This guide walks through the most effective, proven tax planning strategies — from maximizing retirement accounts and harvesting investment losses to advanced charitable vehicles and estate gifting — and explains why these strategies are most powerful when coordinated together, not applied in isolation.

Key takeaways

- HNWIs face compounding tax complexity from multiple income streams, investment portfolios, and estate exposure simultaneously

- Expiring provisions from recent tax legislation create a time-sensitive planning window — key rules are set to shift in 2026

- Maximizing tax-advantaged accounts (401(k), HSA, Roth conversions) reduces current and future tax liability

- Tax-loss harvesting and asset location together can add 0.47%–1.27% to annual after-tax returns

- Coordinated planning across all strategies — not piecemeal application — compounds into greater long-term tax savings than any single tactic alone

Why Tax Planning for High-Net-Worth Individuals Is Different

Standard tax advice like "max your 401(k)" doesn't account for the compounding complexity HNWIs face: multiple income streams, large investment portfolios, estate exposure, and the possibility of being subject to the 3.8% net investment income tax (NIIT). The NIIT applies at a modified adjusted gross income threshold of $250,000 for married couples filing jointly, adding another layer of tax burden on investment income for high earners.

A Legislative Window of Opportunity

The current tax environment — shaped by the One Big Beautiful Bill Act (OBBBA) enacted in 2025 — has created a window of planning opportunity. Key provisions include:

- Permanently increases the base estate tax exemption to $15 million starting in 2026

- Makes individual tax rates permanent, providing long-term planning certainty

- Introduces a 0.5% AGI floor on itemized charitable deductions (effective 2026)

- Caps the value of itemized deductions at 35% for top earners (effective 2026)

For 2025 only, the SALT deduction cap temporarily rises to $40,000 before reverting to $10,000 in 2030. This creates a one-year planning window to maximize state and local tax deductions.

Taken together, these changes reward action in 2025. Once 2026 arrives, the more restrictive charitable deduction rules take effect — making current-year contributions worth more under today's rules than they will be under tomorrow's.

Defining "High-Net-Worth" in This Context

For tax planning purposes, "high-net-worth" typically refers to individuals or households with $1M–$5M+ in liquid assets. Strategies scale in complexity as wealth grows — what works for someone with $1M may differ in both approach and scale from what's appropriate for a $10M+ portfolio. Sophisticated tax planning typically becomes essential around $1–2M in investable assets.

Maximizing Tax-Advantaged Accounts Before and During Retirement

Pre-tax retirement accounts form the foundation of tax reduction for high earners. 401(k) contributions reduce taxable income dollar-for-dollar in the contribution year.

2025 Contribution Limits:

- Employee 401(k) deferral: $23,500

- Catch-up contribution (age 50+): $7,500

- Enhanced catch-up (ages 60-63): $11,250

- Combined employer/employee limit: $70,000

For business owners and executives, maximizing the full $70,000 combined limit creates substantial tax savings while building retirement assets.

Health Savings Accounts: The Triple-Tax Advantage

HSAs represent one of the most powerful tax vehicles available: contributions are deductible, growth is tax-free, and qualified medical withdrawals are tax-free.

2025 HSA Limits:

- Individual coverage: $4,300

- Family coverage: $8,550

Unused HSA funds carry forward indefinitely, making them an underused retirement asset for HNWIs. Unlike Flexible Spending Accounts, there's no "use it or lose it" provision. Paying medical expenses out-of-pocket during working years lets HSA balances compound tax-free for decades, then cover healthcare costs in retirement.

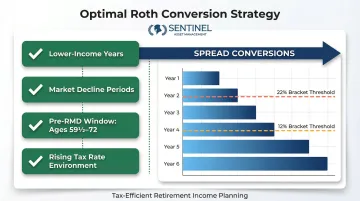

Roth Conversion Strategy: Pay Taxes Now, Grow Tax-Free Forever

Converting traditional IRA or 401(k) funds to a Roth account triggers taxes now but creates a tax-free growth vehicle for the future.

