General information, not personalised tax, legal or investment advice.

This guide walks families through every layer of generational wealth planning: building assets designed to last, protecting them from erosion, transferring them intentionally through legal structures, and preparing heirs to sustain them.

Key takeaways:

- Generational wealth requires multi-decade strategy combining investment discipline, tax efficiency, and legal architecture

- Diversified portfolios stress-tested with an Investment Policy Statement outperform passive accumulation across generations

- Estate planning through trusts and coordinated tax strategy prevents wealth erosion before transfer

- Heir preparation and family mission statements are essential—unprepared beneficiaries are the primary reason wealth fails to survive

What Is Generational Wealth Planning?

Generational wealth encompasses the financial assets—investments, real estate, business interests, life insurance, and cash—passed from one generation to the next, alongside the values, habits, and knowledge needed to preserve them.

Generational wealth planning is the proactive, multi-decade process of building, protecting, and transferring those assets in a way that reflects the family's goals, reduces tax erosion, and prepares heirs to be responsible stewards. The strategy evolves continuously—adapting to shifting family circumstances, tax law changes, and market conditions over time.

Generational wealth planning isn't exclusively for the ultra-wealthy. Families at many income levels can build a meaningful legacy through consistent strategy and early action. What separates those who build lasting wealth from those who don't is rarely starting capital—it's intentional planning, disciplined decisions made over time, and a coordinated approach to the full financial picture.

Building Wealth Designed to Last

The earliest decisions about asset accumulation set the trajectory for a multi-generational plan. Long time horizons, compounding returns, and strategic asset selection create wealth that endures. Passive accumulation without strategy rarely survives across generations because it lacks the structural resilience to withstand market cycles, tax changes, and family transitions.

Choosing the Right Asset Classes

A diversified mix of asset classes gives generational wealth multiple growth engines and income streams. Each plays a specific role:

- Equities provide long-term growth and capital appreciation

- Real estate offers equity accumulation and ongoing income

- Business interests create legacy value and operational continuity

- Cash-value life insurance enables tax-free wealth transfer and liquidity for estate taxes

Publicly traded securities form the foundation of most generational portfolios, offering liquidity, diversification, and access to global markets.

Real estate serves a dual role: home equity builds intergenerational wealth, while rental properties generate ongoing cash flow that can fund family needs or reinvest into other assets.

Family business succession planning turns an operating company into a multi-generational asset. Without a formal succession plan, business value is often lost at the owner's death or retirement. Structuring ownership, defining governance, and preparing successors ensures the business continues to generate value for future generations.

Building a Portfolio Guided by an Investment Policy Statement

A written Investment Policy Statement (IPS) defines investment goals, risk tolerance, income needs, and time horizon. It serves as the disciplined framework that prevents emotional decision-making from derailing a long-term wealth plan.

Sentinel Asset Management builds every client portfolio around an IPS, using their PRIME risk framework (Purchasing Power, Reinvestment, Interest Rate, Market, and Exchange Risk) to stress-test portfolios across market conditions. Each portfolio is tested against historical bear markets, recessions, and inflationary periods—surfacing vulnerabilities before they become real losses.

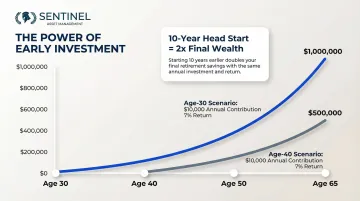

That disciplined framework matters most when paired with time. Starting a $10,000 annual contribution at age 30 rather than age 40—at a 7% return—produces roughly $1 million by age 65 compared to $500,000. A 10-year head start can double final wealth, purely through compounding.

Protecting Wealth Through Risk Management, Insurance, and Tax Strategy

Building wealth is only half the equation. Without a deliberate protection strategy, market downturns, unexpected life events, and tax erosion can quietly dismantle what took decades to build.

Managing Risk in a Multi-Generational Portfolio

Diversification across asset classes, geographies, and sectors is the primary defense against unsystematic risk. A globally diversified, tax-efficient portfolio is better positioned to withstand market cycles than one concentrated in a single sector or region.

Sentinel's PRIME framework addresses the five systematic risks that cannot be diversified away:

- Purchasing Power Risk – Inflation eroding real returns over decades

- Reinvestment Risk – Uncertainty of rates at which interim cash flows can be reinvested

- Interest Rate Risk – Bond price fluctuations as rates change

- Market Risk – Broad market downturns affecting all securities

- Exchange Risk – Currency fluctuations impacting international holdings

Disability insurance protects the income that funds wealth-building during working years. Permanent life insurance provides tax-free liquidity for heirs—particularly valuable for covering estate taxes due shortly after death, preventing forced asset sales.

Risk management and insurance address what can happen to your wealth unexpectedly. Tax strategy addresses what happens to it predictably—and preventably.

Tax Strategy as a Wealth Preservation Tool

Without coordinated tax planning, a significant portion of accumulated wealth erodes before it reaches heirs through income taxes, capital gains taxes, estate taxes, and state-level inheritance taxes.

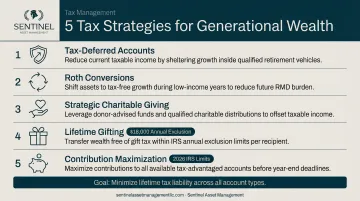

Key strategies include:

- Tax-deferred and tax-advantaged accounts – IRAs and 401(k)s shelter growth from annual taxation

- Roth conversions – Vanguard research shows that paying conversion taxes from outside accounts makes conversions advantageous even if heirs face lower tax rates

- Strategic charitable giving – Qualified Charitable Distributions and donor-advised funds reduce taxable income while supporting causes

- Lifetime gifting – Annual exclusion gifts ($18,000 per recipient in 2024) transfer wealth without tax consequences

- Contribution maximization – 2026 IRS limits raise 401(k) contributions to $24,500 and IRAs to $7,500, with a "super catch-up" of $11,250 for ages 60–63

The goal is to minimize lifetime tax liability across the entire financial ecosystem, not just in any single year. Sentinel analyzes taxable, tax-deferred, and tax-free account "buckets" as one cohesive plan, ensuring withdrawals and conversions are sequenced for maximum efficiency.

