General information, not personalised tax, legal or investment advice.

Introduction

Picture this: You retire in January, and by March, the stock market has dropped 15%. Your first year of retirement spending is due—$60,000 to cover living expenses—and you're staring at a portfolio that's suddenly worth $150,000 less than it was eight weeks ago. Do you sell investments at a loss to fund your lifestyle, or do you cut back and hope the market recovers?

This nightmare scenario illustrates sequence of returns risk—the danger that market downturns early in retirement can permanently damage your portfolio's ability to sustain you for 20 to 30 years. According to Vanguard research analyzing U.S. markets since 1926, retirees who face a bear market in their first years are 31% more likely to outlive their wealth compared to those who retire during stable periods.

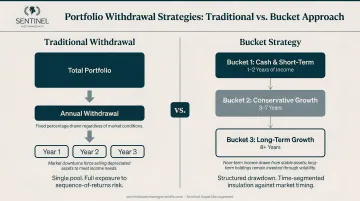

The bucket approach to retirement is a structured drawdown strategy designed to solve this exact problem. Instead of treating your retirement savings as a single pool of money, it divides assets into three time-segmented "buckets," each with a different risk level and purpose: cash for immediate needs, conservative investments for mid-term expenses, and growth assets for the long haul.

This structure provides steady income while allowing long-term assets to grow. More importantly, it gives you a clear plan for when markets turn volatile—so decisions are driven by strategy, not panic.

Key takeaways

- Divides retirement savings into three segments: short-term cash, mid-term conservative growth, and long-term equities

- Protects against sequence of returns risk by covering 1-2 years of expenses without selling during downturns

- Requires accurate expense estimation that accounts for guaranteed income sources like Social Security

- Works through periodic rebalancing: income from Bucket 2 refills Bucket 1, and gains from Bucket 3 replenish Bucket 2

- Best suited for retirees with portfolio-dependent income gaps and 20-30 year time horizons

What Is the Bucket Approach to Retirement?

The bucket approach—also called the "3-bucket strategy"—was pioneered by financial planner Harold Evensky in 1985 as a "cash flow reserve" and later popularized by Morningstar's Christine Benz. The core premise is simple: assets you'll need soon should be kept safe, while assets you won't touch for years can take on more risk for growth.

Unlike a single pooled portfolio, buckets give retirees a clear mental framework for how their money is organized. This isn't just about numbers—it's about psychology. Knowing that your next two years of living expenses are sitting safely in cash means you can watch the market drop 20% without losing sleep, because you can see that your near-term needs are already funded.

How buckets differ from traditional total-return strategies:

Traditional approaches sell from a single portfolio regardless of market conditions, which can mean liquidating stocks at the worst possible time. The bucket strategy avoids this by drawing from the safest, most liquid assets first during downturns. Your invested assets stay untouched, preserving their ability to recover and compound when markets rebound.

In practice, that difference looks like this:

- Traditional approach: Sell whatever's available — stocks, bonds, cash — to fund withdrawals, even in a downturn

- Bucket approach: Draw from cash reserves first, leaving growth assets time to recover before you touch them

A 2013 study in the Journal of Financial Planning found that appropriate use of cash reserves improves plan survival rates by up to 6 percentage points at the 30-year mark, largely by preventing the need to sell investments at depressed prices.

The Three Buckets Explained

Each bucket serves a distinct time horizon and investment purpose. Together, they balance the competing needs of income stability (Bucket 1), inflation protection (Bucket 2), and long-term growth (Bucket 3).

Bucket 1: Short-Term (Years 0-2)

Bucket 1 holds 1-2 years of living expenses in cash or cash equivalents—savings accounts, money market funds, short-duration CDs, Treasury bills. The goal is zero risk to principal and immediate liquidity.

How to calculate your Bucket 1 amount:

- Estimate your total annual retirement spending

- Subtract guaranteed income sources (Social Security, pension, annuity payments)

- The remaining "gap" determines your cash need

Example: If you need $80,000/year and receive $30,000 from Social Security, your portfolio must cover $50,000 annually. Bucket 1 should hold $50,000 × 2 years = $100,000 in cash.

As of March 2026, the average monthly Social Security benefit for retired workers is $2,079.49 (about $25,000 annually), which significantly reduces the withdrawal burden for most retirees.

Bucket 2: Mid-Term (Years 3-10)

Bucket 2 covers expenses for roughly years 3-10 of retirement and is invested in conservative to moderate assets:

- High-quality intermediate bonds

- Dividend-paying equities

- Balanced funds

- CDs with longer maturities

The goal is to at least match inflation while preserving capital. Bucket 2 serves as the "refill engine" for Bucket 1: as Bucket 1 is drawn down, income distributions (interest, dividends) from Bucket 2 replenish it, allowing growth assets in Bucket 3 to remain untouched.

