General information, not personalised tax, legal or investment advice.

Introduction

Most investors only discover their portfolio's true vulnerabilities during a market crash—when it's already too late to act. By then, losses have materialized, withdrawal plans are derailed, and options have narrowed. Portfolio stress testing flips this dynamic: it lets you see the danger before it arrives, revealing how your investments would respond to market downturns, inflation spikes, and liquidity crunches while you still have time to adjust.

Stress testing isn't reserved for banks or institutional investors. It applies to anyone building wealth toward retirement, protecting a legacy, or managing long-term financial security.

For retirees especially, it surfaces risks that traditional metrics miss. Sequence-of-returns risk is one of the most consequential: when losses occur early in the withdrawal phase, they can permanently impair a portfolio in ways that a later recovery simply cannot repair.

This guide covers:

- What portfolio stress testing is and how it works

- Why it matters for individual investors, not just institutions

- How to apply it in practice across different scenarios

- How it connects to smarter retirement income and withdrawal planning

Key takeaways

- Portfolio stress testing simulates how investments perform under adverse conditions—crashes, rate hikes, inflation—so vulnerabilities surface before they cost you

- Identifies hidden vulnerabilities and builds portfolios resilient enough to survive real turbulence

- Retirees face distinct risks—sequence of returns, purchasing power erosion, liquidity crunches—that stress testing is uniquely built to expose

- A structured process—defining goals, modeling scenarios, and adjusting allocations—turns stress test results into a more resilient portfolio

- Most powerful when embedded into ongoing financial planning, not run once and forgotten

What Is Portfolio Stress Testing?

Portfolio stress testing is a simulation process that evaluates how your investments would respond to specific adverse economic or market scenarios. It allows you to measure potential losses, identify structural vulnerabilities, and plan responses—without suffering real financial consequences.

Two Primary Approaches

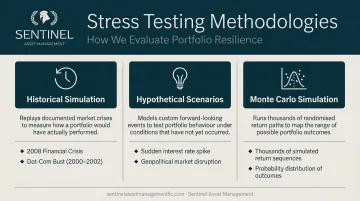

Stress testing operates across two distinct methodologies:

Historical simulations replay past crises against your current portfolio. Examples include the 2008 financial crisis, the dot-com bust of 2000-2002, or the 1970s stagflation period. During the 2008-2009 crisis, the S&P 500 lost over 53% from peak to trough, but a diversified 60/40 portfolio declined by only 23.7%, demonstrating how allocation choices affect downside protection.

Hypothetical scenarios create forward-looking "what if" events tailored to your specific risks: a sudden 40% equity drawdown at retirement onset, a prolonged low-interest-rate environment, or stagflation combining high inflation with weak growth.

Monte Carlo simulation models thousands of random return paths based on statistical assumptions, quantifying the probability of portfolio depletion over time.

Beyond Standard Risk Metrics

Stress testing differs fundamentally from standard risk measures like standard deviation or beta. Standard deviation assumes symmetrical, normally distributed returns—but it fails to capture skewness, kurtosis (fat tails), and the true risk of extreme downside losses. Beta measures volatility relative to a benchmark but ignores non-linear exposures and sequence-of-returns risk—the compounding damage that occurs when you're withdrawing from a falling portfolio.

Stress testing captures tail risks and asymmetric outcomes that averages miss. For retirement-stage investors, where large losses carry permanent consequences, that distinction is critical.

Key Risks Every Portfolio Should Be Tested Against

Not all risks are equal. The risks most likely to derail a retirement portfolio often differ from those getting media attention. Stress testing is most useful when it targets the risks most relevant to your specific financial situation and time horizon.

Market Risk: Sequence-of-Returns Danger

A sustained bear market—especially early in retirement—can permanently impair a portfolio through sequence-of-returns risk. A 30% or 40% loss in year one of withdrawals can be far more damaging than the same loss a decade earlier, because selling depressed assets to fund living expenses permanently reduces the portfolio's ability to recover.

Research from Vanguard shows that retirees facing severe bear markets early in retirement with a fixed 5% withdrawal rate faced an 81% probability of portfolio depletion. Those who retired into full bear markets were 31% more likely to outlive their wealth compared to peers who retired just a year or two later.