Optimal conditions for Roth conversions:

- Lower-income years (between jobs, early retirement, business loss years)

- Periods of market decline when account values are temporarily depressed

- Years before RMDs begin (ages 59½ to 72)

- When tax rates are scheduled to increase

Timing matters. Converting too much in a single year can push income into higher brackets and negate the benefit. Spreading conversions across several years — filling up lower brackets incrementally — produces the best long-term outcome.

529 Plan Front-Loading as Estate Reduction Tool

IRS rules allow superfunding — contributing up to five years' worth of annual gift exclusions at once per beneficiary. With the 2025 annual exclusion at $19,000, an individual can contribute $95,000 per beneficiary ($190,000 for married couples) without triggering gift taxes.

This strategy serves dual purposes: funding education tax-efficiently while reducing the taxable estate. For HNW families with children or grandchildren, this accelerates wealth transfer while maintaining control over education funding.

The RMD Planning Window Most Retirees Miss

Required Minimum Distributions create a forced taxable event in retirement starting at age 73. Proactive Roth conversion or account drawdown sequencing before RMDs begin can meaningfully reduce a retiree's lifetime tax burden.

The "tax torpedo" effect: Failing to plan for RMDs can cause marginal tax rates to spike when RMDs stack on top of Social Security benefits. Because of how Social Security income is taxed, marginal rates can reach 150% or 185% of the statutory bracket, producing effective marginal rates as high as 40.7%.

The window between retirement and age 73 is the most valuable tax planning period many retirees never use.

Investment Tax Strategies: Tax-Loss Harvesting and Asset Location

Tax-loss harvesting involves selling underperforming investments to realize losses that offset capital gains elsewhere in the portfolio. The IRS allows up to $3,000 of excess losses to offset ordinary income annually, with additional losses carried forward indefinitely.

This strategy is especially valuable for HNWIs who face large capital gains events from concentrated positions or portfolio rebalancing. Research shows tax-loss harvesting can add 0.47% to 1.27% annualized after-tax return over 15 years, depending on the investor's net-worth profile and tax situation.

Navigating the Wash Sale Rule

The wash sale rule prohibits repurchasing a "substantially identical" security within 30 days before or after the sale, or the loss is disallowed. Skilled implementation means replacing sold securities with highly correlated but not identical alternatives, preserving portfolio exposure while capturing the tax deduction.

For example, selling a large-cap growth fund and purchasing a different large-cap growth fund from another provider maintains market exposure while securing the tax benefit.

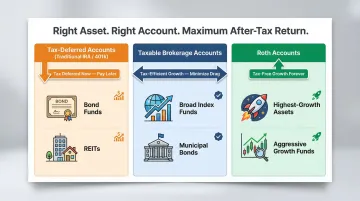

Asset Location: Where You Hold It Matters as Much as What You Own

Asset location strategy assigns investments to account types based on their tax treatment. Optimal asset location can add 5 to 30 basis points of annualized after-tax return over 20 years compared to equal-location strategies. The general framework:

- Place ordinary income-generating assets (bond funds, REITs) inside tax-deferred accounts like traditional IRAs

- Hold tax-efficient investments (broad index funds, municipal bonds) in taxable brokerage accounts

- Use Roth accounts for highest-growth assets to maximize tax-free compounding

Municipal Bonds for High-Bracket Investors

Municipal bond interest is exempt from federal income tax and may be state-tax-exempt depending on the investor's residence. For investors in the top federal brackets, the after-tax yield of munis can exceed that of comparable taxable bonds.

Tax-equivalent yield formula: Tax-Exempt Yield ÷ (1 – Marginal Tax Rate)

A 4.00% tax-free municipal bond equals a 6.36% taxable equivalent yield for an investor in the 37% federal bracket.

