General information, not personalised tax, legal or investment advice.

Introduction

Picture this: a surviving spouse files probate paperwork, confident that her late husband's will leaves his retirement savings to her. Weeks later, she discovers that the 401(k)—worth nearly $400,000—is instead being transferred to his ex-wife from 20 years ago. The will clearly names the current spouse as beneficiary. But the 401(k) beneficiary form, filled out decades earlier and never updated, still lists the ex-wife. Despite a valid, current will stating otherwise, the ex-wife receives the account. In this case, the will is irrelevant: the beneficiary designation controls who gets the money.

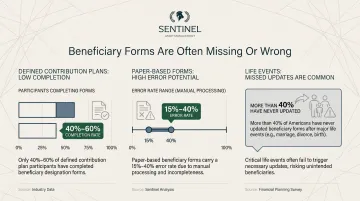

According to testimony provided to the U.S. Department of Labor, only 40% to 60% of defined contribution plan participants have even completed beneficiary forms, and paper-based forms carry a 15% to 40% error rate. A 2024 Fidelity survey found that more than 40% of Americans have never updated their beneficiary forms after major life events: marriage, divorce, the birth of a child, or the death of a loved one.

Beneficiary designations on retirement accounts, life insurance, and annuities are a form of estate planning that most people already have in place. They just need to be reviewed and aligned. This article covers what a beneficiary review involves, when to do one, which accounts it covers, the most costly mistakes to avoid, and a step-by-step process to complete it.

The good news: a beneficiary review is one of the most powerful steps you can take on your own — and the right guidance makes it straightforward.

Key takeaways

- Beneficiary designations override your will — they control who gets retirement accounts, life insurance, and annuities

- A beneficiary review confirms every account designation is current, complete, and aligned with your estate plan

- Review after any major life event: marriage, divorce, a beneficiary's death, or a new child

- Naming your estate, skipping contingent beneficiaries, or listing a minor directly are the most costly mistakes to avoid

- Most people can complete the review in one to two hours — no attorney required for the majority of accounts

What Is a Beneficiary Review (and Why It's the Simplest Estate Planning Step You're Probably Skipping)?

A beneficiary review is a structured process of checking every financial account and insurance policy with a beneficiary designation to confirm that the named individuals are correct, legally valid, and proportioned as you intend. This is distinct from updating a will or trust—it's faster, often free, and doesn't require a lawyer.

Why Beneficiary Designations Have Legal Priority

Beneficiary designations are contractual and supersede what a will or trust says. If someone remarries but never updates their 401(k) beneficiary from their first spouse, the ex-spouse receives those assets, regardless of what the will states.

The 2001 U.S. Supreme Court case Egelhoff v. Egelhoff made this concrete: the court ruled that a deceased man's ERISA-governed life insurance and pension benefits had to be paid to his ex-wife, who remained the named beneficiary, overriding a Washington state law that automatically revoked ex-spouse designations upon divorce.

The beneficiary designation on file with the plan or account custodian governs payment of death benefits, not subsequent changes in marital status or updated wills.

Primary vs. Contingent Beneficiaries

Understanding these two roles is essential:

- Primary beneficiary: First in line to receive assets

- Contingent beneficiary: Receives assets only if the primary cannot or does not (due to death or disclaimer)

Naming both is critical for avoiding unintended outcomes or court involvement. If the primary beneficiary predeceases you and no contingent is listed, assets may default to your estate or be distributed according to the plan's default rules, which is rarely what you intended.

How Beneficiary Designations Bypass Probate

Assets with valid beneficiary designations transfer directly to the named person, typically within a few weeks once the custodian verifies a death certificate (usually within 5 business days). Compare that to probate: the American Bar Association notes the process averages six to nine months, and in California it can stretch 9 to 18 months with substantial court and administrative fees attached.

When designations are aligned across all accounts, your estate plan becomes easier to execute, reduces family conflict, and can lower the tax burden on heirs. In short, keeping beneficiary designations current is one of the highest-leverage actions you can take to ensure your assets reach the right people without delay or dispute.

When Should You Review Your Beneficiary Designations?

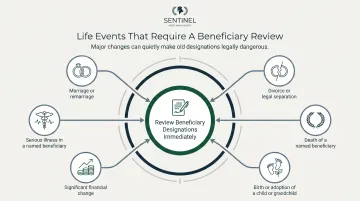

Critical Life Event Triggers

Trigger an immediate review after any of these events:

- Marriage or remarriage: Ensure your new spouse is named where appropriate

- Divorce or legal separation: Note that divorce does not automatically remove an ex-spouse as beneficiary on most accounts—you must actively update the form

- Death of a named beneficiary: Reallocate shares and name a new contingent

- Birth or adoption of a child or grandchild: Add new family members and adjust percentages

- Significant change in financial situation: Major inheritance, business sale, or a new retirement account opened

- Serious illness in a named beneficiary: Revisit contingent designations before circumstances force the decision

Life events aren't the only reason to review. Even when nothing changes, designations can quietly fall out of step with your intentions.

