General information, not personalised tax, legal or investment advice.

Introduction

A retirement income plan is not a "set it and forget it" document. It's a living strategy that must evolve as laws shift, markets fluctuate, and personal circumstances change. For many retirees, a plan built even one or two years ago no longer reflects today's tax rules, contribution limits, or economic realities.

2026 brings several specific triggers that make a plan review more urgent than usual:

- Updated RMD timelines under SECURE Act 2.0

- Elevated catch-up contribution limits for those aged 60–63

- Permanent Tax Cuts and Jobs Act (TCJA) provisions reshaping tax brackets

- Persistent inflation and evolving Social Security cost-of-living adjustments

Each of these changes can affect how much you keep, how long your savings last, and what you leave behind.

This article covers what has changed in 2026 that matters, what to look for in your current plan, and the warning signs that your current strategy needs updating.

Key takeaways

- Plans built even a year ago may not reflect 2026's updated tax rules, RMD age, or contribution limits

- The TCJA tax brackets and estate exemption are now permanent, eliminating the 2026 expiration cliff

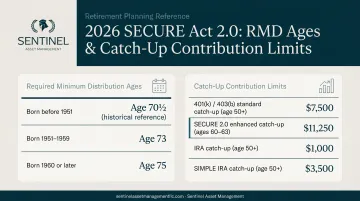

- RMD age remains 73 for those turning 72 after 2022, with higher catch-up limits for ages 60–63

- Key review areas: withdrawal sequencing, Social Security timing, Roth conversions, healthcare costs, and estate alignment

- Annual reviews help avoid costly gaps and uncover new planning opportunities

Why 2026 Demands a Fresh Look at Your Retirement Income Plan

The Retirement Planning Landscape Has Shifted

Persistent inflation continues to erode purchasing power, particularly for retirees drawing income today. Medical care costs have grown faster than overall inflation, creating a gap between Social Security's 2.8% COLA for 2026 and actual healthcare expense growth. This mismatch forces retirees to draw more heavily on portfolio assets to maintain their standard of living.

Elevated interest rates have reshaped bond dynamics. Higher yields offer better income potential, but they also introduce reinvestment risk—the possibility that maturing bonds or coupon payments must be reinvested at less attractive rates if the environment shifts. Retirees who locked in higher rates over the past two years must now plan for how to redeploy those funds as investments mature.

Market volatility amplifies sequence-of-return risk for anyone currently drawing income. Early losses can permanently impair portfolio longevity in ways that later recoveries cannot fully repair. A plan that doesn't account for near-term cash flow protection during volatile periods leaves retirees vulnerable to selling assets at depressed prices.

Legislative Changes in Effect for 2026

The One, Big, Beautiful Bill Act (OBBBA) made TCJA provisions permanent in 2025, averting a scheduled expiration that would have increased taxes for an estimated 62% of filers. For 2026, this means:

- Individual tax brackets remain at current levels (10%, 12%, 22%, 24%, 32%, 35%, 37%)

- Standard deduction is $32,200 for married couples filing jointly and $16,100 for single filers

- Estate tax basic exclusion amount increases to $15,000,000 per individual

These permanent changes eliminate the urgency around completing Roth conversions before a 2026 expiration, but they don't eliminate the value of conversion planning. Tax bracket management remains a critical optimization opportunity.

SECURE Act 2.0 continues to reshape retirement account rules. The RMD age is 73 for individuals who turn 72 after December 31, 2022, and before January 1, 2033. The first RMD can be delayed until April 1 of the year following the year you turn 73.

New for 2026: Catch-up contribution limits for ages 60–63 increase to $11,250 in 401(k), 403(b), and similar plans—$3,250 more than the standard $8,000 catch-up for those 50 and over. This creates a meaningful opportunity for late-stage savers to accelerate retirement funding.

Social Security and Longevity Considerations

The 2.8% Social Security COLA for 2026 increases the average retirement benefit by approximately $56 per month. For those who haven't yet started benefits, this adjustment may shift the math on optimal claiming strategy — a plan built around prior COLA assumptions may no longer reflect the best timing.

Each year of delay past full retirement age increases Social Security benefits by approximately 8%, making longevity assumptions critical. The Social Security Administration's 2025 Trustees Report puts life expectancy at age 65 at 18.5 years for males and 21.0 years for females — but those are averages. Many retirees will live considerably longer, pushing income needs well into the 25–35 year range.