Note that estate and gift tax exemptions are subject to legislative change. Consult a tax professional to understand how any upcoming shifts may affect your specific plan.

Estate Planning and Trusts: The Legal Architecture of Wealth Transfer

Only about one-third of Americans have an estate plan, despite it being the most reliable legal tool for ensuring wealth reaches intended heirs without loss to taxes, legal disputes, or court proceedings.

Core Estate Planning Documents

Every generational wealth plan should include:

- Will – Dictates asset distribution and guardianship

- Durable power of attorney – Authorizes financial decisions if incapacitated

- Healthcare directives – Specifies medical treatment preferences

- Beneficiary designations – Properly aligned with overall plan

Mismatched beneficiary designations on retirement accounts and insurance policies frequently override even a carefully drafted will. Regular review ensures consistency across all documents.

How Trusts Strengthen Multi-Generation Wealth Transfer

Trusts are often superior to a simple will for generational wealth, providing structured distribution, asset protection, and tax advantages across multiple generations.

Relevant trust types include:

- Generation-Skipping Trusts (GSTs) – Transfer assets to grandchildren while minimizing estate taxes

- Spendthrift Trusts – Protect heirs from poor financial decisions and creditors

- Charitable Remainder Trusts – Support philanthropic goals while maintaining income for beneficiaries

Coordinating these instruments across accounts, beneficiary designations, and asset titling is where a financial advisor earns its keep. Sentinel Asset Management manages this coordination directly — organizing accounts, aligning designations, and optimizing titling — and brings in attorneys only when complex legal instruments require it.

Estate plans must be treated as living documents, reviewed and updated after major life events (marriage, divorce, birth, death, significant asset changes) and after material changes in tax law.

Preparing the Next Generation to Receive and Steward Wealth

Inheritors who are unprepared—financially and emotionally—are the primary reason generational wealth fails to survive beyond the second or third generation. Markets and tax laws are secondary factors.

A phased approach to financial education across generations includes:

- Young children introduced to saving and spending through age-appropriate money conversations

- Teenagers given direct investment education and a seat at family financial discussions

- Adult heirs included in family meetings covering the financial plan, shared values, and long-term goals

Involving heirs in philanthropic decisions and smaller investment decisions before they inherit significant assets gives them real, low-stakes practice in financial stewardship. Sentinel's legacy planning includes a "pilot" approach—a small, supervised pool of assets that allows beneficiaries to practice stewardship before receiving their full inheritance.

That early practice matters: heirs who've made real decisions—even small ones—arrive at inheritance with judgment, not just money.

Creating a Family Legacy Beyond Financial Assets

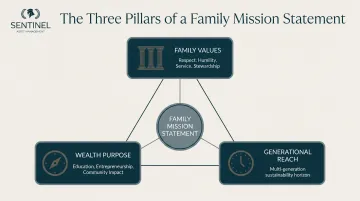

Lasting generational wealth starts with a shared family mission: a clear statement of what the family values, what the wealth is meant to accomplish, and what responsibilities come with inheriting it. Without that foundation, financial assets are more likely to be squandered or fractured by conflict.

A family mission statement creates alignment across generations and serves as a reference point during family disputes or major financial decisions. Most financial planning frameworks for family legacy organize this around three foundational components:

- Family Values – 3-5 core values (respect, humility, service, stewardship)

- Wealth Purpose – What financial resources are meant to achieve (education, entrepreneurship, community impact)

- Generational Reach – Timeline for sustaining wealth across generations

Philanthropy is a powerful vehicle for embedding values into wealth. Donor-Advised Funds held $251.52 billion in charitable assets in 2023, offering a flexible, low-burden alternative to private foundations. Families that structure giving through DAFs or charitable trusts early tend to find it easier to bring younger generations into wealth conversations — making philanthropy a practical entry point, not just a values statement.

Frequently Asked Questions

What is generational wealth planning?

Generational wealth planning is the deliberate process of building, protecting, and transferring financial assets across generations. It combines investment strategy, estate planning, tax efficiency, and family education to ensure wealth endures beyond the person who built it.

What is the best investment for generational wealth?

No single investment fits every family. A diversified combination of equities, real estate, business interests, and permanent life insurance can provide both long-term growth and income. The right mix depends on the family's goals, timeline, and risk tolerance.

What are the three types of family legacies?

The three types are financial legacy (monetary assets and property), values legacy (the principles, work ethic, and life philosophy passed down), and social or philanthropic legacy (the impact a family has on its community or causes it supports).

What is the three-generation wealth rule?

The "shirtsleeves to shirtsleeves in three generations" concept describes a common pattern: the first generation builds wealth, the second maintains it, and the third depletes it. Lack of financial education is usually the cause — and intentional planning with heir preparation directly counters this outcome.

What is the best way to protect a generations old family legacy property?

Start by placing property in a trust or family LLC to control distribution and shield against creditors. From there, establish governance agreements among heirs, secure adequate insurance, and put a formal succession plan in writing.

What is an example of a family mission statement?

"Our family builds and shares wealth to provide opportunity, support education, and contribute to our community—guided by honesty, hard work, and generosity." A financial advisor can help families draft one that reflects their specific values and goals.

Take the next step in your financial journey by exploring our courses page for upcoming live seminars.