Routine Review Schedule

Leading financial institutions recommend checking in on a regular schedule:

- Vanguard: Review beneficiaries annually

- Schwab: Review at least every three years

- Fidelity: Review estate plans and beneficiaries every 3 to 5 years

Tying your review to tax season or open enrollment makes it easy to stay on schedule.

Don't Overlook Employer-Sponsored Plans

Many employees designate beneficiaries when they first start a job and never revisit them. Employers administer 401(k)s and pensions separately from personal IRAs, so check these independently. If your institution merges or rebrands, confirm beneficiary records transferred correctly. These accounts are often the largest assets in an estate—and the easiest to overlook.

Which Accounts and Assets Require Beneficiary Designations?

Financial Accounts That Use Beneficiary Designations

These accounts operate outside of your will and transfer by contract:

- IRAs (Traditional and Roth)

- 401(k)s and other employer-sponsored retirement plans (403(b), 457(b))

- Defined-benefit pensions

- Annuities

- Life insurance policies

- Payable-on-death (POD) bank accounts

- Transfer-on-death (TOD) brokerage accounts

Each account has its own beneficiary form. Updating one does not automatically update the others.

Assets That Don't Transfer This Way

Real estate, vehicles, and personal property typically pass through a will or trust—not beneficiary designation. A beneficiary review focuses specifically on financial accounts and insurance policies in the categories above.

That distinction matters more than most people realize. Many assume their will covers everything, but the bulk of most Americans' financial assets—retirement accounts and life insurance—are governed entirely by beneficiary forms. Finding and aligning those forms is the core of simplifying an estate plan.

Common Beneficiary Designation Mistakes That Can Unravel Your Estate Plan

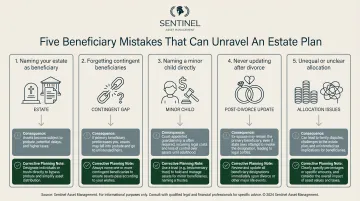

Mistake 1: Naming Your Estate as Beneficiary

Assets routed to the "estate" must pass through probate — a slow and often expensive process. For retirement accounts, this also triggers the 5-year rule if the owner died before their required beginning date.

That rule forces the entire account to be distributed within five years, eliminating any ability to stretch distributions and dramatically accelerating the tax burden on heirs.

Mistake 2: Forgetting to Name a Contingent Beneficiary

If the primary beneficiary predeceases you and no contingent is listed, assets may default to your estate or be distributed per plan documents rather than your actual wishes. This creates court delays, added legal costs, and outcomes that may not reflect what you intended.

Mistake 3: Naming a Minor Child as a Direct Beneficiary

Minors cannot legally receive large sums of money. Courts typically appoint a guardian or custodian to manage the funds, which ties up assets and adds legal overhead. Under the Uniform Transfers to Minors Act (UTMA), assets can be transferred to a custodian — the property belongs irrevocably to the child but is managed by an adult until they reach adulthood (typically 18 or 21, depending on state law).

A trust or UTMA/UGMA account is usually the better approach, and it's especially critical for families with special needs members.

Mistake 4: Never Updating After Divorce

Federal law (ERISA) preempts state laws that would otherwise revoke a beneficiary designation upon divorce. That means 401(k) and pension designations stay in force until you actively change them. In Egelhoff v. Egelhoff, the Supreme Court confirmed that ERISA-governed benefits must be paid to an ex-spouse who remained the named beneficiary.

For non-ERISA accounts like IRAs, state law governs — and while some states automatically revoke an ex-spouse's designation, relying on that without confirming is a significant risk.

Mistake 5: Unequal or Unintentional Allocation

Vague or incomplete allocation is a quiet but costly mistake. Common problems include:

- Percentages that don't add up to 100%

- Shares that weren't reallocated after a named beneficiary died

- Instructions too vague to enforce as written

Be explicit — "50% to each child" leaves no room for ambiguity or unintended outcomes.

How to Conduct a Beneficiary Review: A Step-by-Step Checklist

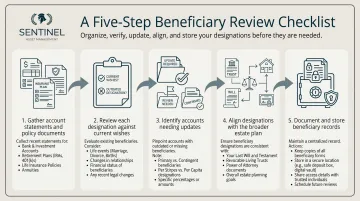

Step 1: Gather All Relevant Account Statements and Policy Documents

Create a master list of every account with a beneficiary designation:

- Retirement accounts (IRAs, 401(k)s, pensions)

- Life insurance policies

- Annuities

- POD/TOD accounts

Note the institution name, account number, and where to access beneficiary forms (online portal or paper form).

