Introduction

Retirement income planning isn't just about how much you've saved—it's about how much you actually keep. Taxes can dramatically erode what retirees take home each year, with research from Boston College's Center for Retirement Research revealing that taxes consume approximately 16% of retirement income for the top 5% of households, rising to nearly 23% for the top 1%. Over a 20-30 year retirement, that adds up to hundreds of thousands of dollars lost to the IRS.

Most retirement plans focus heavily on accumulation—maximizing 401(k) contributions, building IRA balances, watching investment growth. The withdrawal side gets far less attention, and that's where retirees overpay.

Drawing from accounts without considering tax treatment, Social Security interaction, Medicare premium impacts, or bracket thresholds is expensive. Each withdrawal decision creates a ripple effect across your entire financial picture.

This guide covers the core strategies of tax-aware retirement income planning: the three-bucket tax structure, strategic withdrawal sequencing, Roth conversions during the "tax-free window," RMD management, Social Security timing, and additional tools including tax-loss harvesting and charitable giving. Applied correctly, these strategies can reduce your lifetime tax bill by over 40% and measurably extend how long your portfolio lasts.

Key takeaways

- Tax-aware retirement planning targets lifetime tax minimization, not just annual bills, so more of every dollar withdrawn stays with you

- Spreading savings across three "tax buckets" (tax-deferred, tax-free, taxable) creates flexibility to control taxable income annually

- Strategic withdrawal sequencing, Roth conversions during low-income years, and proactive RMD planning dramatically reduce tax exposure

- Social Security benefits and Medicare premiums are both income-sensitive, so coordinating income levels helps avoid costly surcharges

- Tax-loss harvesting, qualified charitable distributions, and asset location add meaningful savings when used correctly

Why Tax-Aware Retirement Planning Matters More Than You Think

Many retirees assume their tax rate will drop in retirement compared to their working years. However, the opposite is often true. Required Minimum Distributions beginning at age 73, Social Security income, and investment distributions can push retirees into the same or higher brackets than before—especially when the majority of savings sit in tax-deferred accounts.

Tax-aware retirement income planning is a legal, strategic approach to optimizing which accounts you draw from, when, and in what amounts. Rather than making withdrawal decisions in isolation, it coordinates across your full financial picture—balancing bracket thresholds, RMD obligations, Social Security taxation, and Medicare premium surcharges.

The decisions made in the first 5-10 years of retirement often set the tax trajectory for the entire retirement period. Three early choices carry the most permanent consequences:

- Roth conversion timing — windows before RMDs begin are often the most favorable

- Social Security claiming age — affects both benefit size and taxable income for decades

- Withdrawal sequencing — which accounts you tap first determines your bracket exposure year by year

A hypothetical analysis by Fidelity found that switching from a traditional sequential withdrawal strategy to a proportional approach reduced total lifetime taxes by over 40%—from approximately $56,000 to $31,500—and extended the portfolio's life by roughly one year. Getting these decisions right early is what separates a well-structured retirement income plan from one that quietly erodes over time.

The Three Tax Buckets: Building a Flexible Retirement Income Base

Tax-aware retirement planning starts with one structural question: where does your money live? Each account type carries a different tax treatment, and knowing the difference gives you real control over what you keep.

| Bucket | Account Types | Tax on Withdrawal | RMD Required? |

|---|---|---|---|

| Tax-Deferred | Traditional IRA, 401(k), 403(b) | Ordinary income | Yes |

| Tax-Free | Roth IRA, Roth 401(k) | None (qualified withdrawals) | No (original owner) |

| Taxable | Brokerage accounts | Capital gains / dividend tax | No |

Why Tax Bucket Diversification Matters

Diversification across all three bucket types—not just across asset classes—gives retirees the ability to blend income sources each year. This flexibility allows you to:

- Stay within favorable tax brackets

- Avoid Medicare IRMAA surcharge thresholds

- Manage Social Security taxation

- Respond strategically to changing tax laws

Practical advantages of each bucket:

- Tax-deferred accounts work best in years with available deductions or lower income — draw from them strategically to fill brackets without crossing into a higher tier

- Roth accounts deliver tax-free income when you need to limit your taxable total — particularly valuable in high-income years or when planning for heirs

- Taxable accounts offer complete withdrawal flexibility and let lower-income filers use the 0% long-term capital gains rate to their advantage

The HSA: A Triple-Tax-Advantaged Tool

Health Savings Accounts function as a powerful fourth bucket for retirement planning. Contributions are pre-tax, growth is tax-free, and withdrawals for qualified medical expenses are tax-free. After age 65, non-medical withdrawals are taxed as ordinary income but penalty-free, making HSAs a useful supplemental retirement resource.

Sentinel Asset Management's structured withdrawal bucket approach aligns near-term, mid-term, and long-term income needs with the right account types—helping clients insulate cash flow from market volatility while maintaining tax efficiency across their portfolio.