Purchasing Power Risk: Inflation's Silent Erosion

Inflation steadily erodes real portfolio value and income purchasing power over time. A portfolio that "holds steady" in nominal terms can still lose substantial real value across a 20-30 year retirement.

Historical data from the Bureau of Labor Statistics shows cumulative inflation from 1970 to 1990 was 236.9%, drastically reducing fixed-income purchasing power. Even moderate 3% inflation erodes the value of a dollar by more than 50% over 25 years.

Sentinel's PRIME risk framework identifies Purchasing Power Risk as a core category to monitor and stress-test for, alongside Reinvestment, Interest Rate, Market, and Exchange Risk.

Interest Rate Risk: Price vs. Reinvestment

Rising interest rates affect fixed-income holdings and bond-heavy portfolios, particularly for retirees relying on bond income. Critically, rate movements cut both ways:

- Rising rates: Bond prices fall, reducing the current market value of existing holdings (price risk)

- Falling rates: Maturing bonds must be reinvested at lower yields, shrinking future income (reinvestment risk)

Both scenarios can erode retirement income in ways that aren't obvious until a stress test surfaces them.

Liquidity Risk: Unexpected Cash Needs

Stress test what happens when a large, unexpected cash need arises—healthcare costs, long-term care, estate expenses—at the same time markets are down. A 65-year-old retiring in 2025 is estimated to need $172,500 in after-tax savings to cover healthcare expenses throughout retirement, excluding long-term care.

Portfolios that look stable on paper can create real hardship if liquid assets are insufficient during a drawdown.

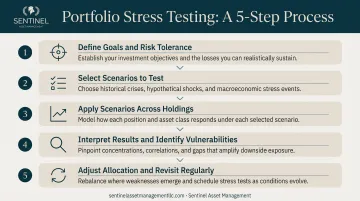

How Portfolio Stress Testing Works: Step by Step

Stress testing doesn't require institutional-grade software to be meaningful—but it does require intentionality. The process below reflects how a disciplined advisor-led stress test works in practice for individual and retirement portfolios.

Step 1: Define Financial Goals and Risk Tolerance

Establish the baseline: what are the portfolio's income requirements, time horizon, and acceptable loss thresholds? Without a clear objective, stress testing produces numbers without direction—and numbers without direction don't protect a retirement.

A formal Investment Policy Statement (IPS) creates the foundation for a stress test by codifying goals, constraints, and risk parameters upfront. According to the CFA Institute's position paper on Investment Policy Statements, the IPS establishes governance, accountability, and predetermined courses of action during market disruptions. It documents investment objectives, loss thresholds the investor cannot tolerate, and how often the portfolio should be reviewed.

Step 2: Select Scenarios to Test

Choose a mix of historical and hypothetical scenarios relevant to the investor's life stage. For retirees, relevant scenarios include:

- A 2008-style equity crash with specific drawdown depth and duration

- A 1970s-style inflation surge combining high inflation with weak equity returns

- A prolonged low-yield environment forcing reinvestment at lower rates

- A combined downturn plus unexpected large expense (healthcare emergency during a bear market)

Scenarios should be plausible and personally relevant—not just statistically extreme.

Step 3: Apply Scenarios Across Portfolio Holdings

Run each scenario against the portfolio's actual allocation—equities, fixed income, alternatives, cash—to estimate the impact on total value, income generation, and liquidity. This step often reveals correlations that aren't obvious in normal markets: assets that appear diversified but move together when a crisis hits.

A portfolio that looks well-balanced on paper may have hidden concentration risk that only emerges under stress conditions.

Step 4: Interpret Results and Identify Vulnerabilities

Analyze the results to identify which scenario causes the most damage, which holdings are most exposed, and whether the portfolio can sustain its income requirements under stress. For retirees specifically, the key question is whether a 30–40% drawdown would force selling at a loss to meet income needs—because that sequence-of-returns risk is often more damaging than the drawdown itself.

Step 5: Adjust Allocation and Revisit Regularly

Use stress test findings to drive concrete changes: rebalancing toward less-correlated assets, shifting to shorter-duration bonds ahead of a rising-rate environment, or building withdrawal buckets that ring-fence near-term income needs from market volatility.

Stress tests aren't a one-time exercise. Vanguard's portfolio rebalancing guidance recommends reviewing at least annually—and immediately after major life events or significant market moves.