Step 2: Review Each Designation Against Your Current Wishes

For each account, verify:

- Who is named as primary and contingent beneficiary

- Percentages add up to 100%

- All named individuals are still living and reachable

- Legal names match current IDs

Step 3: Identify Accounts Needing Updates and Take Action

For each account flagged in Step 2:

- Log into the online portal or contact the institution directly to request an update form

- Complete most changes without a lawyer — the process is typically straightforward

- For employer retirement plans, contact HR or the plan administrator to obtain the correct form

Step 4: Align Designations with Your Broader Estate Plan

Cross-reference each designation against your will and any trusts to confirm intent is consistent:

- Verify that named beneficiaries align with your will's distribution goals

- If you have a revocable living trust, confirm whether accounts should name the trust or an individual as beneficiary

- This decision carries tax and legal implications — an advisor can help clarify which approach fits your plan

Step 5: Document and Store Your Beneficiary Records

Keep copies of all beneficiary designation forms in a secure, accessible location and inform a trusted person of where to find them:

- Store physical or digital copies in a consistent, labeled location

- Tell at least one trusted family member or executor where records are kept

- Review and update this master record after any major life event

Sentinel Asset Management's legacy planning advisors help clients maintain this kind of organized, cross-account record as part of a broader estate and wealth transfer plan — so nothing falls through the cracks when it matters most.

Special Considerations: Taxes, Minor Children, and Special Needs Beneficiaries

Tax Implications for Inherited Retirement Accounts

The SECURE Act mandates that most non-spouse beneficiaries empty inherited IRAs and 401(k)s within 10 years of the owner's death. The 10-year clock starts on December 31 of the year containing the 10th anniversary of the original owner's death. This accelerates taxation and can create a significant tax burden if not planned for.

Exceptions exist for Eligible Designated Beneficiaries (EDBs), who may stretch distributions over their life expectancy:

- The surviving spouse

- A minor child of the employee (until the age of majority)

- A disabled individual

- A chronically ill individual

- An individual not more than 10 years younger than the account owner

Distributions from inherited traditional IRAs are taxed as ordinary income to the beneficiary. Distributions from inherited Roth IRAs are generally tax-free, provided the original owner held the Roth IRA for at least five years before their death.

Special Needs Beneficiaries

Naming a person with a disability as a direct beneficiary can disqualify them from needs-based government benefits like Medicaid or Supplemental Security Income (SSI), as the assets are counted as resources. A Special Needs Trust (SNT) is typically the appropriate vehicle. The Social Security Administration recognizes exceptions for properly drafted SNTs and pooled trusts, allowing these vehicles to hold assets for the beneficiary's supplemental needs without counting toward SSI resource limits.

Sentinel Asset Management has spent 25 years helping families navigate these designations, coordinating with estate attorneys and care planners to ensure both financial security and benefit eligibility are protected.

Divorce and Blended Family Situations

Life structure changes — divorce, remarriage, blended families — create some of the highest-stakes beneficiary mismatches. Beneficiary reviews are especially critical in these situations, where step-children, biological children, and a new spouse all have a stake.

While ERISA preempts state laws for 401(k)s, 26 states have enacted statutes — often modeled on Uniform Probate Code § 2-804 — that automatically revoke beneficiary designations to an ex-spouse for non-ERISA assets like IRAs and life insurance. States with these revocation rules include:

- Alabama, Arizona, Colorado, Florida

- Michigan, Minnesota, New York, Texas

- Virginia, Washington, and others

A financial advisor with divorce planning experience can confirm your designations reflect your actual intent, not just who was listed at enrollment.

Frequently Asked Questions

What is a beneficiary review?

A beneficiary review is the process of examining all financial accounts and insurance policies with beneficiary designations to ensure the named individuals are current, correctly identified, and proportioned as intended. This review is separate from and often more impactful than updating a will.

How often should beneficiary designations be reviewed?

Review designations after every major life event—marriage, divorce, birth, or death—and at minimum once a year as a routine habit. Tying it to tax season or open enrollment creates a built-in, consistent review cycle.

How long do beneficiaries have to withdraw from their 401(k)?

Under the SECURE Act's 10-year rule, most non-spouse beneficiaries must deplete the inherited account within 10 years of the original owner's death. Surviving spouses and certain eligible designated beneficiaries — such as disabled individuals or minor children — follow different, more flexible timelines.

Do beneficiaries pay taxes on inherited retirement accounts?

Inherited traditional IRA and 401(k) withdrawals are generally taxable as ordinary income to the beneficiary. Inherited Roth IRA distributions are typically tax-free if the account was held for at least five years — though the timing of withdrawals under the 10-year rule can shift that tax burden considerably.

What are common pension beneficiary mistakes?

The most frequent errors include:

- Failing to name a beneficiary, which leaves assets to the estate

- Not updating designations after divorce or remarriage

- Neglecting to name a contingent beneficiary

- Assuming assets will automatically transfer to a current spouse without a properly filed designation form

Take the next step in your financial journey by exploring our courses page for upcoming live seminars.