Strategic Withdrawal Sequencing: Choosing Which Bucket to Tap and When

The traditional withdrawal sequence follows this order: taxable first, then tax-deferred, then Roth. The logic is to let tax-advantaged accounts grow longer while spending down taxable assets. However, this "one account at a time" approach creates a "tax bump" when switching to tax-deferred accounts and may leave large untouched Roth balances with missed conversion opportunities.

The Proportional Withdrawal Alternative

Rather than drawing one account dry before moving to the next, the proportional strategy withdraws from each account type based on its proportion of total savings. Research demonstrates this approach:

- Spreads taxable income more evenly across retirement years

- Keeps retirees in consistent lower brackets

- Reduces total lifetime taxes paid

- Often extends portfolio longevity

Bracket Management: The Key Skill

Each year, identify how much room remains in your current tax bracket, then draw accordingly from tax-deferred accounts to fill—but not exceed—that bracket. Supplement remaining income needs from Roth or taxable accounts.

For example: If you're in the 12% bracket with $10,000 of room remaining before crossing into the 22% bracket, you might take exactly $10,000 from your traditional IRA, then draw additional needed income from your Roth IRA to avoid pushing into the higher bracket.

Impact on Social Security Taxation

Bracket management doesn't stop at your IRA—it directly affects how much of your Social Security gets taxed. Up to 85% of benefits can become taxable depending on your combined income, and provisional income thresholds trigger that taxation at specific levels:

| Filing Status | Up to 50% Taxable | Up to 85% Taxable |

|---|---|---|

| Single/Head of Household | > $25,000 | > $34,000 |

| Married Filing Jointly | > $32,000 | > $44,000 |

Keeping total income below these provisional income thresholds—particularly in early retirement—becomes a critical sequencing goal.

Your Optimal Sequence Depends on These Six Variables

No single withdrawal order works for everyone. The right sequence for your situation turns on:

- Total savings across taxable, tax-deferred, and Roth accounts

- Projected RMD size and timing

- Social Security claiming age

- Filing status and state tax treatment

- Legacy and estate planning goals

Getting these variables wrong—even by a few years—can mean paying tens of thousands more in avoidable taxes. A personalized sequencing plan, reviewed annually as tax laws and income needs shift, is what converts strategy into savings.

Roth Conversions, RMDs, and the Tax-Free Window Every Retiree Should Know

The Tax-Free Window Opportunity

The years between retirement and the onset of RMDs at age 73 (rising to 75 in 2033 under SECURE 2.0) offer a narrow but valuable tax planning window. During this period, income is often at its lowest—no RMDs yet, Social Security may be delayed—creating space to convert traditional IRA/401(k) funds to Roth at favorable rates before mandatory distributions force higher taxable income.

How Roth Conversions Work

The IRS treats the converted amount as ordinary income in the year of conversion, taxed at your current marginal rate. However, the converted funds then grow tax-free and qualified withdrawals are never taxed again. Roth IRAs also have no RMDs during the account holder's lifetime, reducing future forced income.

Strategic Approach: Bracket-Filling Conversions

Rather than converting everything at once (which could push you into a higher bracket), experienced advisors model annual "partial conversions"—converting enough each year to fill up to the top of a lower tax bracket without crossing into a higher one. Michael Kitces and other industry experts recommend targeting the top of the 12%, 22%, or 24% brackets before stopping. The jumps to 22%, 24%, and 32% represent steep marginal rate increases that make crossing those thresholds costly.

Understanding RMDs and Their Tax Implications

Starting at age 73, the IRS requires minimum annual withdrawals from all tax-deferred accounts. RMDs are calculated by dividing the prior December 31 account balance by a life expectancy factor from the IRS Uniform Lifetime Table.

Key RMD considerations:

- Fully taxable as ordinary income

- Compound over time as account balances grow

- Interact with Social Security taxation

- Can trigger Medicare IRMAA surcharges

- Carry a 25% excise tax penalty for missed or insufficient distributions (reducible to 10% if corrected within two years)

Strategies to Manage or Reduce RMDs

Three approaches can meaningfully reduce RMD exposure over time:

- Roth conversions before age 73 shrink the tax-deferred balance driving future RMD calculations—every dollar converted now is one less dollar subject to forced withdrawal later

- Qualified Charitable Distributions (QCDs), available from age 70½, direct IRA funds straight to qualified charities; they count toward your RMD but never appear in taxable income

- Account consolidation reduces administrative complexity and lowers the risk of missing a distribution across multiple accounts

Coordinating these strategies in sequence—rather than in isolation—is what separates a reactive RMD plan from one that meaningfully reduces lifetime tax drag.