Stress Testing in Action: A Retirement Portfolio Walkthrough

Consider a simplified but realistic example: a couple in their early 60s with a diversified portfolio of equities and bonds, five years from retirement, stress-testing their portfolio against a market downturn scenario combined with rising inflation.

Test Setup

Their IPS defines a maximum tolerable drawdown of 20%, an income need of $80,000 per year in retirement, and a 30-year planning horizon. The scenario applies:

- 35% equity decline

- 15% bond value reduction (due to rising rates)

- 4% annual inflation rate for five years

This mirrors a stagflationary environment similar to the 1970s.

What the Results Reveal

The portfolio's projected income falls short of their $80,000 target in years 2–5 of retirement if the downturn occurs at the point of withdrawal onset. The stress test exposes sequence-of-returns risk directly and puts a number on it: instead of sustainable $80,000 annual withdrawals, the portfolio can only support $64,000 without accelerating portfolio depletion.

Concrete Adjustments

That $16,000 annual shortfall prompted three targeted adjustments:

- Shifting a portion of near-term income needs (covering 2-3 years) into a short-duration "cash bucket"

- Reducing equity concentration from 65% to 55%

- Introducing inflation-linked assets to protect purchasing power

The stress test couldn't predict whether a downturn would happen. What it did was expose a structural vulnerability clearly enough to act on it before any real crisis forced the couple's hand.

How Sentinel Asset Management Approaches Portfolio Stress Testing

Sentinel serves as a strategic partner for clients who want their portfolios built and maintained to withstand real-world stress, not just optimized for average conditions. Every Sentinel client portfolio is guided by a formal Investment Policy Statement and stress-tested under multiple market conditions as part of the firm's core advisory process.

Sentinel's PRIME risk framework structures how stress scenarios are designed—ensuring the risks most likely to affect long-term outcomes are systematically evaluated, not overlooked. The five risk categories it covers:

- Purchasing Power Risk — inflation eroding real returns over time

- Reinvestment Risk — income reinvested at lower rates than expected

- Interest Rate Risk — rate changes affecting bond values and income

- Market Risk — broad equity and asset price volatility

- Exchange Risk — currency fluctuations affecting internationally held assets

The firm's structured withdrawal "bucket" strategy is designed to insulate near-term income needs from market volatility—a design principle informed by stress testing outcomes. For families navigating retirement, legacy planning, or special needs financial planning, this kind of stress-informed portfolio construction provides the confidence that the plan can hold together when markets don't cooperate.

That track record spans 2,000+ clients guided into retirement and 25 years supporting families with special needs—experience that shapes how Sentinel stress-tests for the scenarios that matter most to each family's specific financial reality.

Frequently Asked Questions

What is portfolio stress testing for individual investors?

Portfolio stress testing for individuals involves simulating how a personal investment portfolio would perform under adverse scenarios—like market crashes or inflation spikes—to identify vulnerabilities and make proactive adjustments before real losses occur.

How often should I stress test my investment portfolio?

Portfolios should be stress tested at least once a year. Beyond that, revisit whenever a significant life event occurs (approaching retirement, major withdrawal, inheritance, divorce) or when market conditions shift materially.

What scenarios should I include when stress testing a retirement portfolio?

The most relevant scenarios for retirees include a major equity market drawdown, a sustained high-inflation period, a rising interest rate environment, and a simultaneous large cash need—since each can compromise retirement income in distinct ways.

What is the difference between historical and hypothetical stress testing?

Historical stress testing replays actual past crises (such as the 2008 financial crisis) against a portfolio, while hypothetical testing creates forward-looking "what if" scenarios. Both are useful, and a robust stress test typically combines both approaches.

Can stress testing prevent portfolio losses?

Stress testing cannot prevent losses, but it reveals how large those losses could be and where they would originate—enabling investors to adjust their portfolios before a crisis hits, rather than reacting emotionally during one.

How does portfolio stress testing connect to retirement income planning?

Stress testing is especially critical in retirement because early losses during the withdrawal phase carry asymmetric damage (sequence-of-returns risk). Understanding portfolio behavior under stress helps advisors build income strategies, including structured withdrawal buckets, that sustain cash flow even during market downturns.

Take the next step in your financial journey by exploring our courses page for upcoming live seminars.