Over that time horizon, even a 0.5% annual drag from avoidable taxes, unnecessary fees, or suboptimal withdrawal sequencing can erode hundreds of thousands of dollars in real purchasing power. The case for reviewing your plan isn't just that circumstances change — it's that the cost of not reviewing compounds quietly, year after year.

Key Areas to Revisit in Your 2026 Retirement Income Plan

No two plans need identical adjustments, but gaps most frequently emerge in these areas:

Your Withdrawal Sequencing Strategy

The conventional withdrawal sequence—taxable accounts first, then tax-deferred, then tax-free—maximizes tax-deferred growth. But this sequence is not universal. Tax bracket shifts, RMD requirements, and capital gains thresholds all affect optimal ordering each year.

2026 Capital Gains Tax Thresholds:

| Tax Rate | Single Filers | Married Filing Jointly |

|---|---|---|

| 0% | $0 to $49,450 | $0 to $98,900 |

| 15% | $49,451 to $545,500 | $98,901 to $613,700 |

| 20% | Over $545,500 | Over $613,700 |

A plan using last year's brackets may miss opportunities to harvest long-term capital gains at 0% or manage conversions within preferred tax bands.

Exceptions to standard sequencing:

- Proportional withdrawals across account types may fill low tax brackets before Social Security and RMDs begin

- Accelerating tax-deferred withdrawals during the "retirement income valley" (the years between retirement and RMD age) can reduce future required distributions

- Harvesting capital gains up to the 0% threshold prevents future taxation when rebalancing becomes necessary

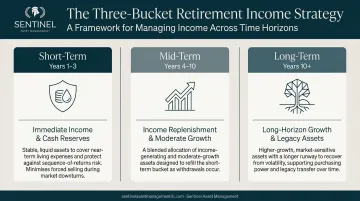

The Bucket Approach:

Each of these exceptions points toward a broader framework for managing cash flow under uncertainty. A structured bucket strategy segments income sources by time horizon:

- Near-term bucket (0–3 years): Cash, short-term bonds, and stable value funds to meet immediate spending needs regardless of market conditions

- Mid-term bucket (3–10 years): Balanced allocations that provide moderate growth while refilling the near-term bucket

- Long-term bucket (10+ years): Growth-oriented assets positioned to maintain purchasing power over decades

This approach insulates day-to-day spending from short-term market swings and protects against sequence-of-return risk. When markets decline, you draw from stable buckets rather than selling growth assets at depressed prices.

Social Security and Benefit Timing

Optimal Social Security claiming strategy can change as circumstances evolve. A spouse's health diagnosis, changes in other income sources, or a revised view of longevity may shift the calculus on whether to delay, claim now, or coordinate with a partner.

Each year of delay past full retirement age increases benefits by approximately 8%—a guaranteed, inflation-adjusted return that's difficult to replicate through investments. For married couples, coordinating claims to maximize survivor benefits often delivers better lifetime income than both spouses claiming early.

Provisional Income Management:

Social Security benefits are partially taxable based on "combined income" (Adjusted Gross Income + Nontaxable Interest + ½ of Social Security Benefits). Thresholds are:

- Up to 50% taxable: above $25,000 (Single) / $32,000 (Joint)

- Up to 85% taxable: above $34,000 (Single) / $44,000 (Joint)

These thresholds are not indexed for inflation, meaning more retirees face taxation each year as incomes rise. Managing withdrawals, conversions, and other income events to control provisional income is a key part of tax-efficient plan reviews.

Tax Law Changes and Roth Conversion Windows

Roth Conversion Opportunities:

Roth conversions remain valuable even after the TCJA permanence, particularly during the retirement income valley. Converting traditional IRA funds to Roth during years when taxable income is lower—after retirement but before RMDs and Social Security begin—reduces future tax liability.

Risks to consider:

- Conversions increase gross income, potentially triggering Medicare IRMAA surcharges based on a two-year lookback

- Conversions increase the taxable portion of Social Security benefits if you've already started claiming

- Large conversions can push you into higher tax brackets, reducing efficiency

2026 tax brackets are now permanent, shifting the focus from "beat the TCJA expiration" to optimizing true marginal tax rates—the actual percentage paid when accounting for deduction phaseouts, Social Security taxation, and IRMAA thresholds.

Qualified Charitable Distributions (QCDs):

For those 70½ or older, donating up to $111,000 directly from an IRA in 2026 satisfies RMD requirements without adding to taxable income. QCDs are powerful for charitably inclined retirees because they:

- Reduce taxable income more effectively than itemized charitable deductions

- Avoid increasing provisional income that affects Social Security taxation

- Help manage IRMAA exposure by keeping Modified AGI lower

Healthcare Cost and Coverage Review

Healthcare is one of the most volatile and underestimated line items in retirement. Fidelity's 2025 estimate reveals that a 65-year-old retiring today could spend $172,500 on healthcare over retirement. For couples with high prescription drug needs, EBRI research shows some may need up to $469,000 in savings to have a 90% chance of covering healthcare costs.