Social Security Timing, IRMAA, and Other Hidden Tax Triggers in Retirement

Social Security Benefit Taxation

Benefits become partially taxable when "combined income" (AGI + nontaxable interest + 50% of Social Security benefits) exceeds IRS thresholds. Unlike tax brackets, Congress has never indexed these thresholds for inflation — they have sat unchanged for decades.

Delaying Social Security to age 70 increases monthly benefits substantially but also pushes more Social Security income into the taxable range later. This makes early retirement the ideal time for Roth conversions to lower future combined income.

Two additional thresholds can catch retirees off guard when income spikes:

- Net Investment Income Tax (NIIT): An extra 3.8% tax on investment income kicks in when MAGI exceeds $200,000 (Single) or $250,000 (Married Filing Jointly).

- Capital Gains Rate Shifts: For 2025, the 0% long-term capital gains rate applies up to $48,350 (Single) or $96,700 (Married Filing Jointly). Large IRA withdrawals stack onto ordinary income and can push gains into the 15% or 20% bracket.

Additional Tax-Smart Tools: Loss Harvesting, Charitable Giving, and Asset Location

Tax-Loss Harvesting

For taxable brokerage accounts, selling investments at a loss offsets realized capital gains, potentially reducing tax owed on profitable sales. Up to $3,000 in excess losses can offset ordinary income annually, with additional losses carried forward to future years.

The wash-sale rule: Cannot repurchase the same or substantially identical security within 30 days before or after the sale. To maintain market exposure, replace with ETFs tracking different indexes.

Qualified Charitable Distributions (QCDs)

The most tax-efficient giving strategy available to retirees aged 70½ and older: up to $108,000 in 2025 and $111,000 in 2026 (indexed for inflation) can be transferred directly from a traditional IRA to a qualified charity. The distribution counts toward your RMD and is excluded from taxable income entirely. This matters most for retirees who take the standard deduction and would receive no additional benefit from a regular charitable deduction.

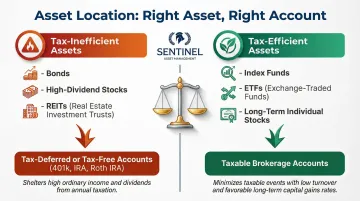

Asset Location

The principle is straightforward: match each asset type to the account where it's taxed most favorably.

- Tax-inefficient assets (bonds, high-dividend stocks, REITs) belong inside tax-deferred or tax-free accounts, where income isn't immediately taxable

- Tax-efficient assets (index funds, ETFs, individual stocks held long-term) fit better in taxable accounts, where lower long-term capital gains rates apply

Sentinel Asset Management builds this asset location discipline into every client portfolio — coordinating which accounts hold which assets, and when gains are realized, to reduce lifetime tax liability as part of an integrated financial plan.

Frequently Asked Questions

What does "tax-aware" retirement income planning actually mean?

Tax-aware planning means making decisions about when and from which accounts to withdraw income with the goal of minimizing lifetime taxes—not just the current year's tax bill. It coordinates withdrawals, bracket thresholds, RMDs, Social Security, and investment choices in one unified strategy rather than treating each decision in isolation.

What is the best withdrawal order for retirement accounts?

There is no universal "best" order. The traditional sequence (taxable, then tax-deferred, then Roth) applies in some situations, but many retirees benefit from a proportional or tax-bracket-managed approach that blends account types annually to smooth taxable income and reduce lifetime taxes. Your optimal sequence depends on your savings mix, RMD projections, and legacy goals.

When is the right time to do a Roth conversion in retirement?

Roth conversions are generally most advantageous during the "tax-free window" between retirement and age 73, when income is lower and before RMDs force larger taxable distributions. The optimal conversion amount each year is typically the amount that fills a favorable tax bracket without crossing into a higher one—often targeting the top of the 12% or 22% brackets.

How do Required Minimum Distributions affect my taxes?

RMDs from tax-deferred accounts are fully taxable as ordinary income and can push retirees into higher brackets, trigger Social Security taxation, and cause IRMAA surcharges. Proactive strategies like Roth conversions before age 73 and Qualified Charitable Distributions after age 70½ can significantly reduce RMD-driven tax exposure.

Can I reduce the taxes on my Social Security benefits?

Up to 85% of Social Security benefits can be taxable based on combined income. Strategic withdrawal sequencing—drawing on Roth funds or managing taxable account withdrawals to keep combined income below IRS thresholds—can reduce or eliminate the taxable portion, depending on your income mix.

What is IRMAA and how can I avoid it?

IRMAA is a Medicare premium surcharge triggered when MAGI exceeds certain thresholds, assessed based on tax returns from two years prior. Avoiding income spikes—large conversions, asset sales—and spacing out conversions strategically keeps you below surcharge thresholds. If a life-changing event caused unusually high income, you can appeal the assessment using Form SSA-44.

Take the next step in your financial journey by exploring our courses page for upcoming live seminars.