How Sentinel Asset Management Builds Tax-Efficient Portfolios

Sentinel builds each client portfolio around their specific tax situation, income needs, and long-term goals — not a generic risk profile. That means matching asset type to account type, structuring withdrawals to minimize tax drag, and revisiting the strategy as tax law and personal circumstances change. The result is a portfolio designed to grow and transfer wealth as efficiently as possible.

Advanced Charitable Giving Strategies That Serve Double Duty

For charitably inclined HNWIs, the right giving structure can reduce taxable income, minimize capital gains, and direct more wealth to causes — all at once.

Donor-Advised Funds: Time Your Deduction, Not Your Gifts

A donor contributes cash or appreciated assets to a Donor-Advised Fund, receives an immediate charitable deduction, then directs grants to charities over time.

2025 deductibility limits:

- Cash contributions: 60% of AGI

- Appreciated assets: 30% of AGI

The strategic value: using a high-income year to make a large DAF contribution, then distributing over multiple years. This "bunching" strategy allows taxpayers to exceed the standard deduction in high-income years while maintaining consistent charitable support.

Critical planning note: Changes to charitable deduction limits take effect in 2026, when a new 0.5% AGI floor will apply. Donations below this threshold won't be deductible, making 2025 contributions more valuable.

Donating Appreciated Securities: Avoid the Gain, Claim the Deduction

By giving shares held longer than one year directly to charity, the donor avoids capital gains tax on the appreciation, claims a deduction for the full fair market value, and allows the charity to sell tax-free.

Selling the security first and donating the cash proceeds instead triggers capital gains tax — reducing both the net charitable impact and the deduction value.

Qualified Charitable Distributions for Retirees

Individuals 70½ or older can transfer up to $108,000 annually directly from an IRA to a qualifying charity in 2025. This satisfies RMD requirements without the distribution counting as taxable income.

The QCD bypasses AGI entirely — a critical distinction for retired HNWIs. That means no downstream impact on Social Security taxation, Medicare premiums, or other AGI-triggered thresholds.

Charitable Remainder Trusts for Complex Estate Situations

For ultra-HNW individuals, a Charitable Remainder Trust allows the donor to transfer appreciated assets to the trust, receive an income stream for a defined period, and have the remainder pass to charity.

A well-structured CRT:

- Reduces capital gains exposure on the transferred asset

- Generates a partial charitable deduction in the year of contribution

- Provides a recurring income stream for retirement

CRTs are best suited for highly appreciated real estate or concentrated stock positions — situations where the tax drag on a direct sale would otherwise be significant.

Estate Planning and Strategic Lifetime Gifting

Strategic lifetime gifting is one of the simplest ways to reduce the taxable estate over time without touching the lifetime exemption.

2025 annual gift tax exclusion: $19,000 per recipient

Married couples can combine exclusions to gift $38,000 per recipient per year. For a couple with three children and six grandchildren, this allows $342,000 in annual tax-free wealth transfer.

With the lifetime exemption potentially declining after 2026, acting now carries added urgency.

Advanced Gifting Vehicles

Two vehicles stand out for high-net-worth families looking to move wealth efficiently:

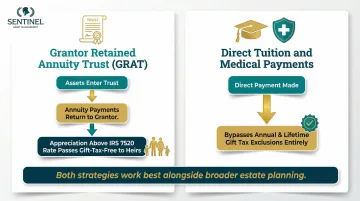

- Grantor Retained Annuity Trusts (GRATs) transfer asset appreciation above the IRS Section 7520 rate to heirs with minimal gift tax — if trust assets outpace that rate, the excess passes gift-tax-free to beneficiaries

- Direct tuition and medical payments made to educational institutions or medical providers bypass both annual and lifetime exclusions entirely, making them one of the most overlooked wealth transfer tools available

When estates are likely to exceed the federal exemption threshold, these vehicles become a natural first line of strategy — and they work best alongside trust-based structures that remove assets from the estate entirely.