For context, the Vanguard Total Bond Market Index Fund (VBTLX) reported a 10-year average annual return of 1.69% as of March 31, 2026—modest, but stable.

Bucket 3: Long-Term (Years 10+)

Bucket 3 holds assets not needed for 10+ years, invested in growth-oriented holdings:

- Diversified equities

- Index funds

- Small-cap and international stocks

This long time horizon allows Bucket 3 to absorb short-term market swings and grow steadily over decades. Bucket 3's growth is what ultimately sustains the entire strategy over a 20-30 year retirement. Periodically trimming gains from Bucket 3 flows back into Bucket 2—and eventually into Bucket 1—keeping the whole system self-sustaining.

How to Fund and Implement Your Bucket Strategy

Step 1: Estimate Retirement Expenses

Track your current spending as a baseline, then adjust for retirement-specific changes:

- Healthcare costs, which tend to rise significantly — the Bureau of Labor Statistics reports households aged 65–74 spend an average of $65,149 annually

- Reduced commuting costs

- Travel goals

- Inflation over the expected retirement period

Step 2: Account for Guaranteed Income Sources

Social Security, pensions, annuities, and RMDs reduce the withdrawal burden on your portfolio.

Example: If annual expenses are $80,000 and Social Security provides $30,000, only $50,000 must come from the portfolio—which directly determines how much to hold in each bucket.

Step 3: Fund Bucket 1 with Cash

Using the example above: $50,000/year portfolio income need × 2 years = $100,000 in Bucket 1 as cash/cash equivalents.

Critical: Bucket 1 is not invested—it is purely a liquidity reserve.

Step 4: Divide Remaining Assets Across Buckets 2 and 3

After funding Bucket 1, divide the remaining investable assets between Buckets 2 and 3 according to your overall target asset allocation.

Example: A 60/40 portfolio would put:

- 40% of remaining assets in Bucket 2 (bonds, conservative holdings)

- 60% in Bucket 3 (equities, growth assets)

Sentinel Asset Management's approach uses a personalized Investment Policy Statement to guide this allocation, stress-tested across different market conditions including historical bear markets, recessions, and inflationary periods.

Step 5: Select Investments Within Each Bucket

Bucket 2 investments:

- Investment-grade bonds

- Dividend stocks

- Balanced funds

Bucket 3 investments:

- Diversified equities

- Index funds

- Growth-oriented assets

Align investment selection with a documented allocation policy and your specific tax situation. That policy framework matters more than any individual holding. Sentinel's approach builds on modern portfolio theory to reduce unsystematic risk through deliberate diversification — managing the five systematic PRIME risks: Purchasing Power, Reinvestment, Interest Rate, Market, and Exchange Risk.

Rebalancing and Maintaining Your Buckets Over Time

The Core Rebalancing Principle

As Bucket 1 is drawn down and market performance causes Buckets 2 and 3 to drift from their target allocations, periodic rebalancing restores the intended risk profile and refills depleted buckets. Review at least annually or after significant market moves.

The Refill Sequence

- Income distributions from Bucket 2 (interest, dividends) flow into Bucket 1

- If income is insufficient, trim gains from Bucket 3 to replenish Bucket 2 and then Bucket 1

- Last resort only: draw principal from Bucket 2—avoid tapping Bucket 3 during a market downturn if at all possible

Market Downturn Strategy

Bucket 1 exists specifically to cover 1–2 years of expenses without selling anything, giving Buckets 2 and 3 time to recover. If a downturn is severe and prolonged:

- Reduce discretionary spending

- Delay large purchases

- Avoid liquidating growth assets at a loss

The Academic Perspective

Research—including a 115-country, 115-year study by Javier Estrada—suggests that static asset allocation strategies with disciplined rebalancing can match or outperform bucket strategies on pure performance metrics. The bucket approach's primary value is behavioral: providing emotional reassurance and a clear drawdown structure, which is itself a meaningful outcome for long-term financial success.

That behavioral edge also has mathematical backing. Michael Kitces' research shows that when a bucket strategy is paired with annual rebalancing, the outcome is mathematically identical to managing the portfolio on a total-return basis — meaning the structure works not despite its simplicity, but because of it.

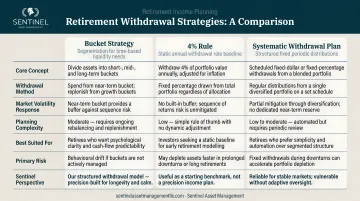

Bucket Strategy vs. Other Retirement Withdrawal Approaches

The 4% Rule

The 4% rule—originated by William Bengen in 1994—suggests withdrawing 4% of your portfolio in year one, then adjusting for inflation each year thereafter.