Medicare Plan Review:

Medicare open enrollment runs October 15–December 7 annually. Plan costs, covered benefits, and provider networks change each year, making annual review essential. Even if you're satisfied with current coverage, comparing Part D plans and Medicare Advantage options can reveal cost savings or better coverage.

IRMAA Management:

Income-Related Monthly Adjustment Amount (IRMAA) surcharges increase Medicare Part B and Part D premiums based on Modified Adjusted Gross Income (MAGI) from two years prior.

2026 IRMAA Thresholds:

| MAGI (Single / Joint) | Part B Premium | Part D Surcharge |

|---|---|---|

| ≤ $109k / ≤ $218k | $202.90 (Standard) | $0.00 |

| > $109k to $137k / > $218k to $274k | $284.10 | +$14.50 |

| > $137k to $171k / > $274k to $342k | $405.80 | +$37.50 |

| > $171k to $205k / > $342k to $410k | $527.50 | +$60.40 |

Even a modest increase in Modified AGI can push you into a significantly higher premium bracket. Timing withdrawals, conversions, and capital gains realizations to avoid IRMAA cliffs can save thousands annually.

Estate and Legacy Alignment

Retirement income planning and estate planning must be reviewed together. Beneficiary designations, trust structures, and will provisions can become misaligned with current intentions if left unreviewed.

The TCJA estate tax exemption is now permanent at $15,000,000 per individual for 2026, eliminating the planned reversion to approximately $7.1 million. This permanence removes urgency around accelerated gifting, but asset titling, trust structures, and distribution strategies still warrant a close look—particularly for estates that were structured around the old lower threshold.

Beneficiary Designation Risks:

Beneficiary designations on retirement accounts and life insurance policies override instructions in wills and trusts. Failure to update designations after marriage, divorce, or a beneficiary's death can result in assets passing to unintended heirs. The Supreme Court case Egelhoff v. Egelhoff established that ERISA preempts state laws that automatically revoke spousal beneficiary designations upon divorce. In practical terms: an ex-spouse remained the legal beneficiary because no one updated the form.

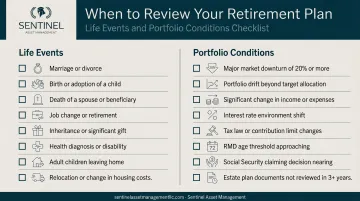

Signs Your Retirement Income Plan Needs an Update

Life Event Triggers

These events almost always require immediate plan revision:

- A spouse's death, divorce, or major health diagnosis

- Sale of a home or business

- Receipt of an inheritance

- Retirement of a working spouse

- Supporting adult children or grandchildren unexpectedly

Any event that materially changes income, expenses, or tax situation warrants a full plan review. Portfolio conditions can trigger the same need — often with less warning.

Market-Driven Triggers

Portfolio performance can silently undermine plan assumptions:

- A portfolio that has grown beyond projections may need rebalancing; one that has declined may require withdrawal rate adjustments

- A 4% initial withdrawal rate may have drifted to 5% or 6% if the portfolio declined — increasing depletion risk

- Morningstar's 2025 research lowered the "safe" starting withdrawal rate to 3.7% for a 30-year horizon, citing higher equity valuations and lower bond yields

Behavioral Drift

Lifestyle spending changes often occur gradually:

- Discretionary travel has increased

- Supporting children or grandchildren has become a regular expense

- Unexpected home repairs or healthcare costs have appeared

When spending consistently runs $500–$1,000/month above projections without a plan adjustment, withdrawal rates creep upward — and the compounding effect over a decade is significant.

What Happens If You Don't Revisit Your Plan

The Compounding Cost of Inaction

A retirement income plan that isn't reviewed annually allows small inefficiencies to grow:

- Paying more tax than necessary on withdrawals

- Missing Roth conversion windows during low-income years

- Maintaining an investment allocation that no longer fits current risk tolerance or time horizon

- Letting healthcare cost inflation erode purchasing power without adjustment

Sequence of Return Risk

A retiree drawing down a portfolio during a market downturn without a structured income strategy can permanently impair long-term wealth. Unlike younger investors who have time to recover, retirees selling assets at depressed prices lock in losses that compound over decades.