Irrevocable Trusts for Estate Removal

Irrevocable Life Insurance Trusts (ILITs) and Dynasty Trusts remove assets from the taxable estate permanently while allowing control over eventual distributions to beneficiaries.

A skilled financial advisor handles the strategic framework — structuring beneficiary designations, titling assets, and aligning trust language with the broader financial plan. Attorneys are brought in when specific legal instruments require it, keeping the process efficient without sacrificing rigor.

Coordinating It All: Why High-Net-Worth Tax Planning Requires a Team

The strategies covered in this guide are most powerful when coordinated — not applied independently.

A Roth conversion in the wrong year can nullify the benefit of tax-loss harvesting. A large charitable contribution can interact with RMDs to create unintended tax outcomes. The goal isn't to use every strategy; it's to use the right combination for your specific income, estate size, retirement timeline, and family goals.

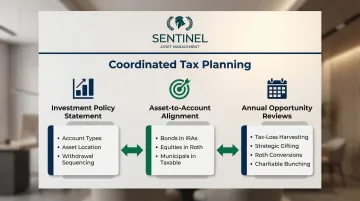

What Coordinated Planning Looks Like in Practice

Coordinated planning typically covers three interdependent areas:

- Investment Policy Statement: Integrates account types, asset location, and withdrawal sequencing — not just risk tolerance and income needs — to minimize taxes across your portfolio

- Asset-to-account alignment: Bonds in traditional IRAs, equities in Roth and taxable accounts, tax-exempt municipals in taxable accounts for high-bracket investors

- Annual opportunity reviews: Year-end harvesting, gift exclusion use, Roth conversion windows, and charitable bunching require proactive monitoring — not reactive responses

Sentinel Asset Management builds portfolios around each client's tax situation, not just their investment goals. Every recommendation — from account structure to withdrawal timing — is designed to reduce lifetime tax liability across a coordinated plan.

Tax Law Changes Frequently — Proactive Discipline Protects Wealth

Tax law changes without warning. Working with an advisory team that monitors legislative developments and adjusts strategies accordingly is itself a form of wealth protection.

Treat tax planning not as a year-end task but as a continuous, proactive discipline. The difference between reactive tax preparation and proactive tax planning can represent hundreds of thousands, or millions, of dollars over a lifetime.

Frequently Asked Questions

What is the best tax strategy for high-net-worth individuals?

There is no single "best" strategy. The most effective approach combines retirement account optimization, tax-loss harvesting, charitable giving, and estate planning, all tailored to the individual's income, portfolio size, and goals. A qualified wealth advisor coordinates these tools so they reinforce each other.

What is a comprehensive wealth management strategy?

Comprehensive wealth management integrates investment management, tax planning, retirement income planning, estate planning, and risk management into a single coordinated plan. This ensures each decision supports long-term financial goals rather than making isolated choices that could undermine other areas of the plan.

What are the 5 pillars of tax planning?

The five core pillars are:

- Income tax reduction — deductions and account contributions

- Tax deferral — retirement accounts

- Tax-free growth — Roth accounts and HSAs

- Capital gains management — harvesting and asset location

- Estate and transfer tax minimization — gifting and trusts

Effective planning coordinates all five, not just one or two in isolation.

What is considered high net worth in retirement?

"High net worth" in retirement is generally defined as $1 million or more in liquid investable assets, with "very high net worth" at $5M+ and "ultra-high net worth" at $30M+. The relevant threshold for complex tax planning strategies often begins around $1–2M in liquid assets.

How does tax planning change once you retire?

In retirement, the focus shifts from reducing earned income taxes to managing RMDs, Social Security taxation, and investment income efficiently. Strategies like QCDs, Roth conversions before RMDs begin, and careful withdrawal sequencing become critical for minimizing taxes across a multi-decade retirement.

Take the next step in your financial journey by exploring our courses page for upcoming live seminars.