General information, not personalised tax, legal or investment advice.

Introduction

Most retirees have a will. According to recent data, 66% of adults in their 70s have a will and 64% have a living will or advance directive. Yet far fewer have a truly coordinated estate plan that integrates with their retirement income, tax strategy, and legacy goals. Without proper planning, assets can be eroded by estate taxes, delayed months or years in probate, or distributed contrary to the retiree's wishes because beneficiary designations override what any will says.

The stakes extend beyond document preparation. Estate planning in retirement intersects with Medicare eligibility, Social Security survivor planning, required minimum distributions (RMDs), and long-term care costs that can deplete an estate by hundreds of thousands of dollars.

That complexity requires coordination across legal, financial, and tax dimensions — coordination most retirees assume happens automatically but rarely does without deliberate oversight.

Here's what every retiree should understand heading into 2026.

Key takeaways

- Estate planning in retirement requires ongoing coordination with your financial plan, not a one-time legal task

- Key documents include a will, durable power of attorney, healthcare directive, and potentially one or more trusts

- 2026 is a critical planning year: the federal estate tax exemption is now $15 million per individual following the One Big Beautiful Bill Act

- Beneficiary designations and trust structures override your will and determine where most assets actually go

- A financial advisor handles account titling, beneficiary reviews, and tax-efficient wealth transfer

Why Estate Planning Looks Different Once You're Retired

Estate planning priorities shift at retirement. The focus moves from accumulation and income protection to distribution, legacy, and incapacity planning. Retirees have more assets at stake, face required minimum distributions that trigger tax consequences, and must account for how long their wealth needs to last — potentially 20 or 30 years.

Unique risks retirees face include:

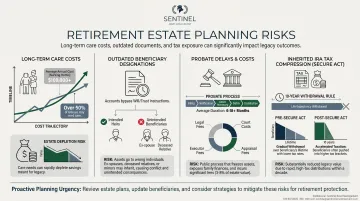

- 70% of adults who reach age 65 will develop severe long-term care needs, and roughly 15% face total costs exceeding $250,000 — enough to deplete a significant portion of an estate

- More than 40% of Americans have never updated beneficiary forms, even after divorce or the death of a spouse

- Plans written decades ago often no longer reflect current family relationships, needs, or intentions

Estate planning for retirees also intersects with Medicare, Medicaid eligibility, Social Security survivor planning, and inherited IRA rules under the SECURE Act. The 10-year distribution requirement for most inherited IRAs compresses beneficiaries' tax liability into a tight window — and without coordinated planning, that tax hit can be substantial.

Each of these factors requires a plan that moves across tax, legal, and income-distribution decisions together, not in isolation.

Even among retirees who have estate documents in place, 14% have never updated them and 13% review them only once per decade or less. As tax laws shift, family circumstances change, and account balances grow, a plan left untouched becomes a liability rather than a safeguard.

Core Estate Planning Documents Every Retiree Needs in 2026

Wills and Powers of Attorney

Last Will and Testament: A will names an executor, specifies asset distribution for probate assets, and can designate guardians for dependents including adult children with special needs. Critically, a will does NOT override beneficiary designations on retirement accounts or life insurance, and does NOT bypass probate for most assets.

Durable Power of Attorney for Finances: This grants a trusted agent authority to manage financial decisions if you become incapacitated. "Durable" means it stays in effect even if you lose capacity — a general power of attorney does not. For retirees managing investment portfolios across multiple accounts, this document is essential to prevent costly guardianship proceedings.

Executor selection deserves careful thought. An executor who is disorganized, geographically distant, or unfamiliar with your accounts can cause significant delays. Professional executors — attorneys or trust companies — charge fees set by state law, often 3–5% of estate value, but may be worth it for complex situations.

Healthcare Directives and Living Wills

Financial authority and healthcare authority are handled through separate documents — both are essential. A living will provides written instructions for end-of-life medical treatment preferences. A healthcare proxy (also called a medical power of attorney) names someone to make healthcare decisions on your behalf. Together, they provide more complete coverage than either alone.

Only 31% of U.S. adults have a living will or advance healthcare directive. Without these documents, family members may need to pursue guardianship through the courts — a process requiring proof of incapacity, significant time and expense, and a court-appointed Guardian Ad Litem.