Pros:

- Simple to implement and backed by decades of historical research

Cons:

- Doesn't account for market timing or individual spending flexibility

- Treats the entire portfolio as one undifferentiated pool

- Struggles in low-yield environments — research from the Financial Planning Association and Morningstar's 2026 State of Retirement Income report both point to a safer starting rate of 3.9% under current conditions

Systematic Withdrawal Plans (SWPs)

SWPs take an even simpler approach than the 4% rule: withdraw a fixed dollar amount or percentage on a set schedule, regardless of what markets are doing.

Pros:

- Easiest to set up and automate

Cons:

- Carries the highest sequence-of-returns risk — withdrawals continue even during sharp downturns, which can permanently deplete the portfolio early in retirement

The Trade-Off

The bucket strategy does carry one cost: cash sitting in Bucket 1 earns less than it would if fully invested. That's the opportunity cost of holding near-term reserves.

For most retirees, that trade-off is worth it. The bucket approach provides behavioral stability and sequence-of-returns protection that neither the 4% rule nor SWPs can match — especially during the first decade of retirement, when a poorly timed downturn can do lasting damage to a portfolio.

Pros, Cons, and Who the Bucket Strategy Works Best For

Pros

- Protects against sequence of returns risk by ensuring near-term needs are funded without selling during downturns

- Provides psychological clarity and reduces anxiety about market volatility

- Flexible enough to accommodate changing expenses or income sources

- Can be combined with Social Security delay strategies or annuitization

Cons

- Cash drag on returns: Holding cash in Bucket 1 creates an opportunity cost, and inflation erodes purchasing power over time

- Requires ongoing monitoring — periodic rebalancing demands either time or professional oversight

- Hard to predict expenses or lifespan accurately

- May be overly complex for very small portfolios

Who It Works Best For

The ideal candidate:

- Retirees with a portfolio-dependent income gap — meaning expenses exceed guaranteed income from Social Security or pensions

- Those who are sensitive to market volatility and need emotional reassurance

- Individuals with a 20–30 year retirement time horizon

- Those who benefit from a structured, easy-to-understand drawdown plan

The ongoing rebalancing and tax-efficient drawdown sequencing involved is also where professional guidance tends to pay for itself. Sentinel Asset Management has guided over 2,000 clients through retirement, coordinating withdrawal sequencing across taxable, tax-deferred, and tax-free accounts to minimize lifetime tax liability and keep portfolios resilient through market cycles.

Frequently Asked Questions

What is the 3-bucket retirement strategy?

The 3-bucket strategy divides retirement assets into three time-segmented pools: cash for immediate needs (1-2 years), conservative investments for mid-term needs (3-10 years), and growth assets for long-term needs (10+ years). This structure provides steady income while protecting against market volatility.

What is the biggest mistake most people make regarding retirement?

One of the most common and costly mistakes is failing to plan for sequence of returns risk. Retiring without sufficient liquid reserves means being forced to sell investments during a market downturn, permanently reducing the portfolio's recovery potential and increasing the likelihood of outliving your savings.

How much do I need to retire on $80,000 a year at 60?

Subtract guaranteed income (Social Security, pension) from your $80,000 target to find your portfolio income gap. If Social Security covers $30,000, you need $50,000 annually from your portfolio — roughly $1,250,000 using the 25x rule. Bucket sizing is based on that gap, not total savings alone.

What is the $1,000-a-month rule for retirement?

The $1,000-a-month rule suggests that for every $1,000/month of income needed, you require approximately $240,000 saved (based on a 5% withdrawal rate). Treat it as a starting estimate — actual bucket funding depends on your specific expenses, guaranteed income sources, and true portfolio withdrawal need.

What is the 30-30-30-10 rule for retirement?

This is an alternative allocation framework advocating 30% in equities, 30% in bonds, 30% in real assets or annuities, and 10% in cash. Unlike the bucket approach's time-horizon segmentation (which organizes assets by when you'll need them), the 30-30-30-10 rule uses fixed asset-class percentage splits regardless of spending timeline.

What is Dave Ramsey's 8% rule?

Dave Ramsey advocates withdrawing 8% annually from a retirement portfolio, based on an assumption of higher long-term stock returns. Research by Karsten Jeske shows this approach has a historical failure rate of 56% to 61% at current market valuations. By contrast, the 3.9–4% safe withdrawal rate — and the more conservative bucket approach — carry substantially lower failure rates across historical market cycles.

Take the next step in your financial journey by exploring our courses page for upcoming live seminars.