asset Management Firm

Selecting an asset manager requires evaluating expertise, transparency, and alignment with your specific needs. Three criteria stand out as non-negotiable: fiduciary commitment, relevant experience, and fee clarity.

Look for Genuine Fiduciary Commitment

Confirm the firm is a registered investment adviser with a legal fiduciary obligation. Verify registration and disciplinary history using the SEC's Investment Adviser Public Disclosure database, then review Form ADV Part 2A, which details business practices, fees, conflicts of interest, and any disciplinary history.

Beyond registration, look for firms that plan around your goals—not generic product templates. Concrete signals of depth include:

- 100+ years of combined advisory experience across the team

- Proven track records across multiple market cycles (not just bull markets)

- Personalized Investment Policy Statements tailored to your income needs and risk profile

Assess Experience with Your Specific Situation

Retirement income planning, special needs financial planning, and divorce financial planning each require a different skill set. Seek firms with documented experience in your specific circumstances—not generalists who treat every client the same.

Sentinel Asset Management, for example, has guided 2,000+ clients into retirement with average plan horizons of 20+ years, and brings 25 years of experience working with families with special needs.

Evaluate Transparency and Fee Structure

Understand how the firm charges—percentage of assets under management, flat fee, or hourly rate. Clarify communication frequency and reporting standards. Before signing anything, confirm you'll receive regular performance reports in plain language and that advisors are reachable when life changes—not just at the annual review.

Review Morningstar's "Five Pillars" framework—Process, Performance, People, Parent, and Price—when evaluating any asset manager or fund.

Frequently Asked Questions

What is asset management in simple terms?

Asset management is the professional practice of investing and managing your money on your behalf, with the goal of growing wealth over time while keeping risk at an acceptable level. Essentially, a specialist makes informed investment decisions so you don't have to navigate markets alone.

What does an asset manager do?

An asset manager builds and oversees your investment portfolio—making buy and sell decisions aligned with your goals and risk tolerance, monitoring performance, and rebalancing when needed. They act as fiduciaries, legally required to put your interests first.

What are the 4 types of assets?

The four main categories are equities (stocks), fixed income (bonds), cash and cash equivalents, and alternative assets such as real estate and commodities. A professionally managed portfolio typically blends all four in proportions suited to your goals and timeline.

What is an example of asset management?

A couple approaching retirement works with an asset manager who builds a diversified portfolio with income-generating bonds and dividend stocks, uses a bucket strategy to fund near-term expenses without touching long-term growth assets, and coordinates withdrawals for tax efficiency—all guided by a written Investment Policy Statement.

What are the 5 P's of asset management?

The commonly cited framework covers Plan, Process, People, Performance, and Price. Each represents a key dimension for evaluating both how an asset manager operates internally and how clients should assess any firm they consider working with.

Is $500,000 enough to work with a financial advisor?

Minimums vary by firm, but portfolio size matters less than fit—the right advisor's fee structure, expertise, and services should align with your specific goals. As financial situations grow more complex, professional guidance tends to deliver more value. Review a firm's Form ADV Part 2A to confirm their minimums and fee disclosures.

Final Takeaway:

Professional asset management gives your savings a structure, a purpose, and a plan that holds up under pressure. Whether you're approaching retirement, managing a complex family situation, or want your money working more deliberately, the goal is the same: find a fiduciary with documented expertise in your circumstances—one who builds for endurance, not just presentation.

Vanguard's research shows that working with an adviser can add around 3% in net returns annually—driven primarily by behavioral coaching that keeps clients from abandoning their plan during market stress, not by market timing. Staying the course, it turns out, is the strategy most investors struggle to execute alone.

Take the next step in your financial journey by exploring our courses page for upcoming live seminars.