The stakes are real: guardianship proceedings can take months and cost thousands of dollars, all while critical medical decisions remain in limbo.

These documents are not one-and-done. Review and update them when:

- A major health event changes your treatment preferences

- Your named proxy is no longer the right person

- You relocate to a new state

Most states recognize out-of-state directives, but executing new documents in your state of residence ensures local providers accept them without question.

Trusts, Beneficiary Designations, and Avoiding Probate

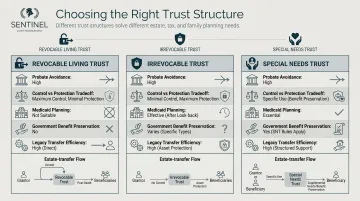

Choosing the Right Trust Structure

Revocable Living Trusts: The most common retiree tool. Assets placed in a properly funded revocable trust pass directly to beneficiaries without probate, maintaining privacy and speed of transfer. The grantor retains control and can change, update, or cancel the trust while alive.

The critical word is "funded" : a trust that hasn't been retitled to include assets provides no probate protection. This coordination between legal documents and actual asset ownership is where many plans fail.

Irrevocable Trusts: Used when retirees need Medicaid planning, asset protection from creditors, or estate tax savings. Once assets are transferred into an irrevocable trust, the grantor loses control. This trade-off makes sense for larger estates or specific protection needs. Setup costs typically range from $2,500 to $5,000, sometimes higher for complex structures.

Special Needs Trusts: Essential when a beneficiary receives government benefits. Leaving assets outright to someone on SSI (which has a $2,000 individual resource limit) or Medicaid can disqualify them from those programs. A properly structured special needs trust preserves eligibility while providing supplemental support beyond what government programs cover.

Beneficiary Designations and Probate Avoidance

Beneficiary designations on retirement accounts (IRAs, 401(k)s), life insurance, and payable-on-death (POD) accounts override what any will says and often represent the majority of a retiree's estate. Financial institutions must follow the beneficiary form, not the will, when the two conflict.

Review and update designations immediately after:

- Divorce or remarriage

- Death of a named beneficiary

- Birth or adoption of grandchildren

- Significant changes in family relationships

Joint ownership with rights of survivorship works as a simple probate-avoidance tool for certain assets like real estate and bank accounts. Limitations include no asset protection, potential unintended gift tax issues, and no contingency if both owners die at the same time.

The average estate takes six to nine months to complete probate, though timelines range from three months to over two years depending on state court backlogs and complexity. With approximately 2.6 million probate cases filed annually in U.S. state courts, the practical case for proper trust funding and updated beneficiary designations is straightforward: assets transfer faster, more privately, and with less court involvement — typically at a fraction of the cost of probate administration.

Tax Strategies Retirees Can't Ignore in 2026

The One Big Beautiful Bill Act (P.L. 119-21) averted the TCJA sunset, setting the 2026 federal estate tax exemption at $15 million per individual. At that threshold, the estate tax touches roughly 0.07% of decedents — only about 2,129 estates owed federal estate tax in 2019. Even so, estates approaching that ceiling benefit from deliberate planning. Three strategies deserve attention in 2026.

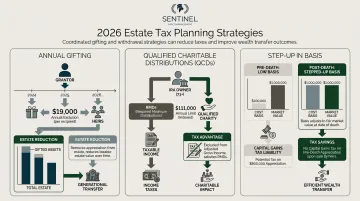

Annual gifting uses the $19,000 per-donee exclusion (2026 amount) to transfer assets without triggering gift tax or eroding the lifetime exemption. Systematic gifting over several years chips away at a taxable estate while putting funds in heirs' hands when they're often most useful.

Qualified Charitable Distributions (QCDs) let retirees age 70½ or older donate up to $111,000 (2026 limit) directly from an IRA to charity — satisfying RMD requirements while keeping the distribution out of taxable income entirely. It's one of the few strategies that handles two tax problems at once.

Step-up in basis is a quieter but powerful tool. Assets held until death reset to fair market value on the date of death, wiping out capital gains accumulated over decades.

That distinction matters when choosing between gifting assets now versus holding them. If you gift appreciated assets during life, the recipient inherits your original cost basis — meaning they'll owe capital gains tax on the full run-up when they sell. Holding those same assets until death can save beneficiaries tens or hundreds of thousands in taxes.