A bucket-based plan addresses this directly by keeping near-term income insulated from volatility. When markets decline, retirees draw from stable buckets, allowing growth assets to recover without forced selling. Sentinel Asset Management stress-tests each plan against historical bear markets, recessions, and inflationary periods — so clients have a clear path forward before conditions deteriorate, not after.

Estate Planning Consequences

Outdated beneficiary designations and estate documents can undo years of careful planning:

- Assets passing to the wrong individuals

- Unintended tax burdens on heirs

- Charitable or family bequests going unfulfilled

- Key decisions left to probate courts rather than your documented wishes

Research shows that outdated beneficiary designations after divorce or a beneficiary's death are among the most common—and costly—estate planning mistakes.

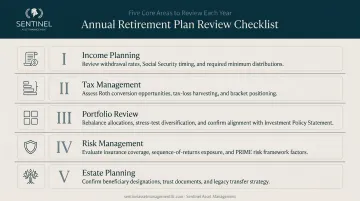

How to Make the Most of Your Annual Plan Review

What a Productive Review Covers

A comprehensive annual review is more than an investment check-in. It should include:

- Income and expense projections updated to reflect actual spending patterns

- Portfolio stress-tests run across multiple market scenarios for sustainability

- A current-year tax projection to surface savings opportunities before year-end

- Confirmation that your Social Security claiming strategy still makes sense

- Insurance and estate documents reviewed for alignment with your current goals

The Value of an Investment Policy Statement

An Investment Policy Statement (IPS) is a written document that governs how a portfolio is managed, under what conditions it is adjusted, and how withdrawal strategies are stress-tested against different market environments.

Sentinel Asset Management uses a formal IPS for every client portfolio. Having guided 2,000+ clients into retirement, the firm structures each IPS to specify exactly when and how portfolios adjust — so when markets shift, the response follows a predetermined framework rather than a reactive one. The result is a plan built on deliberate strategy, not short-term noise.

What to Bring to Your Review

A well-prepared review meeting stays focused on strategy rather than paperwork. Bring the following:

- Account statements for all retirement accounts

- Social Security estimates and current benefit information

- Medicare plan information and premium statements

- Insurance policies (life, disability, long-term care)

- Documentation of any life changes since the last meeting

- Updated income and expense records

The more complete your picture going in, the more your advisor can focus on what actually moves the needle for 2026.

Frequently Asked Questions

What is a good monthly retirement income in 2026?

"Good" is highly personal and depends on pre-retirement spending, location, and goals. The common guideline suggests replacing 70–80% of pre-retirement income. According to the U.S. Census Bureau, the median household income for those 65 and older in 2024 was $56,680 annually. However, working backward from your specific lifestyle goals is more useful than benchmarking against averages.

What is the number one mistake retirees make?

The most commonly cited mistake is failing to plan for longevity—underestimating how long retirement will last and withdrawing too aggressively in the early years. Running out of money decades into retirement is a real risk that an updated withdrawal strategy can help prevent.

How often should I review my retirement income plan?

A full review should occur at least once a year, and more frequently after major life events (health changes, inheritance, sale of property), tax law changes, or significant market moves.

What are the 2026 RMD changes I should know about?

Under SECURE Act 2.0, the Required Minimum Distribution age is 73 for anyone who turned 72 after December 31, 2022. Your first RMD can be delayed until April 1 of the year after you turn 73, which affects when you must begin drawing from tax-deferred accounts.

How do I know if my withdrawal rate is still sustainable?

A withdrawal rate that started at 4% may have drifted higher if the portfolio declined, or lower if markets performed well. A stress-test comparing your current rate against multiple market scenarios—ideally done with an advisor—is the best way to assess ongoing sustainability.

What happens to my retirement plan if tax laws change in 2026?

The TCJA provisions are now permanent, eliminating the scheduled 2026 expiration. However, tax laws can still change through future legislation. If rates rise, Roth conversions completed before increases become even more valuable. Consult with a tax advisor to model the impact on your specific situation.

A retirement income plan is only as good as its most recent update. Permanent tax law changes, updated RMD rules, rising healthcare costs, and market uncertainty make 2026 a critical year to revisit your strategy. Whether you built your plan last year or five years ago, a comprehensive review ensures it still serves your goals—and surfaces adjustments you may not have considered.

For personalized guidance on updating your retirement income plan, contact Sentinel Asset Management at 203-793-0707 or visit one of our five offices across Connecticut and Maryland.

Take the next step in your financial journey by exploring our courses page for upcoming live seminars.