The Role of a Financial Advisor in Your Estate Plan

Most estate planning coordination happens at the financial planning level, not the legal level. This includes beneficiary designation reviews, retirement account titling, tax-efficient withdrawal sequencing, and gifting strategies.

At Sentinel Asset Management, advisors focus on the financial coordination side of estate planning — working with accounts, insurance policies, and ownership structures to ensure assets are structured, titled, and distributed in ways that align with legal documents so the plan actually works as intended.

Financial advisors coordinate the ecosystem around estate planning:

- Reviews all retirement accounts, life insurance policies, and POD accounts to ensure beneficiary designations reflect current intentions and align with your will and trust

- Organizes assets across taxable, tax-deferred, and tax-free accounts so ownership structures support your estate goals

- Sequences withdrawals using structured "bucket" approaches — near-term, mid-term, and long-term funds — to minimize lifetime tax liability while preserving wealth for heirs

- Coordinates annual gifting, charitable distributions, and other wealth transfer techniques with overall retirement income needs

An advisor also flags when a situation calls for an attorney — for instance, when establishing an irrevocable trust, drafting a will with specific bequests, or navigating Medicaid planning. The advisor serves as the ongoing coordinator of the plan, with the attorney executing specific legal instruments as needed.

This coordination is particularly valuable for retirees managing complex portfolios across multiple accounts, where the interaction between withdrawal decisions, tax consequences, and legacy goals requires continuous oversight.

When and How to Keep Your Estate Plan Current

Life events that trigger immediate review:

- Death or incapacity of a named executor, trustee, POA agent, or beneficiary

- Marriage, divorce, or remarriage

- Birth or adoption of grandchildren

- Significant change in asset levels (inheritance, sale of business, major market gains)

- New tax legislation affecting exemptions or rates

- Move to a new state (estate laws, probate processes, and POA/healthcare directive recognition vary significantly)

Recent research shows that among individuals with wills or trusts, 14% have never updated their documents and 13% review them only once per decade or less. Outdated documents are one of the most preventable estate planning failures.

Schedule an annual review — ideally timed with your financial planning meeting. At each checkpoint, confirm:

- Beneficiary designations are current

- Trust funding is complete

- Gifting strategies are on track

- The plan reflects any changes in your health, values, or family circumstances

Relocating to a new state deserves particular attention. While most states recognize out-of-state advance directives, executing fresh documents under your new state's laws ensures local providers and courts accept them without delay.

Frequently Asked Questions

What should I not tell my estate planning attorney?

You should not withhold financial information from your estate planning attorney — complete disclosure ensures proper planning. That said, be cautious about sharing speculative asset values or informal promises made to family members. Documenting these can create legal obligations that are difficult to modify later.

What is the average cost to set up a trust?

A revocable living trust for an individual typically costs around $2,475 nationally in 2026, while joint trust packages (including pour-over wills, financial POAs, and healthcare directives) range from $2,700 to $3,000. Irrevocable trusts cost $2,500 to $5,000 or more due to complexity. Costs vary by state, attorney experience, and estate complexity. A financial advisor handles much of the surrounding coordination outside these legal fees.

How much does it cost to have a lawyer as executor of a will?

Attorney executor fees are often set by state law as a percentage of the estate — typically 3-5% depending on estate size and state. For example, California charges 4% of the first $100,000, while New York charges 5% of the first $100,000. These fees represent a meaningful cost on larger estates. Named family executors are also entitled to similar statutory compensation.

Do I need an attorney for all aspects of estate planning?

No. While an attorney is essential for drafting legal documents (wills, trusts, healthcare directives), much of estate planning is financial work: beneficiary coordination, account titling, tax strategy, and retirement distribution planning. These tasks are handled by a financial advisor who coordinates the overall plan and ensures legal documents align with how your assets are actually structured and titled.

How does the 2026 estate tax exemption change affect my plan?

The One Big Beautiful Bill Act set the 2026 federal estate tax exemption at $15 million per individual (up from previous levels), averting the TCJA sunset. If your estate approaches or exceeds this threshold, consult a financial advisor immediately to explore gifting and trust strategies. Estates well below this threshold can still reduce tax exposure through annual gift exclusions, beneficiary updates, and proper account titling.

Take the next step in your financial journey by exploring our courses page for upcoming live seminars.